2021 Fintech Predictions

A topic I really care about is financial equality and inclusion as well as income disparity. And that's why I care about fintech - fintech is not going to solve the world's problems, but it can certainly help those excluded or exploited by existing financial systems.

As 2020 comes to a close (okay it's a couple months away but 2021 could really not come faster) it really got me thinking about what is happening in the fintech space and where I think it's going in the future.

These might seem really obvious after you read but I find that most things seem obvious to me after I read them, so perhaps it can still be somewhat educational!

Firstly, I'd like to address one huge overarching theme:

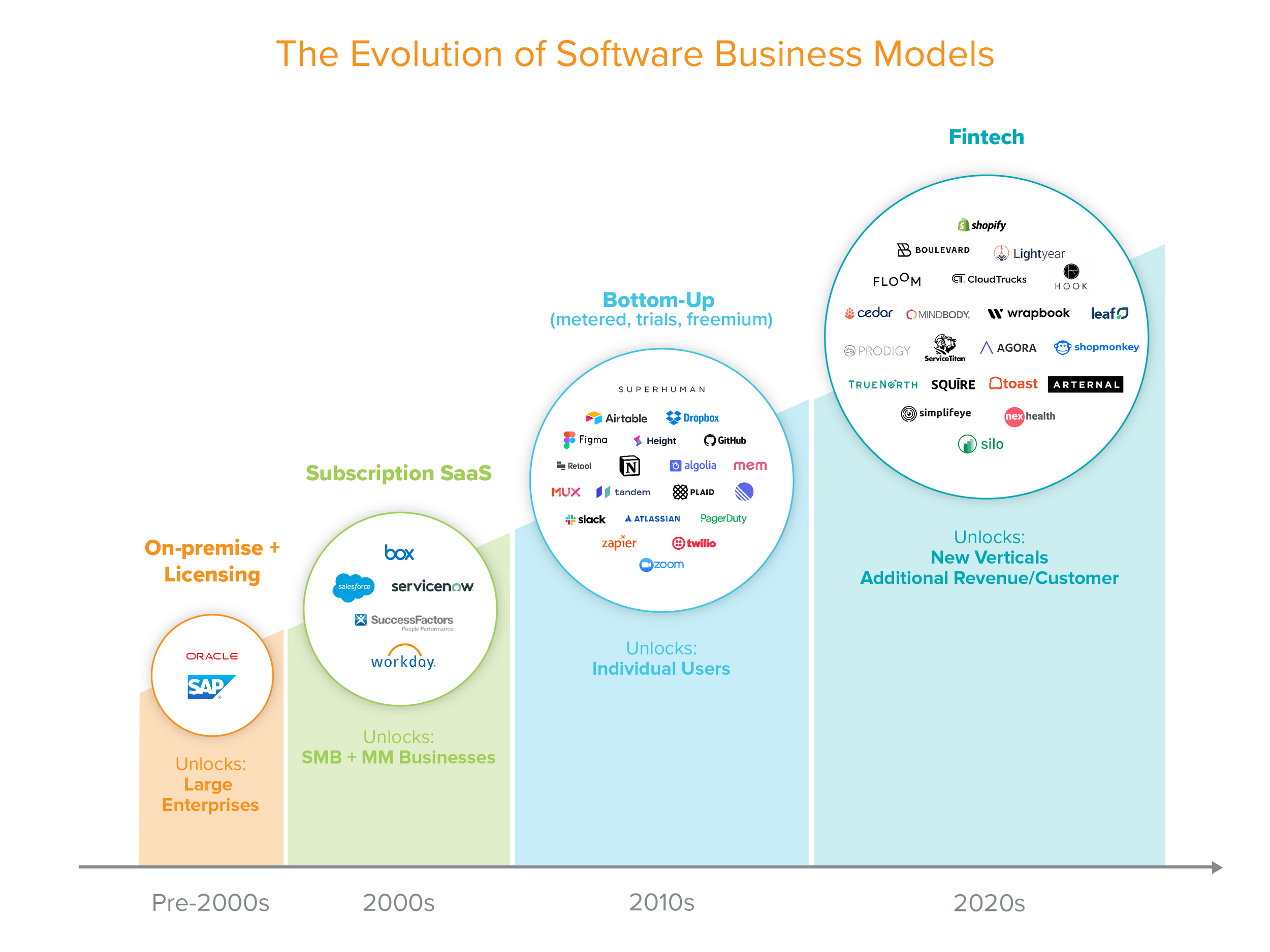

With the onset of the digital age, we've seen the classic rinse and repeat of unbundling and rebundling - newspapers got unbundled by blogs, CDs were unbundled and sold individually, and now healthcare is being unbundled by digital providers.

