Article by Jake And Stake Edited by Frank America

One of the oldest projects on Ethereum, MakerDAO created DAI, the original, decentralized stablecoin and has since established itself as the longest-standing DeFi lending protocol. After surviving the collapse of both the capital and crypto markets over a 36-hour period on March 12–13 2020, MakerDAO has proven to be one of the most resilient protocols in DeFi.

SPX (Trading View)

But Maker is not a company; Maker is a tech stack that offers a variety of products centered around the stablecoin DAI.

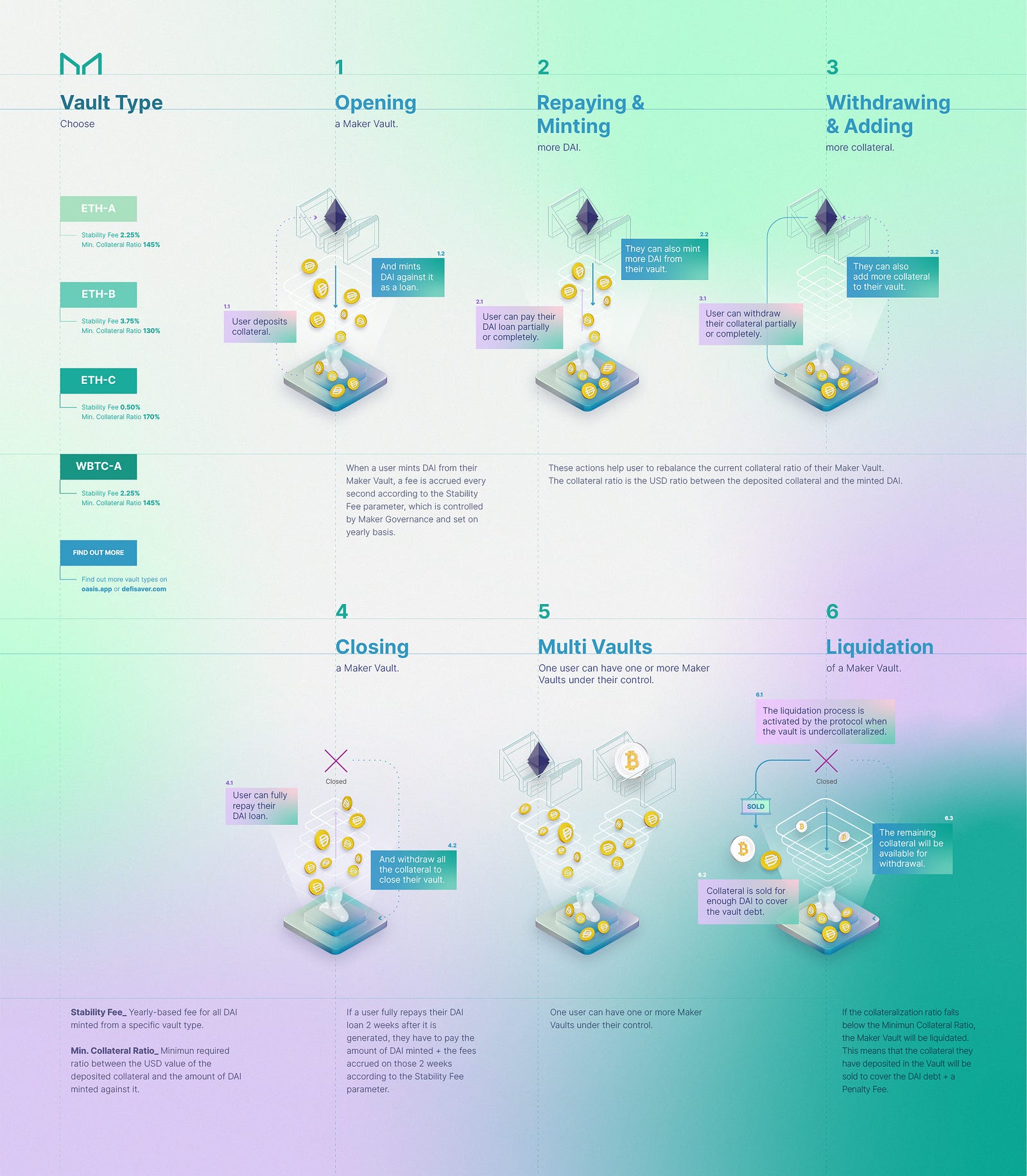

It all starts with Maker’s lending product: Maker Vaults. For the uninitiated, Maker uses its vault contracts to let users deposit collateral and borrow against it. Users deposit collateral and receive a loan in the form of DAI — Maker’s native stablecoin. If your collateralization ratio falls too far, your collateral is subject to liquidation and DAI must be repaid to avoid this.

DAI is an over-collateralized stable asset fully backed by crypto assets and Real-world Assets (RWAs) as well. The over-collateralization gives its biggest advantage, providing security for any DAI holders. But its most crucial feature is that DAI is fully decentralized meaning that it cannot be censored, so that’s an extra layer of safety for DAI holders.

— CORINA (MAKERDAO TEAM)

Maker generates fees in correlation with the amount of collateral deposited and reinvests those fees into the protocol. The entire system creates an upward spiral of value that feeds back into DAI and MakerDAO.

Maker is a tech stack.

Maker is incentivized to increase demand for DAI across as many platforms as possible (within the Ethereum ecosystem). This means increasing demand for DAI denominated debt positions, improving liquidity & capital efficiency, and reinforcing the strength of its peg through diverse collateral. Let’s get into how they’re doing that.

