Table of contents

1、Overview

2、Critical Statistics

3、Latest news

3.1 Treasury

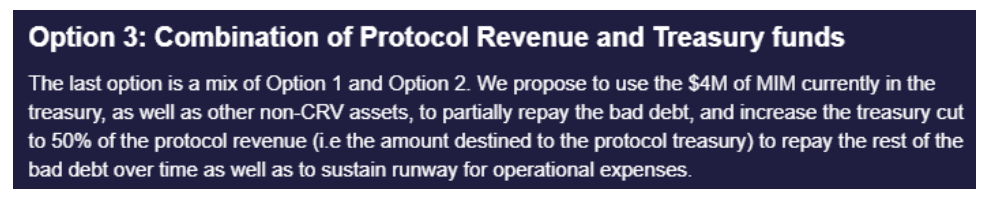

3.2 Bad Debt Repayment

3.3 Team restructure

4、Token

5、Summary

1、Overview

Abracadabra is a multichain lending protocol that utilizes interest-bearing tokens as collateral to mint a USD-pegged stablecoin - Magic Internet Money (MIM) that can be used as any other traditional stablecoin. (Interest bearing tokens are tokens whose balance changes over time due to interest accrual and have a pegged exchange rate to the underlying asset.)

The project consists of the following four major components:

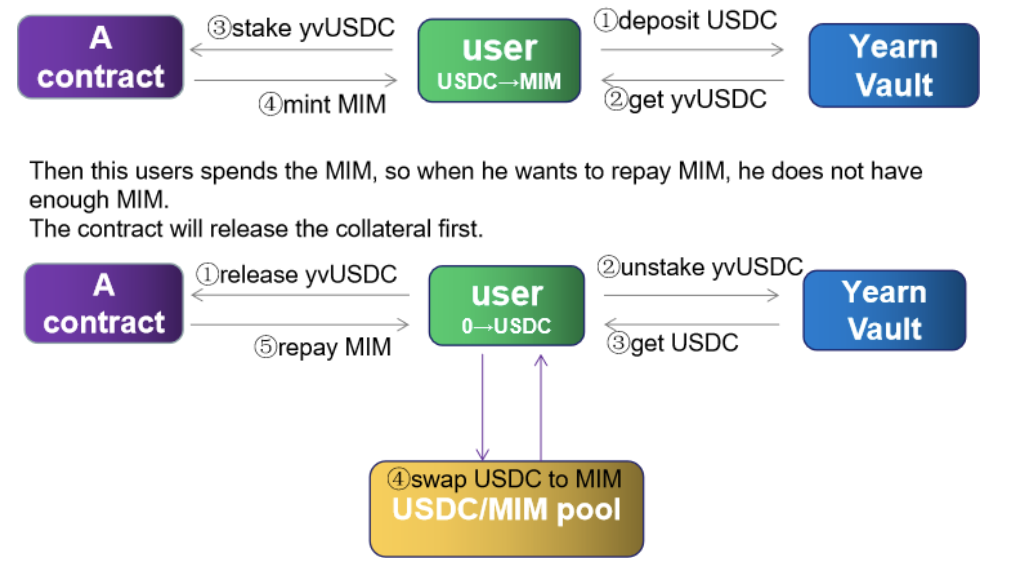

Lending Market: Users can deposit various types of collateral to mint MIM.

Leverage farm: Automatically helps users convert the borrowed MIM into USDT, and deposit these USDT into the Yearn Vault to obtain yvUSDT,which will be deposited back to Abracadabra as collateral.

That is to say: Users actually only lock in partial value of assets but can get full value APY income, and the remaining assets can be spent or made by other investments. A little bit like credit card. Of course, the liquidation risk also increases accordingly.

Farm: Using LP tokens to farm.

Two staking methods:

sSPELL - stake SPELL tokens and earn more SPELL

mSPELL - stake SPELL tokens and earn stablecoin income through $MIM

For users, in addition to interest, the cost of borrowing needs to be paid, and there is also a one-time loan fee paid when borrowing.