Basically, large incumbents build a great company on the technology of that time. But then underlying technology changes, such as the arrival of the internet and social media. Then the incumbent is challenged to keep up and stay ahead of the times, or else new and hip startups with nothing to lose will start doing a small segment what you do, but better... and steal customers.

Banks used to have every financial services available in the 90s and 2000s. But then we saw Lending Club ($322 million market cap as of 10/28/2020) and Robinhood (worth $11.2 billion) take one piece (lending and investing) from big financial services firms and get really good at it.

But consumers at the end of the day don't want 50 finance apps on their phone - hence the rebundling that I posit. Companies that have unbundled some services successfully will start consolidating via M&A or building new products to cross sell to customers. Rebundling is worth because it means more revenue across new products such as insurance and investing.

For example, M1 Finance is trying to become a finance "super app" by bundling several banking products together (sounds like... Ant??). We saw Visa acquire Plaid for $5.3 billion, and now face anti-trust scrutiny [1/12/2021 update: Deal Terminated]. We saw Intuit acquire Credit Karma for $7.1 billion and also now face antitrust. We also saw NerdWallet acquire Know Your Money and Fundera both in this year of 2020.

As companies consolidate, there will always be antitrust concerns from the DoJ.

But all in all, fintech rebundling is good - because it will challenge incumbents to get even better at what they do (survival of the fittest!). For example, we recently saw JP Morgan launch a new QuickAccept service with free fast funding for SMBs (like Square). Jamie Dimon is showing that fintechs won't be the only ones to monopolize new trends. Goldman Sachs also launched APIs so that clients' developers can build on their platform and embed Goldman's services. This is mutually beneficial because it allows Goldman to also move into transaction banking aka broaden the firm's revenue streams. Legacy banks are moving into the banking-as-a-service space!

I personally think that fintech rebundling will be mostly driven by large fintech companies like Chime or Stripe because they have a lot of money. They may acquire new fintechs that have a found a wedge in a new segment but haven't found a way to monetize yet. This brings me to my second point:

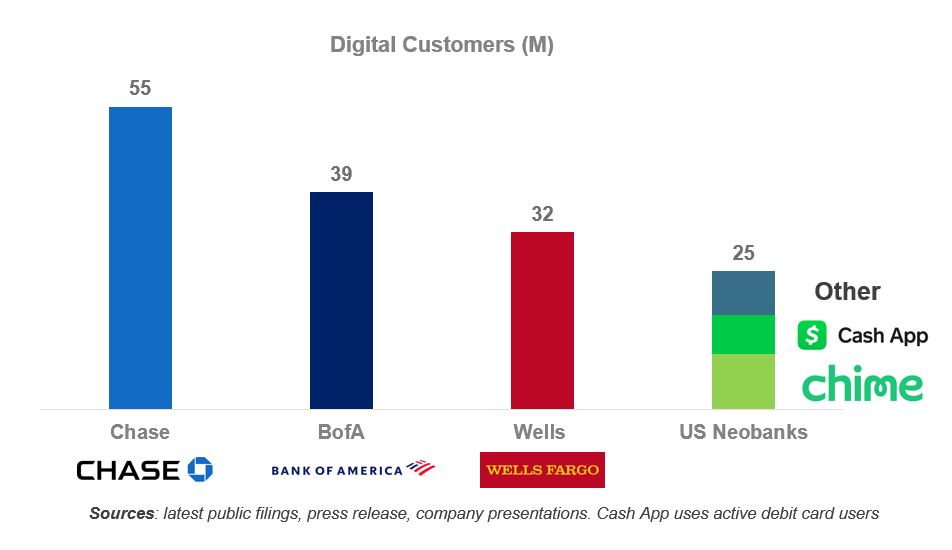

In 2019, Chase, Bank of America, and Wells Fargo added 5 to 6 million digital accounts total. In contrast, challenger neobanks added 10 to 15 million.