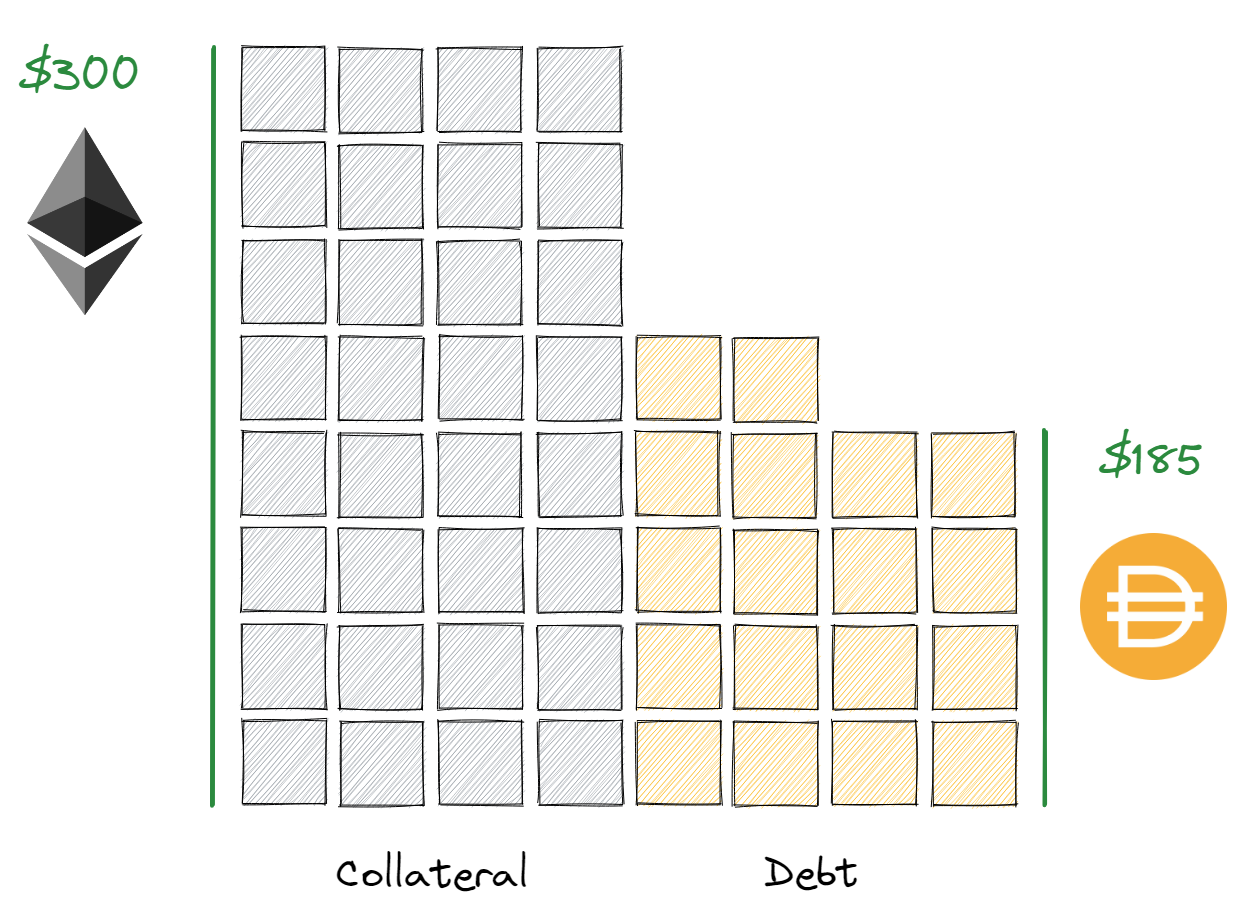

In order for users to mint multi-collateral DAI, they must first deposit their collateral into Maker’s vaults which are categorized by collateral type. As a result, the user creates an overcollateralized debt position denominated in DAI. There’s no due date for repayment, but if the collateralization ratio falls below the liquidation ratio, your funds are subject to requisition.

Collateral (grey) vs Debt (yellow)

During inflationary periods of an economy, the purchasing power of money (USD) decreases, meaning there’s a general price increase of goods and services. In such cases, holding assets can be safer than holding money, and productive assets even more so.

Once users have created their position, the generated DAI can be used for everyday activities, like buying groceries, paying off debt, or purchasing your favorite NFT. During periods of persistent inflation, the value of your collateral could increase compared to the value of the loan. If your collateral is more valuable in relation to the loan, you can increase your credit line or pay back your loan with less collateral.

As long as the DAI stability fee is less than the USD inflation rate, the cost of your DAI-denominated loan will fall; meaning the DAI you borrowed is worth more than the DAI you are required to repay.

At the time of writing, the stability fee for depositing can be 1.50%, 3.00%, or 0.50%, depending on what type of vault the user decides to use, ETH-A, ETH-B, or ETH-C, respectively, while USD is inflating at 8.5%.

As mentioned previously, productive assets are extremely attractive during inflationary periods — especially hyperinflation. Instances of hyperinflation throughout history include Zimbabwe in 2008 and Argentina over the past decade. During periods like these, productive assets are even more attractive.

Staked Ether (stETH) is one such productive asset. ETH has been coined the “internet bond” because staked ETH returns a practically risk-free, ETH-denominated yield from block production. This serves as an automatic increase in your line of credit. Not only will the value of your collateral increase compared to your loan, your collateral will also compound in ETH terms.

Stability fees according to makerburn.com by collateral type:

stETH-A (1.5%)

stETH-B (0%)

ETH-A (1.5%)

WBTC-A (2.0%)

MakerDAO

As the price of Ethereum rises, so will your DAI credit line. And if inflation is higher than the stability fee, your debt will be diluted away. This makes stETH an auspicious collateral because of its yield, making it productive ETH.

Borrowers can also increase their exposure to ETH. After depositing collateral into a vault, users can generate new DAI to buy more of the same collateral, using Maker’s vaults to benefit from inflationary periods. Users can then pay off their debt at more attractive prices.

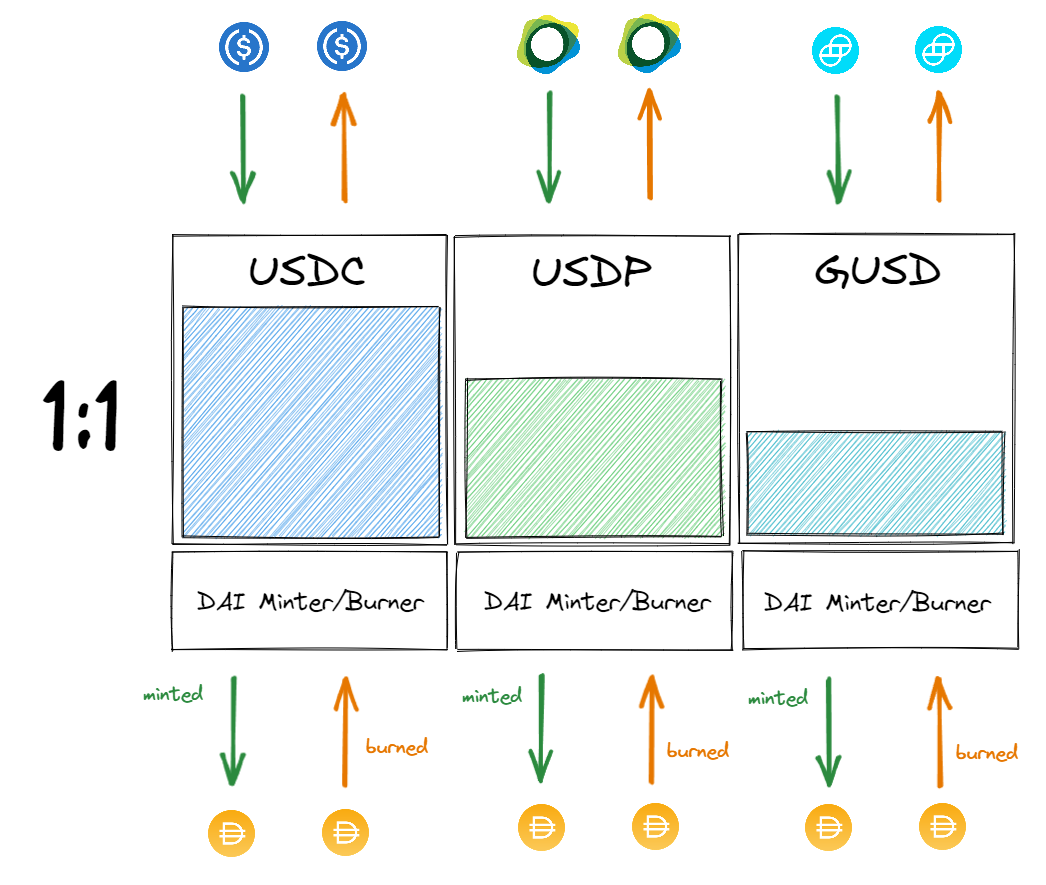

It’s important that DAI maintain its peg. If the value of DAI is volatile compared to 1 USD, users will not find it as attractive to use as a safe-harbor and thus not use Maker’s Vaults. That’s why MakerDAO provides mechanisms like the Peg Stability Module (PSM) to ensure that DAI is pegged to 1 USD.