At present, most of the collaterals supported by Abracadabra are still mainly interest-bearing assets, and the following tokens are also supported:

ETH/wETH/wBNB/AGLD/Cake/wBTC

2、Critical Statistics

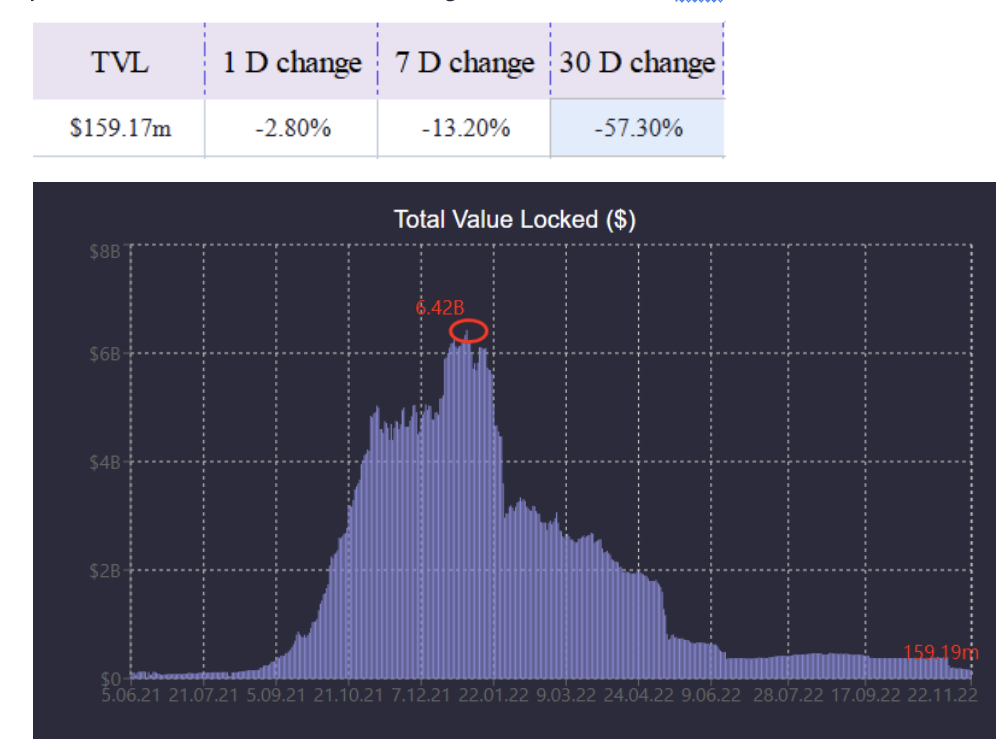

We first have a look at the TVL. Due to the bear market caused by UST and FTT, the TVL of Abracadabra fell over 57% this month. Before that the peak is $6.42B. At present, the TVL is $159.17m, among which 97% are on ETH chain.

Total supply of MIM is 688,417,710 and the holders are 5,348 now, but 66.4819% of the token are locked in one address, which is an anyMIM contract.