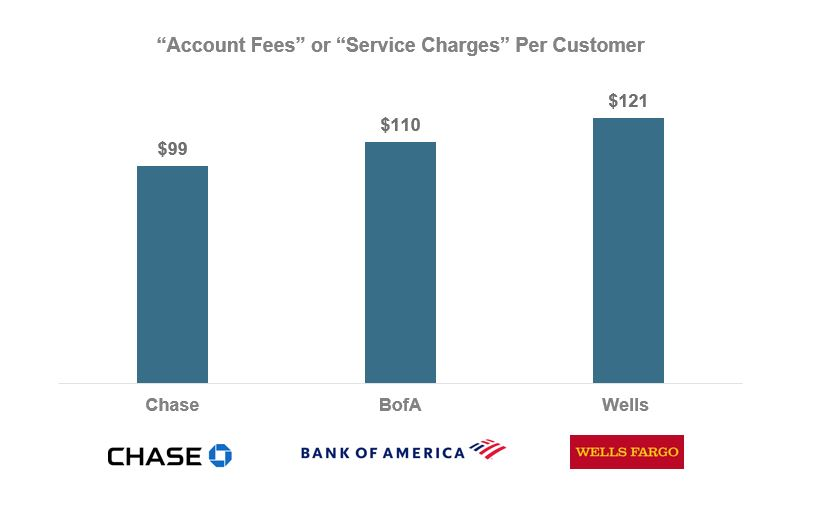

But they're charging quite a bit (overdraft fees, inactive accounts, minimum balances, etc.)...

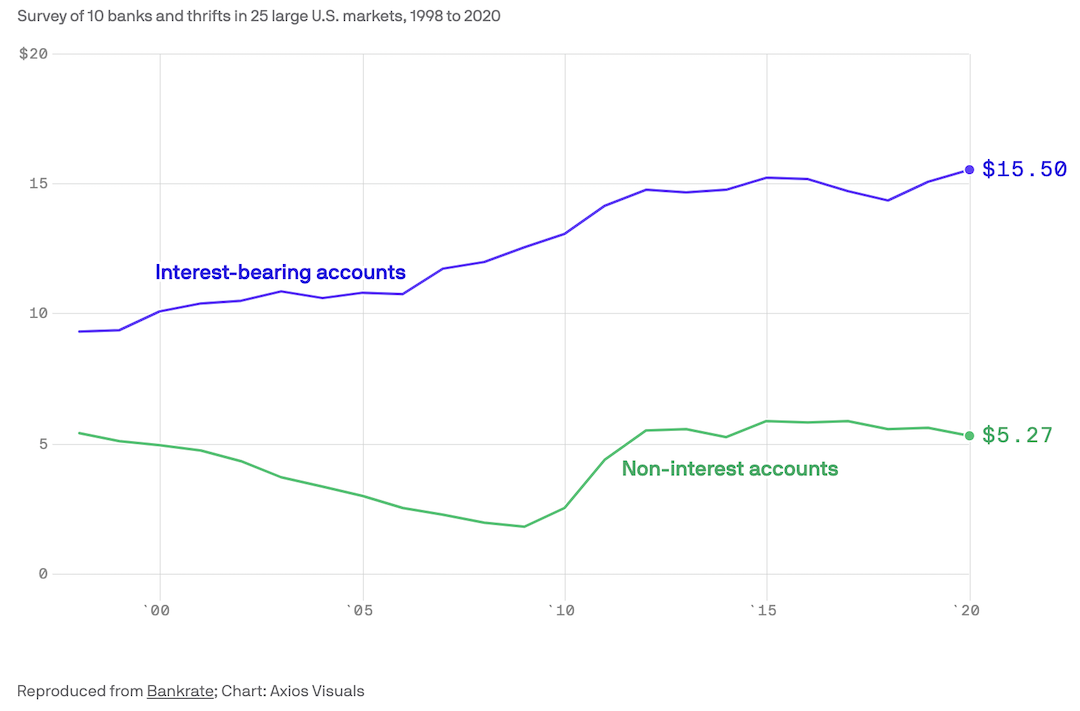

...while paying super low interest!

I want to first define what a neobank is before diving into them.

Click here to skip ahead if you already understand

A neobank is a company that offers a limited suite of banking products and does not have a brick and mortar presence. Basically, they're digital only, except that they may have physical cards for you to use at ATMs etc. And they don't have to be a bank - in fact most are not because it takes a long time to get a banking license! They offer banking products.