Typically, if DAI is trading below 1 USD, Maker can increase the stability fee to incentivize users to repay their loans and subsequently increase demand for DAI. Similarly, the DAI savings rate serves to incentivize users to hold and deposit DAI, pushing the price back to 1 USD.

During events like Black Thursday, Ethereum prices fell 50%, leading to huge demand for DAI. This pushed the price of DAI to $1.10, well past the peg. The Maker community quickly voted to accept USDC as a collateral type, serving as a release valve for users to short the peg back down.

Afterwards, Maker voted to implement the Peg Stability Module (PSM). Users can deposit USDC and generate DAI at a 1–1 ratio, no matter the price. The constant one-to-one exchange allows users to arbitrage DAI’s price.

The PSM allows users to swap their stablecoins for DAI and vice versa. The DAO can receive a fee on swaps. This allows users to seize arbitrage opportunities in the market, when DAI is trading above its peg users can deposit other stablecoins to receive DAI at a 1–1 ratio (minus the swap fee which is currently 0) and sell it on the open market. Similarly for the inverse.

The PSM mechanism will tighten DAI’s range to its peg of $1 by acting as a release valve if the value of DAI swings too widely. Currently, the PSM holds 3.5 billion USDC.

MakerDAO

Under the hood, the module functions like a vault, but unlike other vaults all tokens inside it are owned by MakerDAO. This allows Maker to change the stability fee (0%), liquidation ratio (100%), and swap fee.

As a result of the PSM, all of the USDC in Maker has been deposited by users to arbitrage stablecoin prices. The PSM is a new feature of the DAI tech stack that the market finds extremely useful.

Users can access the PSM through 1inch, Paraswap, or the interface created by one of MakerDAO’s community members, found here.

Maker has a similar mechanism for DAI borrow rates. In order to increase demand for DAI, borrow rates must be low enough to be attractive and high enough to be profitable, but sometimes secondary lending markets’ rates are not optimal. That’s where D3M comes in.

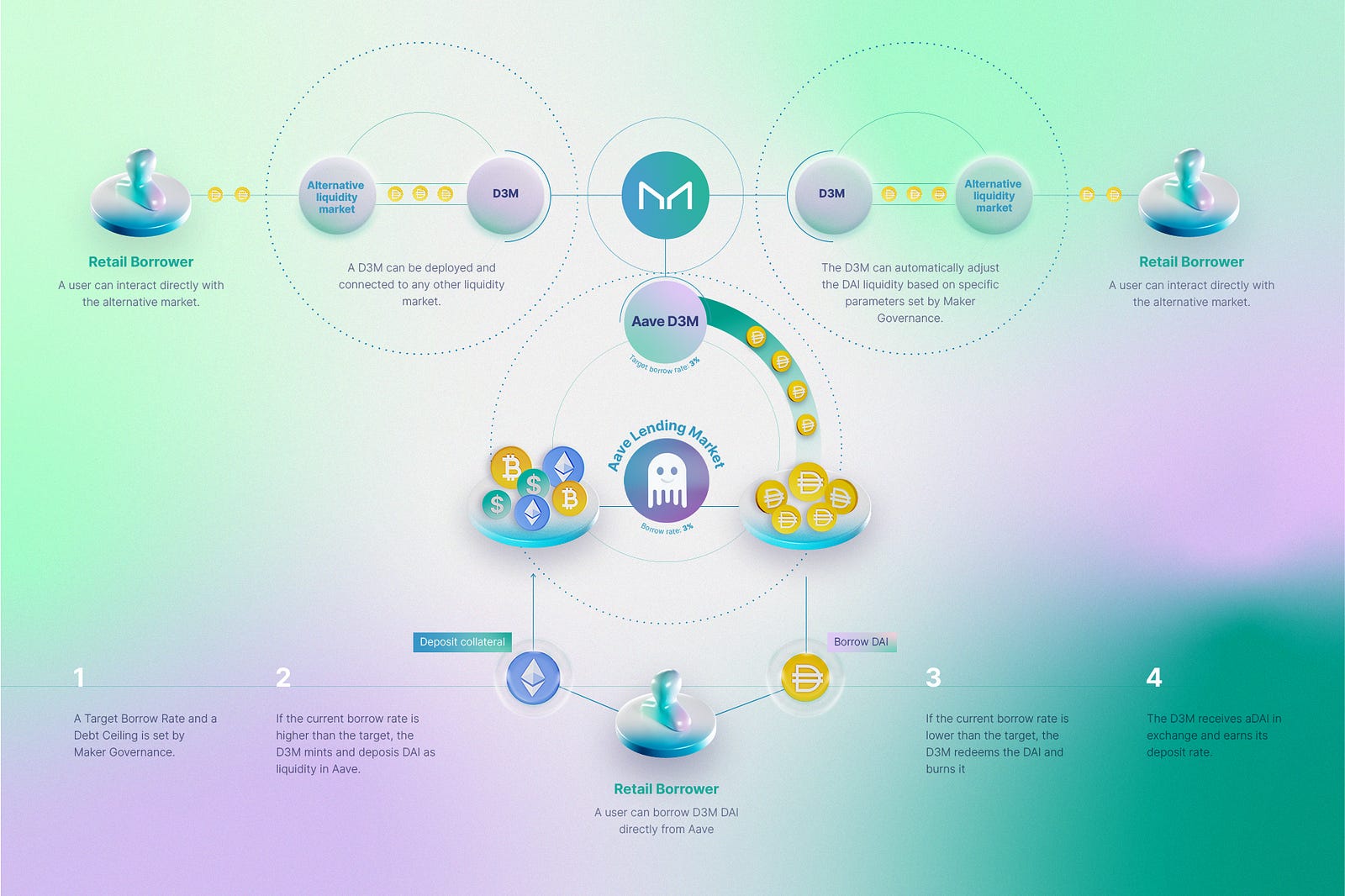

How the Direct Deposit DAI Module can help stabilize the variable interest rate.

D3M is Maker’s “Direct Deposit DAI Module”. D3M is a new feature that will allow Maker to supply liquidity to and remove liquidity from secondary markets (like Aave) algorithmically. MakerDAO governance sets a parameter called the “Target Borrow Rate”, which determines the borrow rate “equilibrium” that D3M wants to maintain. This allows Maker to stabilize the variable interest rate of DAI on these markets, thus creating predictability for borrowers and lenders. These reduced fees incentivize demand to borrow DAI.

By algorithmically expanding or contracting the supply of DAI, Maker can optimize demand and revenue and earn fees based on borrow-demand. Additionally, this earns the protocol rewards from the secondary market’s liquidity mining incentives, thus increasing Maker’s governance rights in these markets.

D3M allows these lending markets to become distributors of DAI throughout whichever L1 and L2 chains they exist, further stabilizing DAI’s variable interest rate, which makes DAI more attractive to large institutional investors and borrowers.

MakerDAO

How does it work?

Users deposit collateral into Aave.

If the borrow rate for DAI on a Aave is higher than Maker’s target rate (liquidity is low), D3M will generate DAI collateralized by Aave’s liquidity pools (ETH, WBTC, etc).