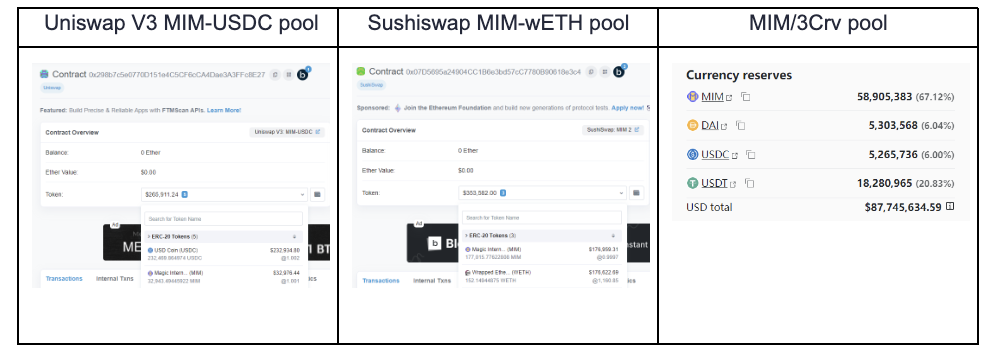

As for the liquidity on Ethereum mainnet, we find that in Uniswap V3 MIM-USDC pool, Sushiswap MIM-wETH pool and MIM/3Crv pool, the proportion of MIM is 12.4%, 50% and 67% respectively. All MIM in these pools are 59,115,342, so the proportion is 64% of the circulating supply.

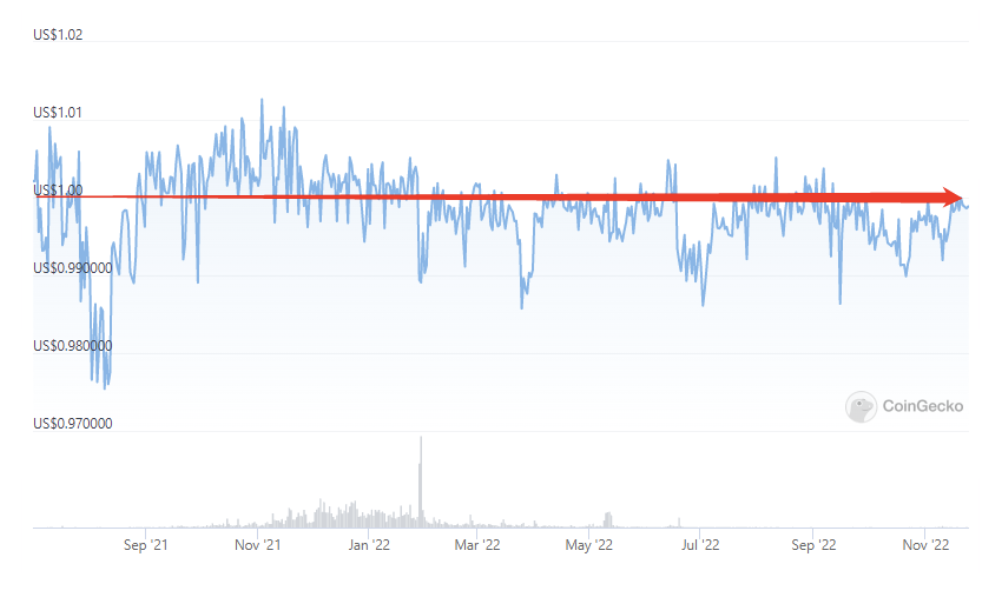

Warning! The risks of depegging still exist.

Depegging history of MIM

Most of the time, MIM is depegged from $1.00 as shown in the chart.

At last is another important point: capital utilization. we usually use ratio of volume and circulating market cap to stands for utilization, and the utilization of MIM is just 1.07%, while USDC is 8%. Also we can see the daily transactions are not much.

So we can say that MIM is definitely overissued just like UST.

3、Latest news

On November 22nd, 2022, the team announced the current status of operations and future plans for Abracadabra! Read more about it in the mirror article below:

We would like to select a few of points for analysis:

3.1 Treasury

The current treasury consists of:

6,213,784.085371 USDT

3,300,000.00 yveCRV-DAO (Which will be used to collect bribes and incentivize liquidity)

975,274.26576848 unlocked CRV tokens

371,233.839528 USDC

446,941,713 SPELL (Coming from Yearn bribes)

96.5 ETH

Another approximately 120k in other stablecoins

The total treasury value, at the time of writing this article, is $9,572,789.85.

The current treasury does not consist of MIM because they just used $4m MIM to repay the bad debt.

