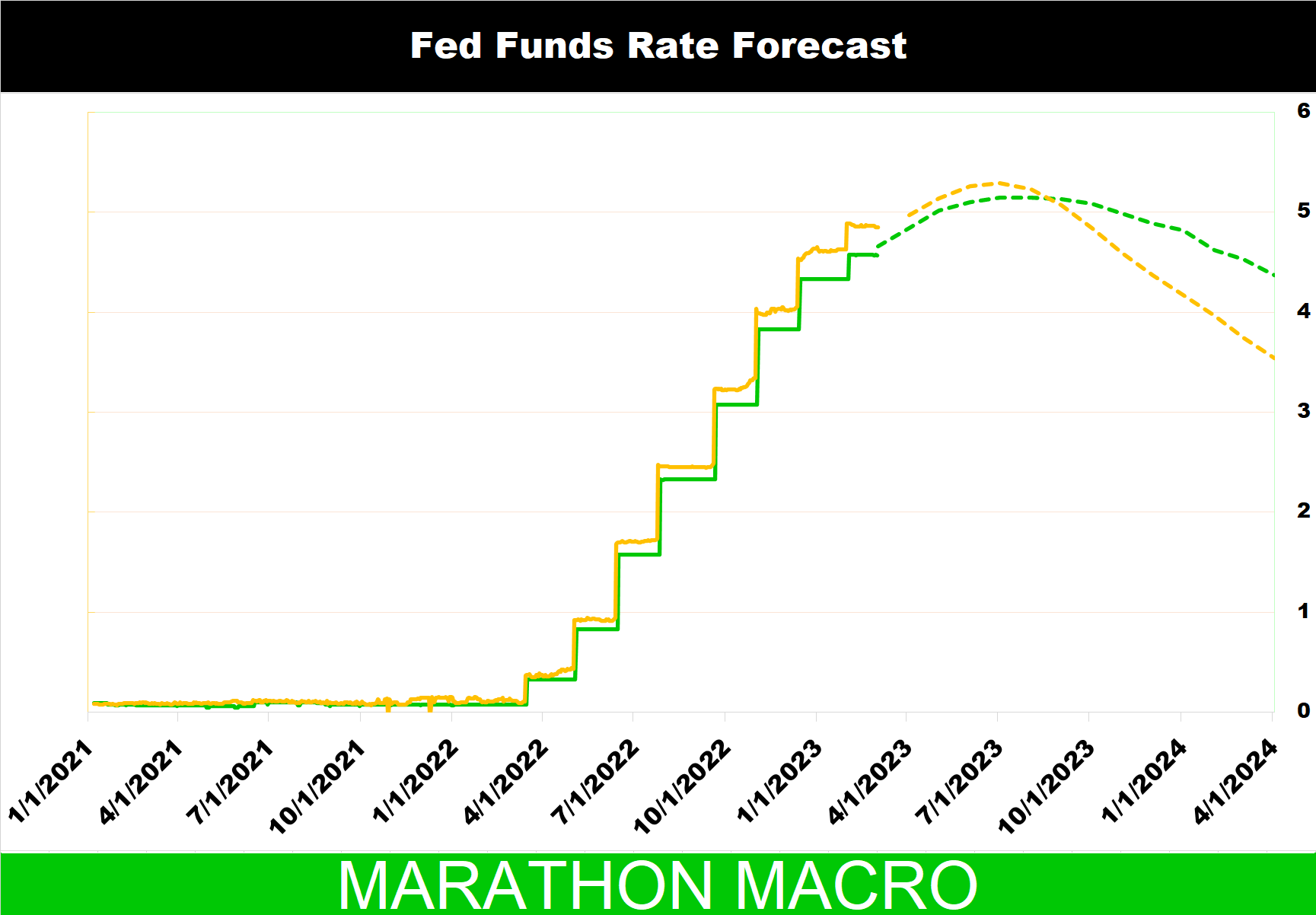

The low interest rate environment following the 2008 financial crisis created a situation where banks faced a difficult challenge. The traditional source of revenue for banks, lending money to borrowers, was no longer yielding the same returns it once had. With the Federal Reserve keeping interest rates at historically low levels, it was difficult for banks to earn a decent return on their loans. This prompted banks to seek alternative sources of revenue to maintain profitability.