That DAI is deposited in Aave, generating $aDAI, earning the same rate Aave provides to its users. This reduces the borrow rate, incentivizing demand to borrow DAI.

The generated $aDAI goes to D3M.

If borrow rates are too low, D3M will withdraw DAI from the pool to maintain equilibrium. Reducing supply and pushing borrow rates up.

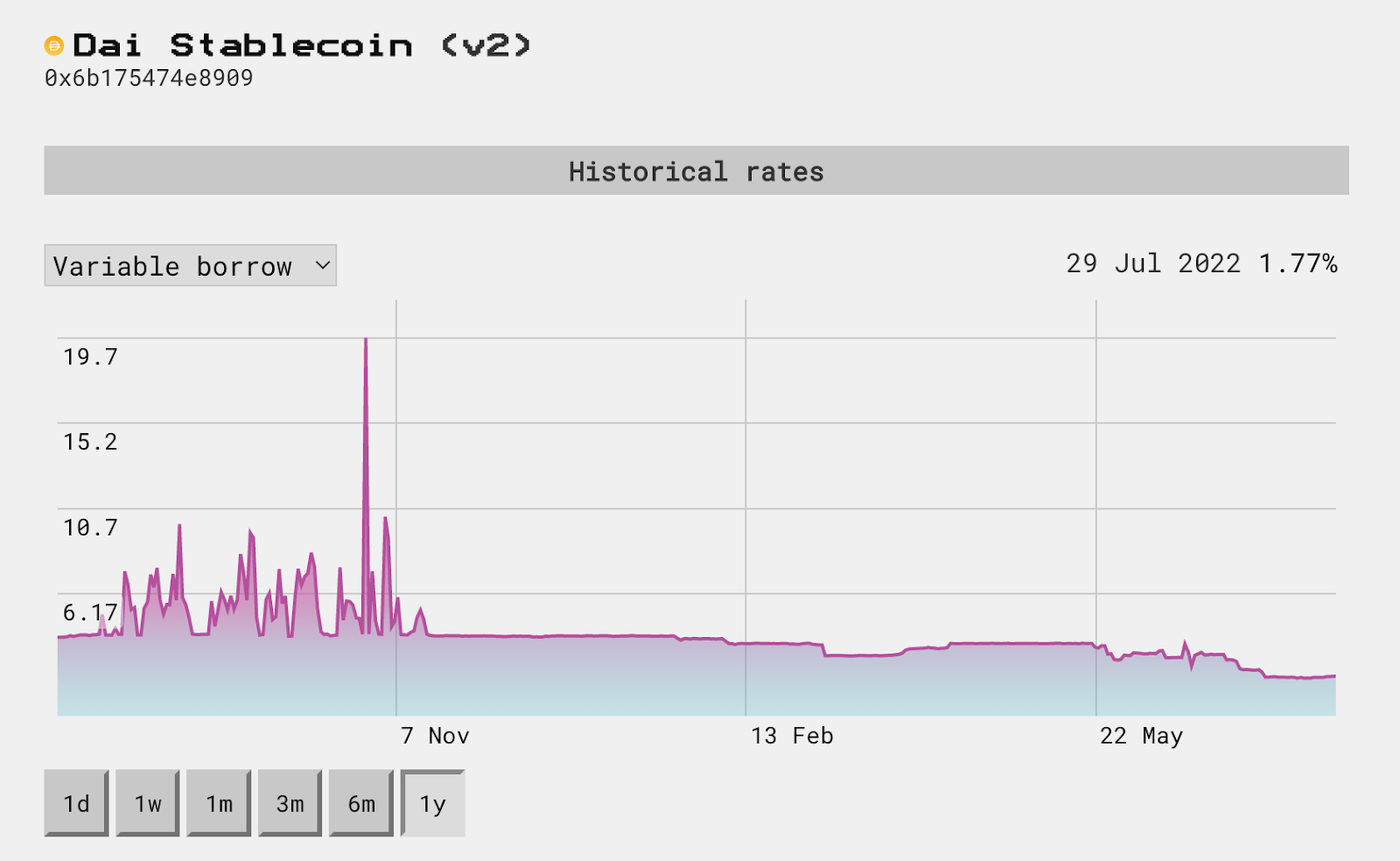

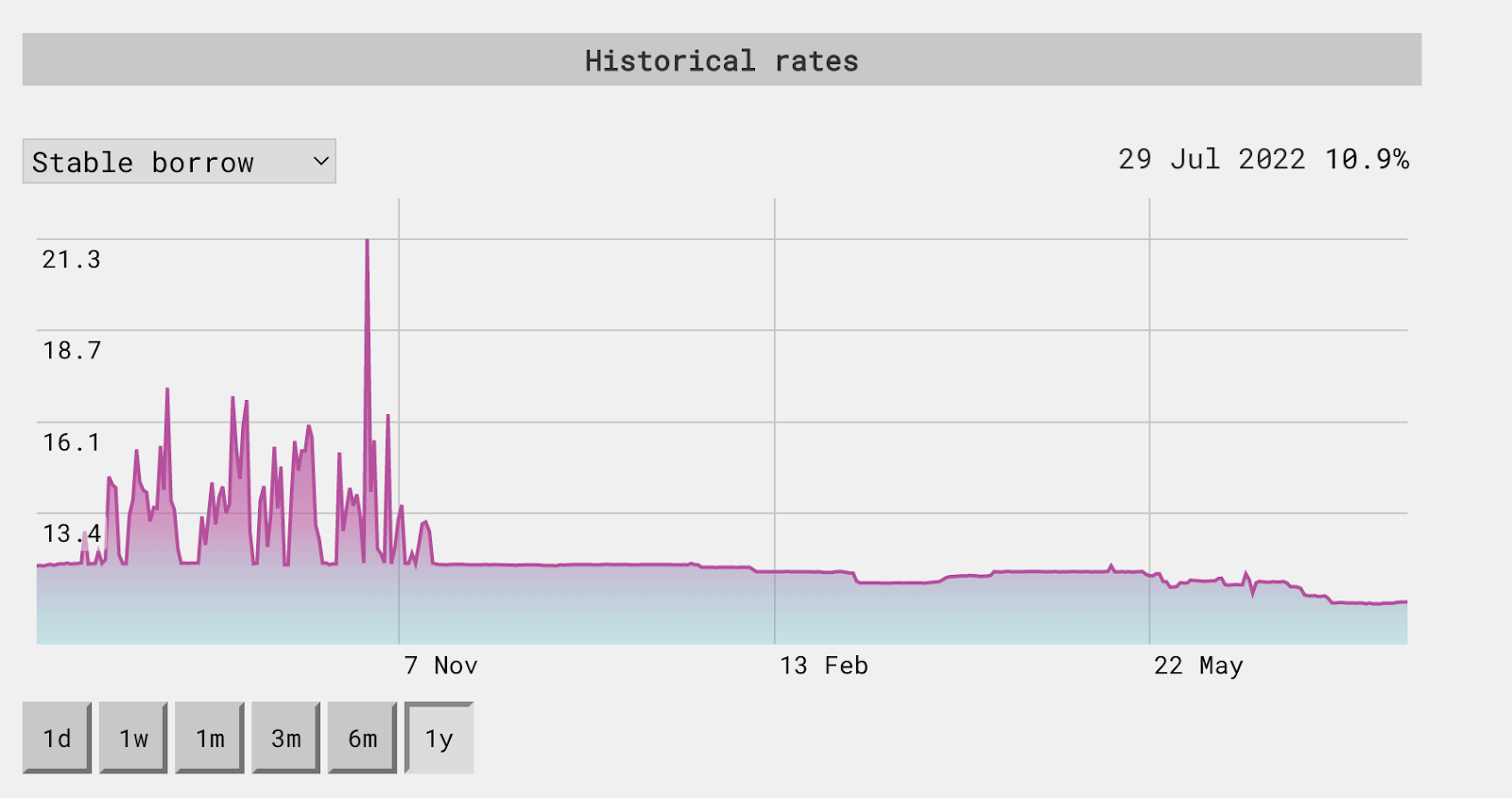

The efforts have been effective. Since its launch in November 2021, DAI variable borrow rates have stabilized to a range of 1.7% to 3.8% on Aave. The results are similar for the stable borrow rate.