To dive into it a little bit more, neobanks existed to unbundle the banking value chain. A bank is just a semblance of regulatory infrastructure, UI/UX, and middleware layers to keep everything working together. Each step can be built in-house or rented. Legacy banks offer a bajillion services such as checking/debit, wealth management, investments, loans, wires, etc. These services obviously come at a cost.

Neobanks then come into the picture by taking a very select number of services/products and offering a superior experience, usually in the form of an app, with simple UI/UX that legacy banks cannot compete with. Because they only focus on a few services, they can really provide their digitally native users the best experience, such as with rewards programs, lotteries, etc. Their costs are also usually a lot easier.

The neobank space is incredibly noisy and saturated. Practically a new one pops up every day that is claiming to own one banking product and offer the best experience with a new metal card. So what distinguishes one?

Is a neobank able to find the right customers? Their whole existence is dependent on finding and retaining the specific customers they're targeting - if there isn't enough volume then they need to charge fees (perhaps subscription) to make the numbers work.

Short Caveat on the Durbin exemption

Neobanks became popular in the beginning because like the DTC consumer space, they could reach the customer at a much lower cost and thus transfer cost savings to consumers by not charging all the ridiculous legacy bank fees. However, now that the space is so saturated, neobanks need to pivot and think about how to generate additional revenue. Perhaps it is through offering investment or insurance products. They don't have to make everything in-house, but they do need to increase their product suites to retain target customers and boost their profits. If they can do that and distribute these products with the best experience, they will pop off! Another option is to offer embedded financial products, which brings me to my next point:

a16z

Consider fintech as an ingredient for technology businesses instead of being just a business model itself. That's embedded finance! Embedded finance is attractive because it unlocks new revenue opportunities at very low marginal costs, assuming the company already has customers. Customers can have better experiences and thus repeatedly use that company's product and purchase. Companies can own more of that customer relationships.

Amazon - you earn points to reinvest in the Amazon business. They've also dabbled in checking accounts I believe.

Uber - you use the Uber card and its point to have a seamless experience from the customer and driver's point of views.

Gusto - recently launched wallets, a great move as they already have customers and data so offering benefits through employers' customers aka moving into managing customers' financial wellness and perhaps moving into lending seems like a natural response... at a very low CAC for them.

Moov - open-source infrastructure for businesses to send, receive and store customers' money, rebuilding banking infrastructure for our cloud-native world. They're building a developer-first, modular for customization banking-as-a-service (BaaS lol) platform.

Stripe. Square. Shopify. Obvious ones. And some of the biggest.

Airlines - often offer travel insurance.

Lambda School - provides an income sharing agreement (ISA), where students' future income is charged rather than an upfront tuition. Interesting to consider if the ISA opportunity has shifted given employment struggles nowadays.

If you can abstract the components of payments, banking, and insurance into tech that is embeddable, it allows literally any merchant to provide better financial experiences for their customers at a low cost. If you already have a huge volume of data on your users, you basically have 0 CAC, 0 marginal distribution costs, and natural cross-selling. Integration and monetization come naturally at that point.

Legacy financial providers gotta watch out!

Anyways, one embedded finance vertical I am particularly bullish on is:

Why lending? Well companies can drive revenue at almost 0 CAC by distributing loans. Loans can be offered on the spot when someone needs it. And lending can reinforce engagement and retention loops, thus driving more brand loyalty.

Basically, lending has a high upfront capital cost but its economies of scale prospects are incredible.

It takes a LONG time to launch a lending product. A lot of people don't want to get into lending because it could really decrease margins. Loan funds often come out of free cash flows, which can limit other parts of the business.

However, an embedded lending company spreads out its infrastructure costs across multiple partners and thus sees costs greatly decrease with scale. This drives their profitability, something a brand trying to build an internal lending business might never achieve.

Obviously reaching the scale needed to achieve profitability is hard. But if they're able to aggregate data across many similar partners, that is true power!

One vertical of embedded lending is POS lending.

We've all heard of Affirm, Klarna, Sezzle, etc. POS lending was very innovative several years ago. But these companies were able to churn out very sticky relationships with customers and merchants, create excellent partnerships, and create higher conversion rates for customers at checkout. A very positive feedback loop for all stakeholders involved.

This form of lending is very exciting and will continue to challenge traditional lenders of the past!