One such alternative was securities investments, particularly AFS securities, which provided higher yields than traditional lending. Banks were attracted to the flexibility that AFS securities provided. These securities could be easily sold if conditions changed, without the need to revalue the entire portfolio, as would be necessary with HTM securities.

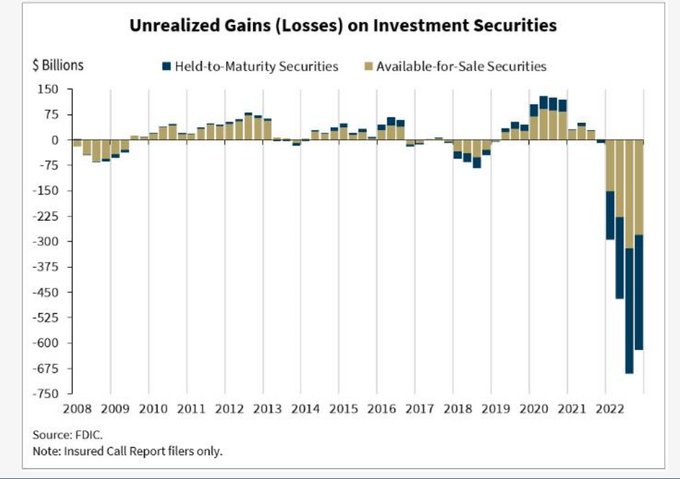

However, this flexibility came at the cost of increased volatility and risk. AFS securities are marked-to-market, meaning that they are valued based on current market conditions. This creates an element of volatility in a bank's capital base, as the value of these securities can fluctuate rapidly. The regulatory capital for banks with over $700 billion in assets is directly impacted by the volatility of available-for-sale (AFS) securities[1]. AFS securities are financial assets that are not held for trading or held to maturity, but rather are intended to be sold in the future. The value of these securities can fluctuate based on market conditions, which can lead to volatility in regulatory capital for banks[1].