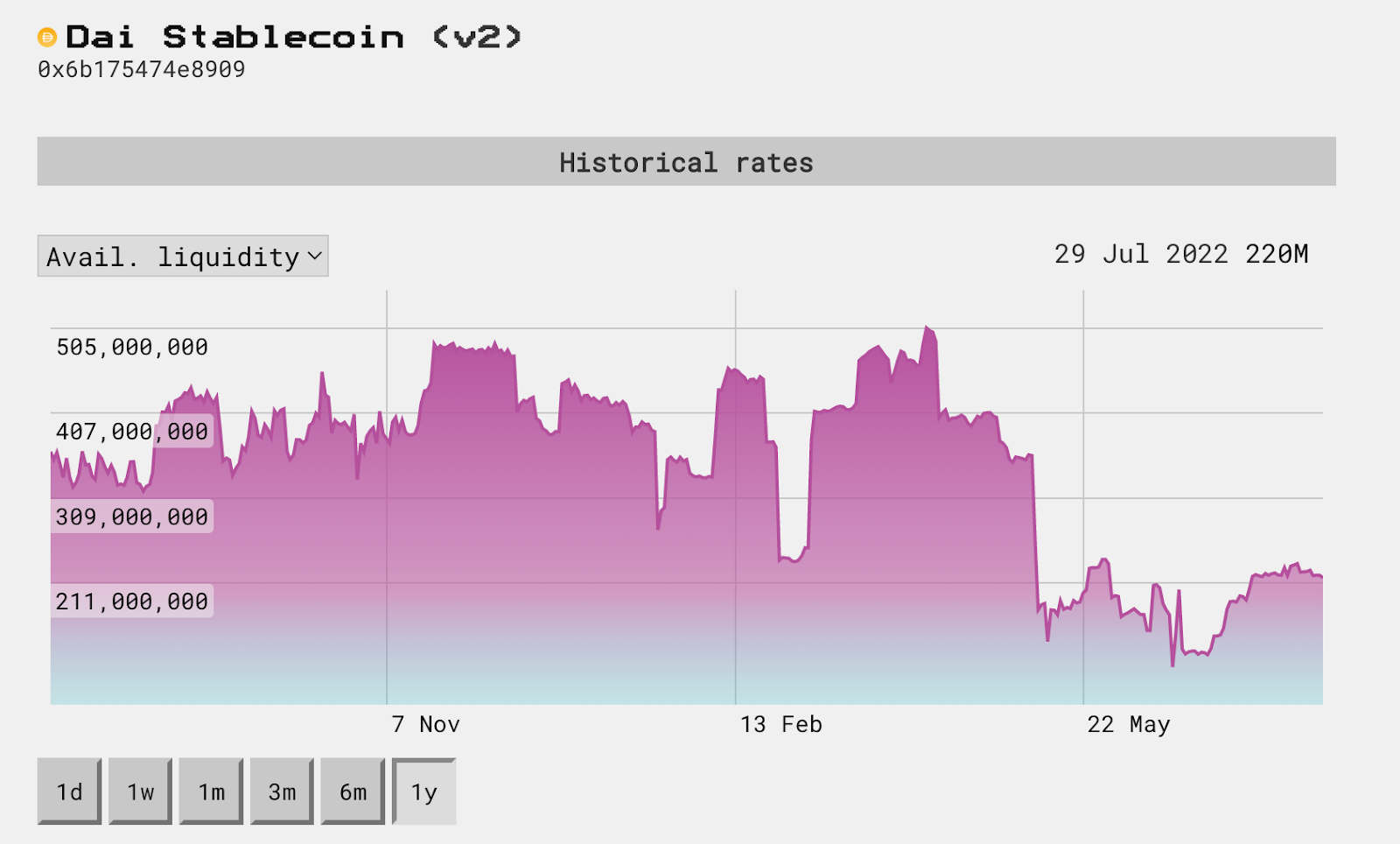

You can see an increased variance of liquidity as a result of algorithmically stabilizing the borrow rates. Note that liquidity was affected heavily by large market drops in January, February, and May. Maker also turned off the D3M system connected to Aave during the ETH-stETH depegging event in order to manage the risk posed by Aave’s exposure to stETH.

Maker is the only protocol that has the ability to inject and remove DAI liquidity to/from secondary markets algorithmically. Protocols get a plug-and-play experience with the D3M to adjust DAI borrow rates quickly.

“Maker is the only protocol that can inject and remove DAI liquidity algorithmically.”

With D3M, Maker becomes a wholesale creditor for other protocols. Even though, at the time of writing, Aave is the only protocol with a D3M deployed, a Compound D3M will be deployed soon, and you can imagine several specialized protocol’s integrated with Maker similarly (Maple, TrueFi, Centrifuge, etc.) D3M allows Maker to scale their credit facility across protocols with different core competencies than itself.

