Q4 and 2022 Market and Investment Trends Review

Global Coin Research

4 min read·

Welcome to GCR, where the community takes the lead in research and investment. Together, we source the best opportunities, conduct thorough research, and make strategic investments!

To read the full report - please visit here.

2022 in a Snapshot

The community deployed a total of $6M+ of community-sourced capital across 44 deals, and in Q4 alone we deployed $1.1M+ of community-sourced capital across 6 deals.

The GCR community saw over 500 deals during 2022, of which ~43% came directly from the community members.

The community deployed the most capital into Web3 Infrastructure (both in Q4 and Q3)

Later stage deals continue to dominate and we see a falloff in early stage opportunities

Later Stage Deals Continue to Dominate But We See Opportunities in Early Stage Deals

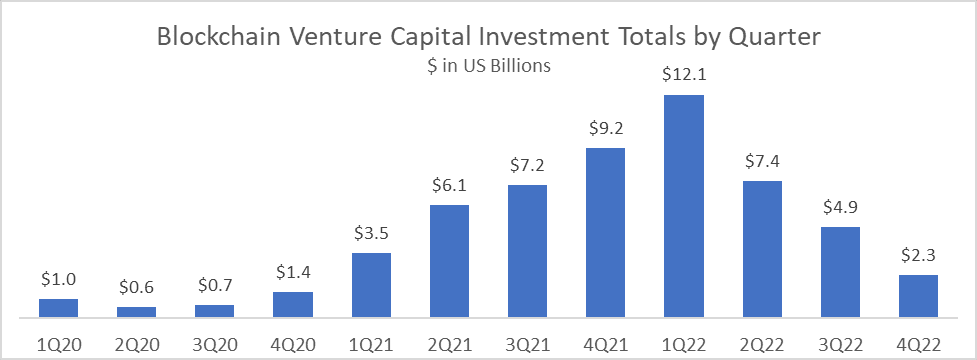

Exacerbated by the demise of FTX and unfavorable macro conditions, crypto was in the negative spotlight during Q4 2022 as liquidity flooded out of the market. Fortunately, none of our portfolio companies were directly affected by the FTX implosion and instead have been making significant strides in their roadmaps. While the collapse of FTX, BlockFi and other CeFi companies may have impeded the industry’s growth for the next few years, these events underscore the need for trustless and transparent systems.

Despite the billions of dollars in dry powder for Web3 investments, VC funding for Web3 has significantly plummeted in Q4 as non-Web3 native investors fled away from the industry. Early stage projects faced more difficulties in raising capital as investors became increasingly conservative and risk averse as they assess investment opportunities. Hence, we have seen later-stage projects with some traction and clear roadmaps garner more interest from investors, which led to competitive rounds with higher valuations. Later-stage projects will be well capitalized due to the large amount of dry powder, but we don’t see many asymmetric return opportunities in the later stage projects due to competition.

At GCR, we remain committed to Web3 and are focused on Pre-Seed and Seed Stage projects that will bring clear innovation to the Web3 ecosystem. Web3 is still a nascent industry with a lot of near-term catalysts to make it more mainstream and we believe Pre-Seed and Seed projects are the most attractive investment opportunities.

GCR Investment During 2022

Similar to our previous quarterly letters, the dominance of Infrastructure and Tooling projects returned as a pivotal theme in Q4. With Web3 enabling novel revenue streams for entrepreneurs, more top Web2 talent will migrate away from Web2 to build in Web3. The same caliber of infrastructure and tools that exists in Web2 is needed in Web3 to reduce the friction for onboarding. Instead of betting on domain-specific applications, our thesis is to underpin the core protocols and tools that empower developers to build powerful applications.

Compared to Web2, building an exceptional project in Web3 requires more resources due to additional skill sets involved in development. For example, this problem is evident in game development, which is already time and resource-intensive in Web2. Game developers would rather dedicate their resources to creating fun and well-designed games instead of focusing on the integration of user-friendly wallets, NFTs, token economies and other Web3 components with their games. Web3 infrastructure and tools should eliminate the complexities of Web3 development and enable developers to focus on their areas of expertise

Plus, with infrastructure projects, the best tech and biz plans come out on top. We're all about supporting the talented teams at Common, IntellaX, and Scroll, so join us and let's simplify Web3 development together!

Private Markets Feedback

The pace of deployment continued to slow, in particular after the collapse of FTX in November. In particular, there has been nearly no growth-stage deal activity in months as many of the larger allocators, including generalists, sovereign wealth funds and pensions, retrench after suffering flesh wounds from FTX in which many were invested. Overall, the investment pace is still ~3-4x higher than during the last bear market though, reflecting industry growth over a longer timeframe. Similarly, valuation expectations are coming down, although the number of datapoints has decreased as well making it hard to come to a general conclusion.

Macro

The dominant story of 2022 was the historically aggressive pace of rate increases enacted by the US Federal Reserve and similar actions globally in order to combat inflation, reversing a decade of declining rates. In 2023, the major story will be what the impact of higher rates will be on the economy as the lagged impact of tighter liquidity and credit conditions flow through. Eventually, the page will turn to when inflation normalizes, monetary conditions loosen and rates begin to decline again, or the “Fed Pivot”. Whether this is because the Fed, in its war against inflation, successfully engineers a soft landing or because the economic hardship from tighter monetary conditions becomes too tough to bear is yet to be seen. As is always true in investing, two reasonable people presented with the same facts can rationalize different conclusions

This remains a macro-driven market, and this is evidenced by the amount of focus and attention being paid to inflation. The market has gone from not caring much about CPI a year ago (given its decades-long trend in the +2% annualized range) to a focus on increasingly, absurdly granular metrics going from CPI to core CPI to services CPI and now to what some are calling “Supercore CPI”. No doubt tightening monetary conditions will continue to stress the economy, in particular, uneconomic highly levered entities, but the rate of change is no longer worsening.

The Big Picture

To put valuations in a longer timeframe historical context, at year-end BTC and ETH were trading at the same price as five years ago. At the same time, the industry has made meaningful advancements in both technology improvements and adoption since then:

- BTC has gained acceptance as legal tender or form of payment in multiple countries

- ETH has transitioned to Proof-of-Stake and is now a yield-bearing asset

- DeFi ($40bn industry) and NFTs ($25bn industry) are new use cases that have taken off

- Access has improved – Coinbase IPO, retail brokerages, ETF and futures products

What is particularly striking is that despite the negative backdrop, the momentum of adoption by large financial institutions and consumer brands only continues to build. In our view, this is the single most important thing to track, because the biggest upside to industry growth will come from large non-crypto native companies entering this space and bringing with them their existing multi-million user base. This past quarter:

- Google Cloud began accepting crypto for payments, powered by Coinbase Prime (link)

- Activision Blizzard COO Daniel Alegre is appointed CEO of Yuga Labs creator of Bored Ape Yacht Club (link)

- Goldman (link) and JP Morgan (link) begin using blockchains to execute and settle live fixed income and foreign exchange trades

- WisdomTree launches digital funds, which are tokenized equity and fixed income funds tradeable on the blockchain (link)

- Roofstock sells first on-chain single family home as an NFT on OpenSea (link)

As usual, If you want to take advantage of full benefits as a GCR member, please follow the steps :)

Read our most popular weekly newsletter by subscribing directly on the top bar of our website

Follow us on Twitter

Check out our Linktree for various social media platforms (e.g. TikTok, YouTube, etc.)

Also, if you have friends / people in your network who want to join GCR, please share this application (6-month Gold+ membership) with them!

Best,

The GCR Core Team