Bob Bank and Amarii Bank

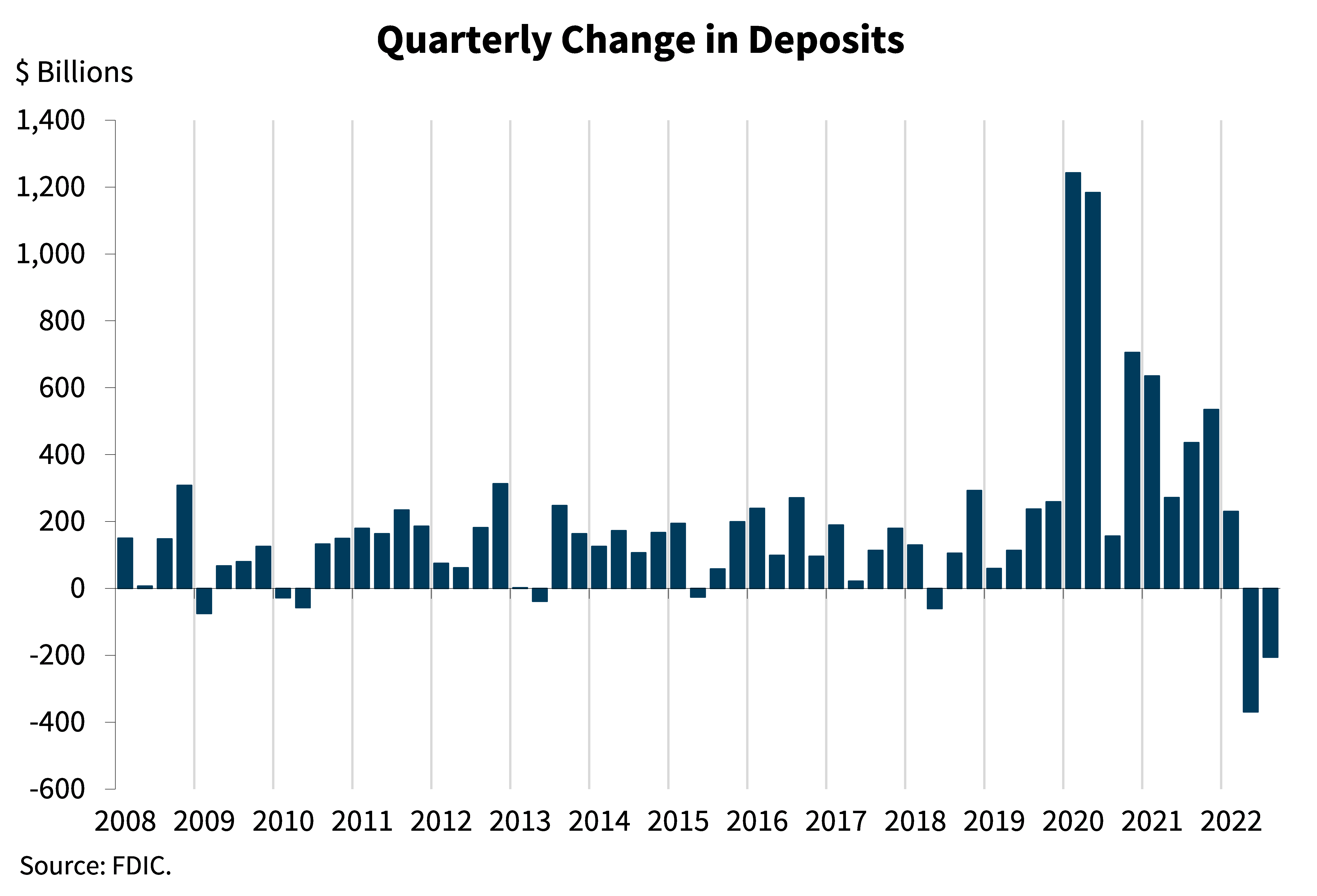

Let's consider a scenario where interest rates rise and there are fewer deposits in the market. In such a situation, the demand for loans decreases, and banks may find it difficult to lend the funds they have on hand. As a result, banks may choose to invest in bonds as an alternative way to earn income.

Bob Bank and Amarii Bank both purchase a bond with a face value of $1,000, a coupon rate of 5%, and a maturity period of five years. At the time of purchase, the bond is trading at par value, meaning it is priced at $1,000.

Now, let's assume that over the next two years, interest rates rise fast, and there is a decrease in deposits. As a result, the bond's market value falls to $900.

Bob Bank decides to designate the bond as "held-to-maturity" (HTM), which means that it will remain on Bob Bank's balance sheet at its original cost of $1,000, regardless of any changes in the bond's market value over the five-year period. This means that if the bond's market value falls to $900, Bob Bank will not have to report any loss on its balance sheet.

On the other hand, Amarii Bank decides to designate the same bond as "available-for-sale" (AFS), which means that any changes in the bond's market value will be reflected on Amarii Bank's balance sheet. If the bond's market value falls to $900, Amarii Bank will have to report a loss of $100 on its balance sheet.

In this scenario, Bob Bank has the advantage of not having to report any loss on its balance sheet, even though the market value of the bond has decreased. However, Bob Bank will not be able to take advantage of any increase in the bond's market value in the future, as the bond will remain on its balance sheet at its original cost.

On the other hand, Amarii Bank will have to report a loss on its balance sheet if the bond's market value falls below its original cost. However, if the bond's market value increases in the future, Amarii Bank will be able to take advantage of the increase and report a gain on its balance sheet.

AFS Securities: Banks' New Favorite Rollercoaster Ride"

It's interesting to note that there has been a significant increase in the amount of available-for-sale (AFS) securities held by US banks, according to data from the Federal Reserve. According to, the total amount of AFS securities held by banks increased by $1.31 trillion (46.89%) between Q3 2019 and Q4 2021, which is a much larger increase than the $131 billion mentioned in the original question. The total amount of AFS securities held by these banks reached $3.5 trillion in Q4 2020.[1]

A report by the Bank for International Settlements (BIS) also confirms that the share of AFS securities in the portfolios of major banks in advanced economies rose significantly in the first half of 2020.[1] This report highlighted that banks that relied more on non-traditional activities, including investment banking and trading, and had more exposure to corporate bonds and mortgage-backed securities, tended to hold a higher share of AFS securities.