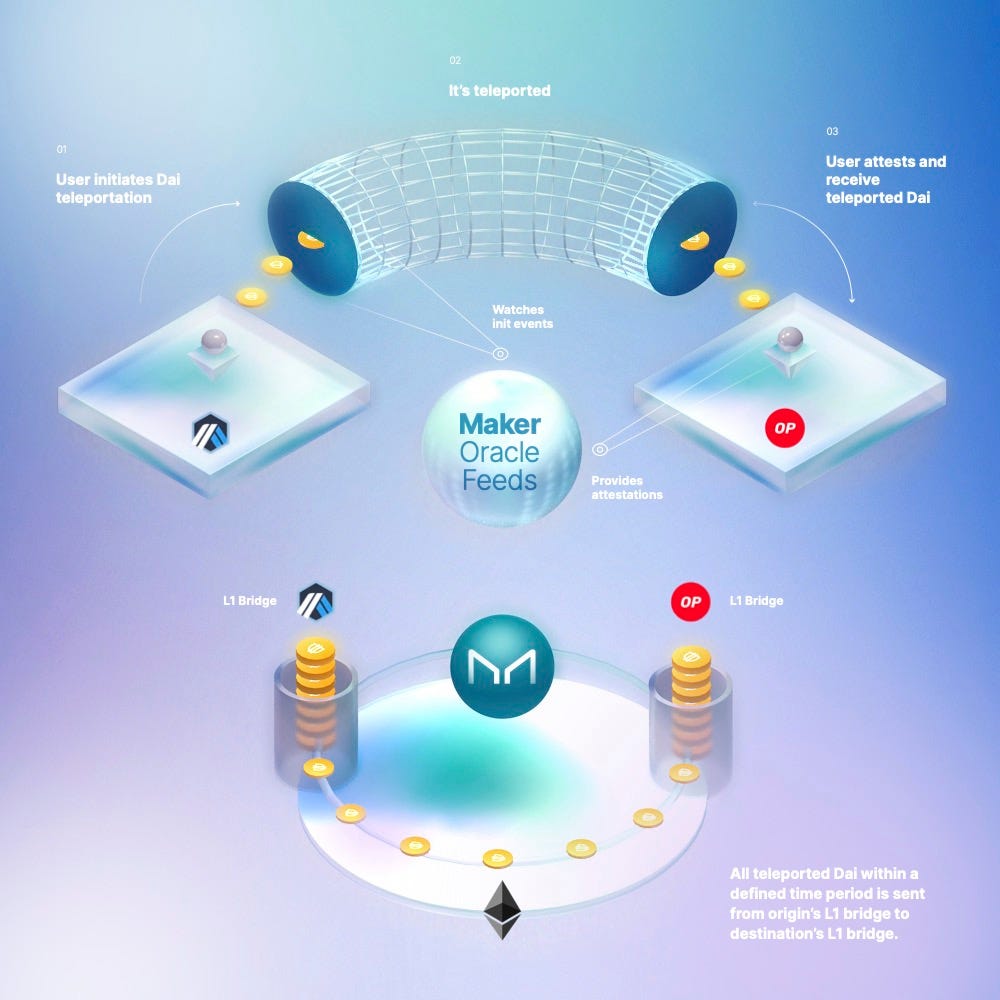

Still, D3M isn’t the only way for DAI liquidity to spread to the multichain world. Maker is developing a novel bridging mechanism to expand DAI’s reach.

How teleports will reduce gas fees and enable fluid DAI movement across L2s.

Maker will allow users to bridge between L2 solutions faster and more efficiently than other stablecoins. Bridging from chain to chain is cumbersome and costly, as users must interact with L2 bridges and wait for their transactions to settle on each layer:

L2-A → L1

L1 → L2-B

Maker will utilize a burn and mint contract on each L2 to enable users to move funds without waiting for the typical settlement times. This will reduce the friction of bridging across ecosystems, with transaction finality improving drastically. Optimistic rollups can take 1–2 weeks, while ZK rollups can take just a few hours.

When users want to initiate a teleport from L2A → L2B, they will send their DAI to the L2A bridge contract where it is burned. This event generates an attestation that users can provide to the minting contract on L2B, withdrawing their DAI. To account for the DAI moved from one chain to another, DAI will be transferred across bridge contracts on Ethereum L1.

Teleport allows DAI users to have canonical DAI on a variety of different L2s with faster withdrawals than typical settlement pathways. This will also be more gas efficient. DAI will not be moved piecemeal — per transaction — but will instead be transferred in batches, reducing gas costs. Instead of multiple drivers traveling alone, they carpool with each other and save on gas.

https://twitter.com/TheRugNews/status/1543700665548935168?s=20&t=P1Wz27uBoUX90i3dFco-5Q

This approach increases DAI’s liquidity across the Ethereum ecosystem, making it more attractive to users as the default stablecoin. The increased demand will further accrue value to the MKR token in a similar manner as above. The more debt is denominated in DAI, the more demand there is for DAI to service those debts.

Maker’s ambitious bridging strategy will also make borrowing with vaults more capital efficient and will lower users’ fees. By minting natively on L2 rollups, users will save gas leading to a direct reduction of costs. Users can enter and exit positions at lower costs than they would on Ethereum L1.

The reduction of costs will also make it feasible to offer vaults that use different collateral types. In the past, Maker had to off-board the use of certain collateral because the costs were too high.

https://twitter.com/MakerGrowth/status/1449406582404550665

But now Vaults can use the reduced L2 fees, drastically reducing the cost to maintain oracles for these collaterals.

Within the next couple of quarters, MakerDAO is planning to fully deploy the Maker protocol (MCD) on other Layer 2 chains — such as Arbitrum and Optimism. This is an important step in the Multichain Strategy Roadmap.

— CORINA (MAKERDAO TEAM)

Rollups are also expected to increase transaction throughput by a factor of 100 by way of ZK rollups. This will improve vaults by increasing the oracle update speeds and decreasing costs thus allowing Maker to issue loans at lower minimum borrow requirements. All of this together will improve the liquidation experience, reduce minting and repayment times, and allow users to move easily from one chain to the next.

As Makers L2 strategy continues to be built, it proves to be hugely beneficial to users. Cheaper fees, faster transactions, and unparalleled security across several chains differentiate Maker’s DAI from other stablecoins.

If you’re interested in a deep-dive into Maker’s multi-chain strategy and its mechanics, check out this article detailing their partnership with StarkWare.

Finally, Maker is diversifying its collateral methods by using Real World Assets (RWA):

Another vital part of the Maker expansion plan is accepting real-world assets tokenized on-chain as collateral in the Maker protocol. Two examples we can bring in here are the 20M loan provided by Maker in DAI to SG Forge (subsidiary of French bank Societe Generale) and the recent 100M loan deal with Huntington Valley Bank.

— CORINA (MAKERDAO TEAM)

Let’s dive into how Real World Assets (RWA) factor into the MakerDAO roadmap.

One side effect of leaving a bull market is that the demand for leverage decreases, but as prices go down, traders and market actors look to stablecoins as a safe haven for their wealth. The problem here is that the DAI supply is largely a function of demand for Maker’s loans.

As a result, Maker enabled the PSM, a permissions liquidity tool that accumulates USDC and saves it as a liquidity reserve for DAI. This has exposed Maker to counterparty risk (a la Circle) and regulatory risk from the US government.

Still, the demand for stablecoins can increase past the supply of other stablecoins and crypto-collateral alone (even “blue chips” like BTC and ETH). The demand to leverage long is not high enough for Maker to supply the DAI necessary for the market’s demand. This is where RWA comes in.