I'd like to quickly spotlight Afterpay, which has teamed up with Westpac to launch its first savings account in Australia.

And I'd like to spotlight Lunar, a Nordic bank that started off in personal finance but acquired a full banking license and is moving in to the 'buy now pay later' space (note that Varo took 3.5 years to acquire its banking license). Sounds like cross selling and consolidation to me!

Like I said earlier, fintech is important to be because it allows antiquated financial systems (but very important ones) to be accessible and usable by more people. What I've mentioned above is mostly in the US with a sprinkle of Europe. But I think that Africa, Latin America, and SE Asia are HUGE opportunities. I personally am less well versed in this area but I am really excited to learn more and absolutely anticipate more big companies coming from those areas or more fintech companies entering those markets. The companies based there I expect will either grow independently consolidate with current large fintech players (obviously). For example:

Stripe acquired Nigeria's Paystack for $200 million this month (October 2020) to increase their reach.

Tala is based in CA but is building loan products for the Kenyan market and now operates in the Philippines, Tanzania, Mexico, India, etc.

Jumo is a B2B company co-founded by Salomon Brothers alumnus Andrew Watkins-Ball, building predictive data products for the 1.7 billion people in Africa excluded from access to financing.

Klar is based in Mexico and is a bank providing a digital and secure alternative to traditional credit/debit services. Like a neobank.

Konfio is based in Mexico as well and provides unsecured working capital to SMB.

Nubank is based in Brazil and is a neobank. They are the largest fintech in LatAm!!! They're valued at $10 billion!

Grab was started in Singapore and started as a taxi-hailing app but now provides transportation, food delivery, digital payments, and more across Southeast Asia.

Momo is a digital wallet and payment service based in Vietnam.

These target markets are some of the fastest growing in the world. They can't be ignored!

And now moving onto the very very last thing I'd like to touch on - crypto, because I can't help myself:

Paypal launched crypto and is planning to expand it into Venmo. Paypal has also invested in several crypto startups.

Libra and Telegram have failed to come to fruition due to regulatory reasons but nonetheless are incredibly important for crypto's publicity and education.

Paradigm's founders are incredible. Absolutely amazing so cool cannot stress enough!

Singapore's Project Ubin should be coming to a close soon.

China is still developing its digital currency but honestly might get there quite a bit sooner than we all expect.

Polkadot, a blockchain interoperability project built on Ethereum focused on enabling others to more easily build their products, and also a community I'm part of, has market cap is almost $200 million. Bet you didn't know that we co-exist with another huge international borderless market!

Overall, having crypto/decentralized blockchain co-existing in our very polarized and regulated world sounds like an oxymoron in itself. There needs to be some catalyst or breakthrough to make this all "mainstream". Not quite sure this will happen in 2021. But I am optimistic about the future - I do see pressure coming in internationally!

Please read my piece on crypto here if you'd like to learn more 🙂

Will startups distribute before incumbents innovate? That has always and will always be the big question.

I expect more (1) fintech and especially neobank rebundling, and an increase in embedded finance, especially in (3) embedded lending will occur in 2021. (4) [X] for Africa/LatAm/SE Asia is already here but I anticipate a much bigger focus on it.

Just the embedded finance market is worth over $7 trillion in 10 years time, 2x the combined value of the world's top 30 banks today. There are huge revenue opportunities and platform loyalty upside. You really just can't ignore that.

You also can't ignore this space with news that Ant Group has won approval from Chinese regulators for the Hong Kong leg of its IPO. Yahoo rallied 30% in the 3 months before BABA's IPO. Ant won't be listed in the US, but you bet that its presence will be just as big if not bigger! Retail investors already placed bids for a record $3 trillion of shares in their HK IPO. TRILLION! Wowza. (read my piece on Ant here)

💡

11/3/2020 Update: Regulators have halted the HK listing of Ant. "Ant said in a statement to the Hong Kong stock exchange that its offshore share offer had also been suspended because the company “may not meet listing qualifications or disclosure requirements due to material matters relating to the regulatory interview of our ultimate controller, our executive chairman and our chief executive officer by the relevant regulators and the recent changes in the fintech regulatory environment."

Oh, and of course also an (5) optimistic overtone of more crypto education and PR for the world. Because what would this writing of predictions be without a trend some people are super pessimistic about? 😉