However, the report also emphasized the increased risks associated with holding AFS securities during the pandemic, including higher volatility, increased uncertainty, and potential liquidity risks. In fact, the BIS found that banks with a higher share of AFS securities experienced greater market value losses during the pandemic-induced market downturn in March 2020.

These findings suggest that the pandemic-induced monetary policy response did have an impact on the situation with banks holding large amounts of AFS securities, as lower interest rates and asset purchase programs increased demand for higher-yielding securities. However, this shift in strategy also came with added risks, particularly during a period of increased market volatility and uncertainty.

The Stress Test Paradox: Why Some Banks Get a Pass

The Dodd-Frank Act, passed in 2010, mandated stress testing requirements for certain banks and financial institutions in the aftermath of the 2008 financial crisis. The Federal Reserve is responsible for enforcing stress testing requirements based on the size and complexity of the financial institution. The Dodd-Frank Act categorizes institutions into four groups, with each group subjected to different stress testing requirements.

Category I institutions include bank holding companies with $250 billion or more in total consolidated assets or nonbank financial companies designated as systemically important by the Financial Stability Oversight Council.

Category II includes bank holding companies with total consolidated assets between $100 billion and $250 billion

Category III includes those with assets of between $50 billion and $100 billion.

Category IV includes bank holding companies with total consolidated assets of less than $50 billion.

The stress test frequency and reporting requirements vary depending on the category of institution. Category I and Category II institutions undergo stress tests annually and are required to publicly disclose the results. Category III and Category IV institutions also undergo stress tests but are not required to publicly disclose the results. The Federal Reserve conducts supervisory stress tests on all Category I, II, and III institutions annually. However, Category IV institutions are not subject to supervisory stress tests. Nonetheless, they are still subject to regulatory scrutiny and may be required to provide their stress test results to regulators upon request.

A Risky Game of Regulatory Arbitrage

The emergence of the shadow banking system as a significant source of systemic risk in the global financial system is a cause for concern. One of the main drivers behind the growth of shadow banking has been the use of AFS assets by traditional banks, which allows them to avoid regulatory capital charges that come with holding these assets. This creates an arbitrage opportunity for shadow banks, enabling them to earn higher returns by taking on more risk without holding as much capital as traditional banks.

Historical events have shown that shadow banking can be highly leveraged and engage in maturity transformation, which creates liquidity risks. The interconnectedness between traditional banks and shadow banks can also transmit risks between the two sectors, leading to a contagion effect during a financial crisis. The 2008 financial crisis, for example, highlighted the dangers of this interconnectedness and the potential for shadow banking to contribute to a systemic crisis.

Banks that rely more on non-traditional activities, such as investment banking and trading, tend to hold a higher share of AFS securities. As a result, they are more likely to create regulatory arbitrage opportunities for shadow banks, indirectly contributing to the growth of the shadow banking system. This poses significant risks to the stability of the financial system, and regulators need to address the issue of regulatory arbitrage in order to mitigate the risks posed by the shadow banking system.

Personal Notes

To ensure that we are consistently providing our readers with valuable insights, I suggest that we publish Micro Thoughts every Tuesday, twice a month. This will give us the opportunity to focus on specific issues affecting the United States and provide regular updates on those topics. Continuing the publication of Macro Thoughts every Thursday is vital to provide our readers with a comprehensive understanding of the world. These articles will concentrate on global events and analyze their possible impact on the United States. Overall, I believe that by incorporating both micro and macro thoughts and publishing on a regular schedule, we can greatly improve the quality and relevance of Marathon Macro.

The information contained in Amarii Holdings' website and newsletters is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. This information is not intended to constitute individual investment advice or to be tailored to your personal financial situation. The views and opinions expressed in these publications are those of the publisher and editors and are subject to change without notice. The information may become outdated and there is no obligation to update it. Any use of this information is at your own risk and Amarii Holdings accepts no liability for any loss or damage resulting from your reliance on it. You should consult with your financial advisers before making any investment decisions to determine if a particular investment is suitable for your needs.