3.2 Bad Debt Repayment

The first tranche of bad debt repayment happened a few weeks back. They paid with protocol revenue and treasury funds. The bad debt has been reduced from an initial $12.5m MIM to less than $8.5m, actually is $8.16M(because of UST). There is still 30k MIM backed by FTT.

We get the debt ratio of Abracadabra is 85% now, which is not a healthy one.

$61.45M MIM was backed by stable assets, which is 66.45% of the total MIM borrowed. Other $31.03M guarantees are non-stable assets including WETH, BNB and BTC. It is worth noting that there are $2.1M MIM mortgaged by sSPELL.

So under what situation will the occurrence of insolvency happen?

Well, putting aside the failure of the strategy of Yearn, it depends on the difference between the value of these interest-bearing collateral and the current value. Take WETH for example, suppose the price at the time of staking was $1800 and the APY on Yearn vault is 8%. Then the user borrowed max MIM which is 90% LTV, so he got 1620 MIM. The current price of ETH is $1200, if he used these MIM to buy ETH he can get 1.35 ETH. He doesn’t want to repay. A outstanding bad debt happened. Solend and BendDAO have encountered similar situation. We think it is a good hedging strategy.

On the first day of each month, the treasury will repay approximately 5% of the bad debt, 425k MIM, to the UST cauldron. They have also increased the percentage of treasury protocol fees from 25% to 50%.Finally, the debt ratio will gradually decrease ideally.

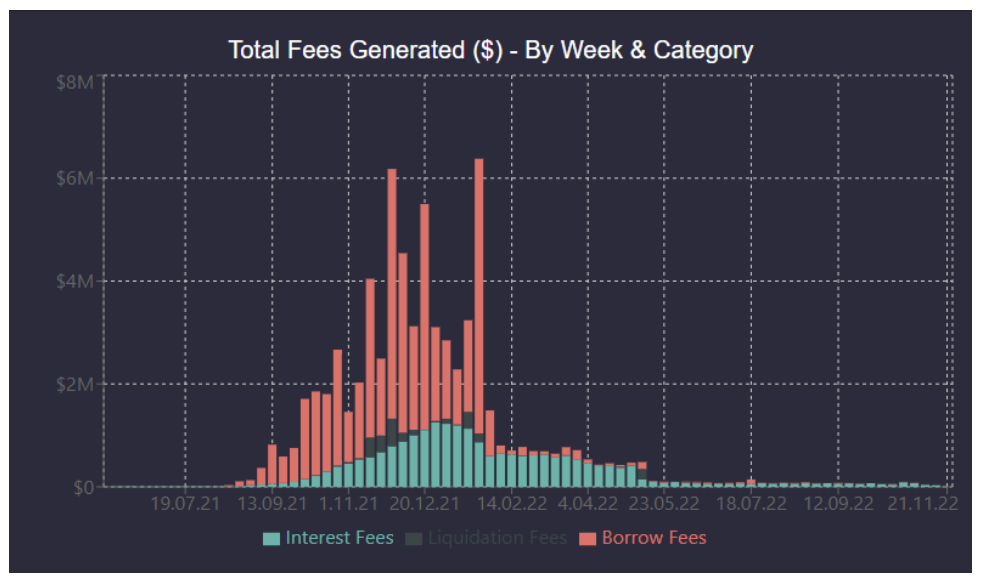

Then we see the fees earned by the protocol. Last week they got total fees of $23.91k. The total fees they earned is $97.75M, which is more than the total circulated MIM.

The picture below is the information about the debt repaid.

3.3 Team restructure

Abracadabra has recently undergone a restructuring of the team. Founder, Daniele is no longer an active member. Following this restructuring, the first actual change to the protocol operations will be a reduction in the emissions across the board. In a word, reducing emissions in the short-term will also reduce selling pressure on SPELL.