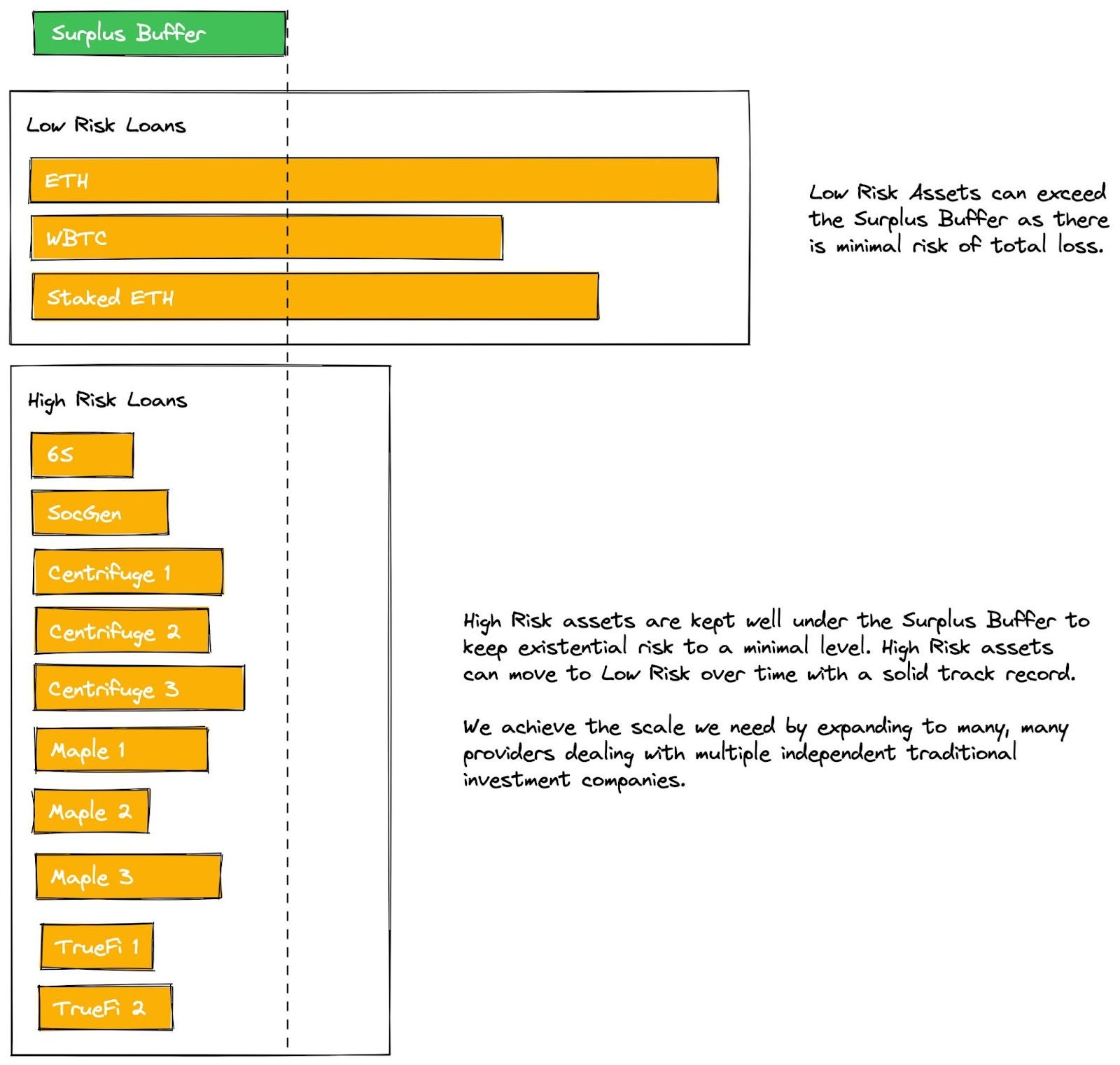

Maker found themselves in a position where they held a lot of USDC, but the assets weren’t compensating for the small amount of risk they have or contributing to profitability. But if Maker could deploy these assets into productive, low-risk, yield-bearing assets the protocol would have another revenue stream.

In an effort to explore this opportunity, Maker has begun to onboard new collateral types. This has expanded beyond cryptocurrencies and into real world assets (RWA). The new collateral also improves the security posture of DAI because RWA prices are not as highly correlated with cryptocurrencies as cryptocurrencies are with each other. For example, when BTC falls, so does ETH, but this is not the case with housing bonds which are generally unaffected by crypto price movements.

The move to onboard RWA is an effort to expand into productive assets that are uncorrelated with the majority of DAI’s collateral. This move serves to diversify Maker’s portfolio and allow them to have a surplus of assets that will allow the protocol to mint more DAI and take risks without existential threats to the system.

Aggressive Growth Strategy (hexonaut). Part of Maker’s “Aggressive Growth Strategy ‘’ is to use this surplus buffer to hedge against bad debt incurred by fast downward price movements.

Maker has had its sights set on RWA as early as March 2020, with their first foray into the industry being a collaboration with French Bank Société Générale:

“Société Générale’s investment arm, SG-Forge, is raising a $20 million loan through MakerDAO’s DeFi lending protocol to refinance their on-chain covered bond issuance backed by real estate, called OFH tokens.

“Obligations de financement de l’Habitat” (OFH) tokens roughly translates to “housing finance bonds”. Since then the deal has progressed further with MakerDAO voting to create a new vault type (RWA-008) that will have a 30 million DAI debt ceiling with a stability fee of 0.05%.

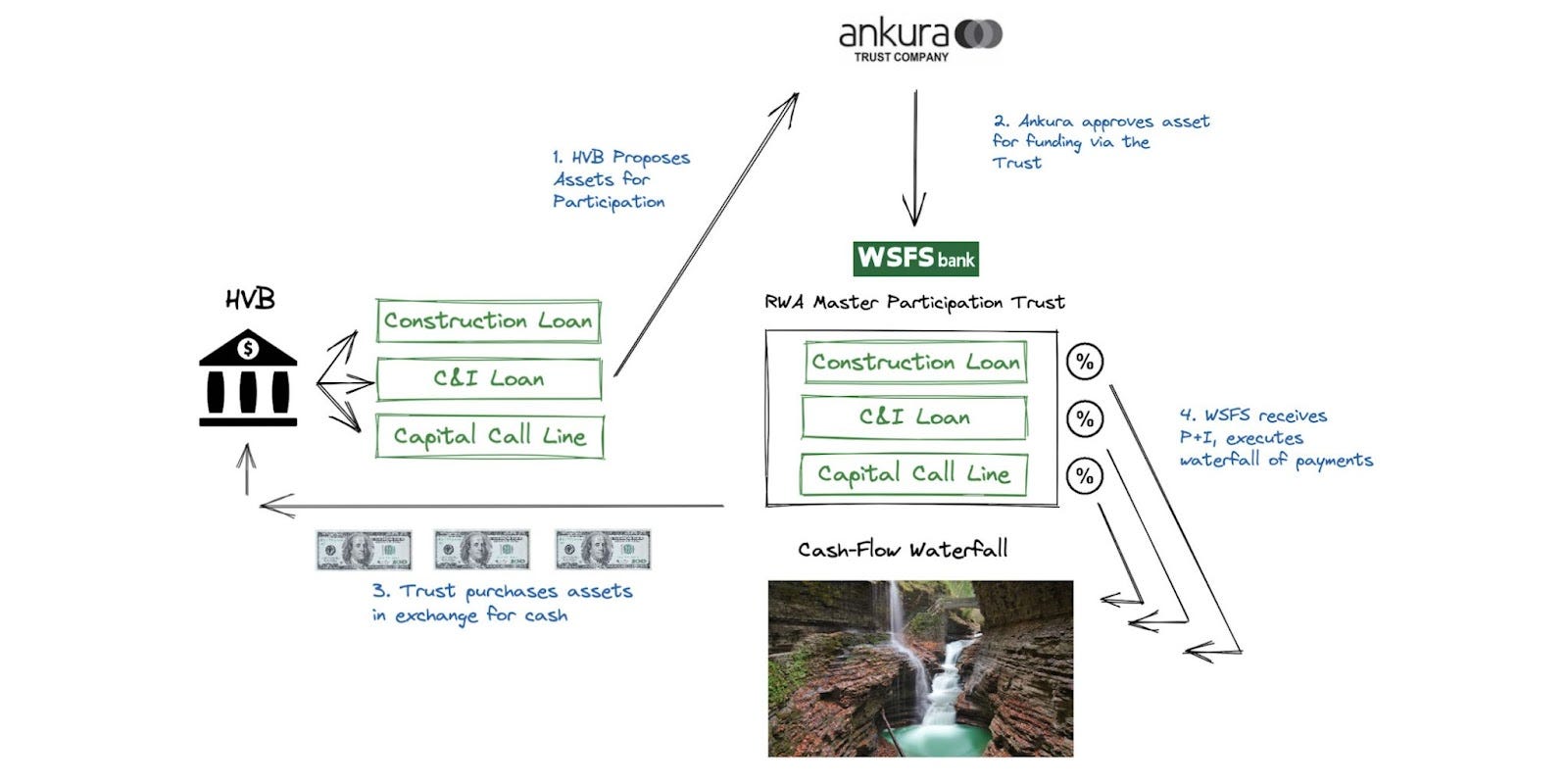

In that same proposal, Maker created a similar vault for Huntingdon Valley Bank with a 100 million DAI debt ceiling and stability fee of 0%.