4、Token

SPELL is the native token of the project. The current use cases for SPELL include:

Staking: Users can stake SPELL to receive sSPELL for a share of the protocol revenue distribution. Protocol revenue is used to fund SPELL token buybacks at the market price, which are then distributed to the stakers.

Liquidity Mining: Users can provide MIM or SPELL to liquidity pools on DEXs such as Curve Finance and Sushiswap to earn SPELL and a share of the transaction fees.

Governance: sers will need to stake SPELL in return for sSPELL to vote on governance proposals.

You can stake and lock your SPELL to get sSPELL and earn more SPELL

As for AIP #10, 50% of the protocol revenue will be used to buyback SPELL tokens or distributed through mSPELL staking contracts, while 50% will be used to build up a treasury.

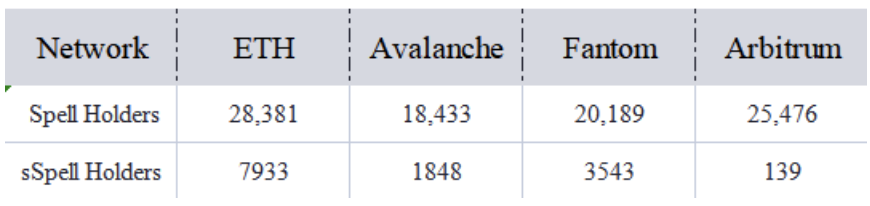

SPELL is launched on ETH, AVAX,FTM and Arbi now and the holders on each chain are almost the same. But the holders of sSPELL are just 28% of those of SPELL on ETH mainnet, so SPELL farming is not attractive to users.

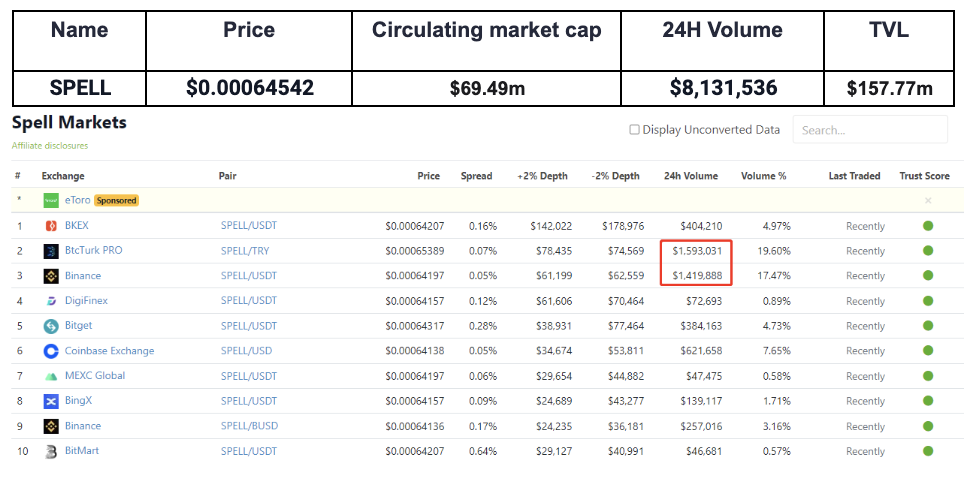

At last, we see the token information:

5、Summary

The project has the following characteristics:

For Product:

-The target customer group is relatively unique

-There are few competitors

-Interactive applications such as Yearn and Curve are relatively well-known

-Leverage farming is friendly to users

For Market:

-They have adopted effective and timely strategies every time the crisis comes

-They are committed to paying off the debt, which helps build customer loyalty

At last, what we can learn from Abracadabra team are:

For the liquidity:

-There are two reasons why users choose to hold MIM instead of putting them in the pool

-The pool is too shallow, they are worried that they won't be able to get out the token

-They are not motivated enough

For the bad debt:

-No matter what kind of assets are facing the risk of bad debts

-The value of main assets can be preserved using MIM

When you decide whether MIM and SPELL are good investment assets, please take the risks talked above into consideration.