Huntingdon Valley Bank (HVB), a Pennsylvania-based community bank, has entered a partnership with Maker where HVB will originate loans for commercial mortgages, construction financing, business loans, etc and Maker will give HVB access to DAI liquidity in exchange for a share less than or equal to 50% of the value of the loan and claims on its interest. Maker is represented by the RWA Master Participation Trust which will distribute payments accordingly.

In the above example, Ankura Trust (an independent loan assessor) verifies the loan of which a share is given to Maker’s Trust in exchange for cash. This is the first large-scale partnership between a regulated US bank and a DeFi protocol, the result of which is Maker’s entrance into wholesale lending and access to real world assets, broadly and at scale.

Note that HVB is not borrowing assets from Maker, but is instead selling these assets to the protocol via the Maker-controlled trust. In exchange for USD converted from DAI, Maker receives access to RWA cash flows and TradFi assets.

This expansion represents more than just increasing the security of DAI. It transitions Maker from a purely retail DeFi banking system into a wholesale DeFi banking system. It allows Maker to enter larger financial transactions. These transactions may come with higher risk, but that risk is mitigated by partnering with expert wholesale entities.

RWAs open an entirely new market to Maker and serves to diversify the longest standing stablecoin in DeFi: DAI. These are battle-hardened smart contracts that have a new market, new collateral, and expert financial analysts backing an already irreplaceable money lego.

Real World Assets diversify the longest standing stablecoin in DeFi.

Maker has created products and formed partnerships to increase DAI liquidity throughout the Ethereum ecosystem. By way of D3M, Maker can directly inject DAI liquidity to secondary lending markets, decreasing loan rates and increasing demand. This desire to borrow DAI is supercharged by Maker’s wormhole bridge and multi-chain strategy. Making vaults available across various chains will make DAI available to new, cost-conscious users, increasing demand further.

Maker’s biggest competitive advantage for lending is having the lowest rates in DeFi. As the issuer of DAI, the protocol does not pay third party liquidity providers for capital and acts as a primary market lender for the other lenders in the ecosystem […] Maker is highly secure, relying on an automated Dutch liquidation system as well as its own price oracles.

— CORINA (MAKERDAO TEAM)

The more prevalent DAI is, the more utility is needed for it, further increasing demand. Maker is supercharging this by allowing DAI to be accessed across a variety of lending platforms and chains. But Maker is also capitalizing on its strong position by diversifying its collateral with atoms (RWA).

In using RWA as collateral, Maker is strengthening DAI’s ability to maintain its peg and creating opportunities for Maker to enter other markets. All of this serves to increase DAI utility, strength, and availability. Subsequently, this demand creates a surplus of value that is fed into the MKR token.

“The Maker protocol is akin to a living system that adjusts its behavior to what the market needs. In bear markets, it can shift to hold mostly fiat backed stables due to market conditions. In bull markets, users want to use leverage, and the protocol subsequently holds much more ETH and wBTC than any other collateral.”

— MARIANO DI PIETRANTONIO (MAKERDAO TEAM)

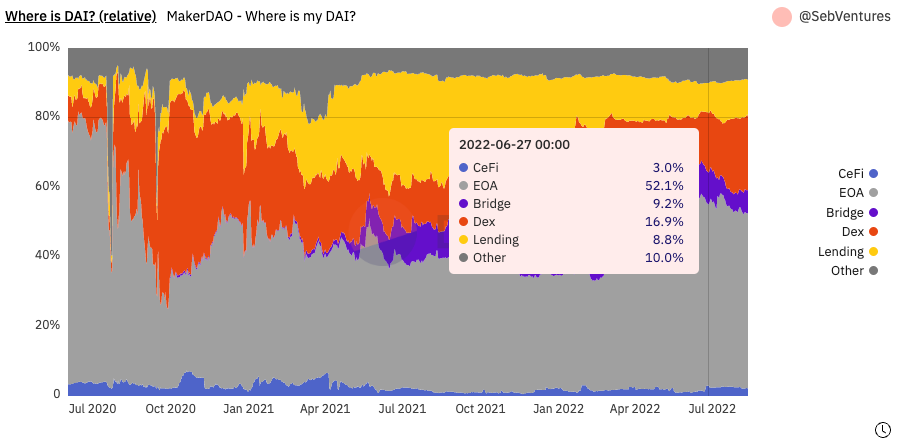

DAI is decentralized in another fashion: distributions. More than 50% of all DAI in circulation is held by externally owned accounts (EOA); in other words plain-old wallet addresses. This statistic indicates that DAI has organic users that believe in its stability, resilience, and decentralization.

Most recently, Maker has demonstrated its resilience as Celsius fell. Before filing for bankruptcy, Celsius took out a loan from MakerDAO, and while many of their creditors are owed funds, MakerDAO is not one of them. Celsius had to pay back the loan in order to get their collateral back. Maker is the equivalent of a senior creditor, but not because of enforcement by the law, but by code. Maker’s smart contracts have superseded the need for a court system and government intervention.

DAI has seen it all, and Maker is moving in the right direction on several fronts. Maker is not a company. It’s a set of systems that serves to make DAI the most abundant, demanded, and innovative stablecoin in crypto.

Special thanks to Corina Dolghier, Mariano Di Pietrantonio, Cristobal Garcia, and Frank America for their feedback.

Author Bio

Jake and Stake is a writer and editor at BanklessDAO. He is the creator of and contributor to the DeFi Download, with a background in software engineering and cybersecurity.

Editor Bio

Frank America is an author, comedian, musician, and narrator. He is the Co-founder of The Rug, and a content manager for Bankless Publishing.

BanklessDAO is an education and media engine dedicated to helping individuals achieve financial independence.

This post does not contain financial advice, only educational information. By reading this article, you agree and affirm the above, as well as that you are not being solicited to make a financial decision, and that you in no way are receiving any fiduciary projection, promise, or tacit inference of your ability to achieve financial gains.

Bankless Publishing is always accepting submissions for publication. We’d love to read your work, so please submit your article here!

More Like This

MakerDAO Lets Money Grow on Trees by Kalex1138

Canonical DAI Stablecoin Upgrade by Zero Mass

MakerDAO Paradigm Bending Bridging Solutions on Starknet by Jake And Stake

Subscribe to IndyPen CryptoMedia

Over 19k subscribers

IndyPen CryptoMedia publishes a wide range of web3-related content written by independent authors.