The years that Paul Volcker served as the Federal Reserve's chairman, from 1979 to 1987, are fascinating to me. For his efforts to reduce rising inflation in the United States in the late 1970s and early 1980s, Volcker is well known.

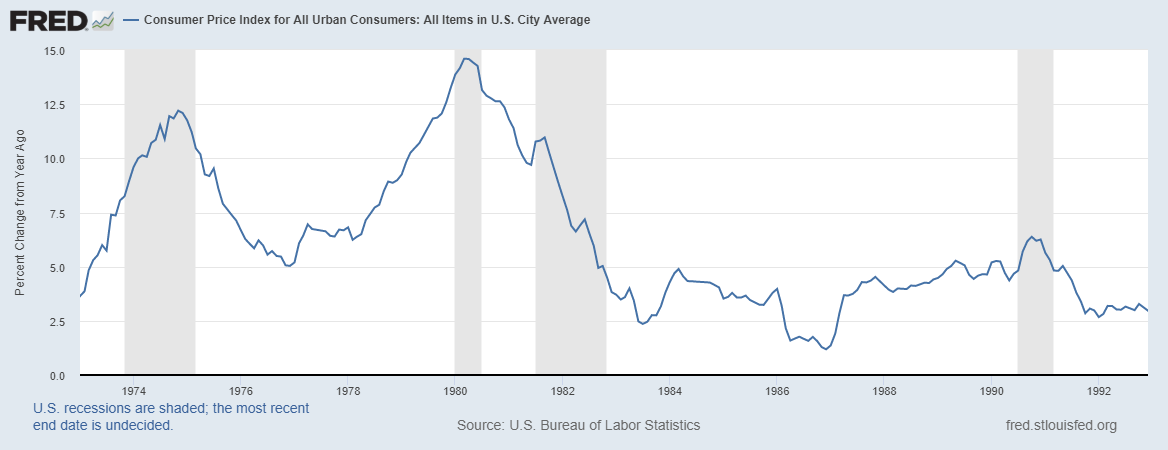

From the late 1960s, inflation has been a recurring issue in the American economy, reaching double-digit levels by the middle of the 1970s. It was commonly assumed that the Federal Reserve had lost control of the situation after previous attempts to fight inflation had failed.

In 1979, when Volcker became the new chairman of the Fed, he made bringing inflation under control his primary goal. He followed a stringent monetary strategy, increasing interest rates and limiting the amount of money in circulation. While doing so caused a severe recession, it also managed to lower inflation.

I also recognize the unexpected repercussions of Volcker's decisions. Since the recession was longer and more severe than expected, many people and businesses experienced substantial unemployment and financial hardship. Also, the Fed's high interest rates caused the dollar to appreciate significantly, which reduced the competitiveness of US exports and fueled the expansion of trade imbalances.

The United States' economy was still recuperating from the recession caused by Volcker's tight monetary policy in the early 1980s in the mid-1980s. While inflation was under control, the economy continued to struggle, with high unemployment and weak growth.

In order to address these concerns, Volcker began to relax monetary policy. He gradually reduced interest rates, making borrowing more affordable and accessible to consumers and businesses alike. This, in turn, resulted in higher spending and investment, which aided economic growth.

Volcker's more lenient approach to monetary policy was also influenced by global economic factors. In the mid-1980s, many other countries, including Japan and Germany, were experiencing strong economic growth. This put pressure on the U.S. to adopt more expansionary policies in order to remain competitive.

High inflation and unemployment rates were plaguing the economy, and the Federal Reserve was under pressure to take action. Paul Volcker, the Fed Chairman at the time, knew that he had to implement a tight monetary policy to combat inflation[1].

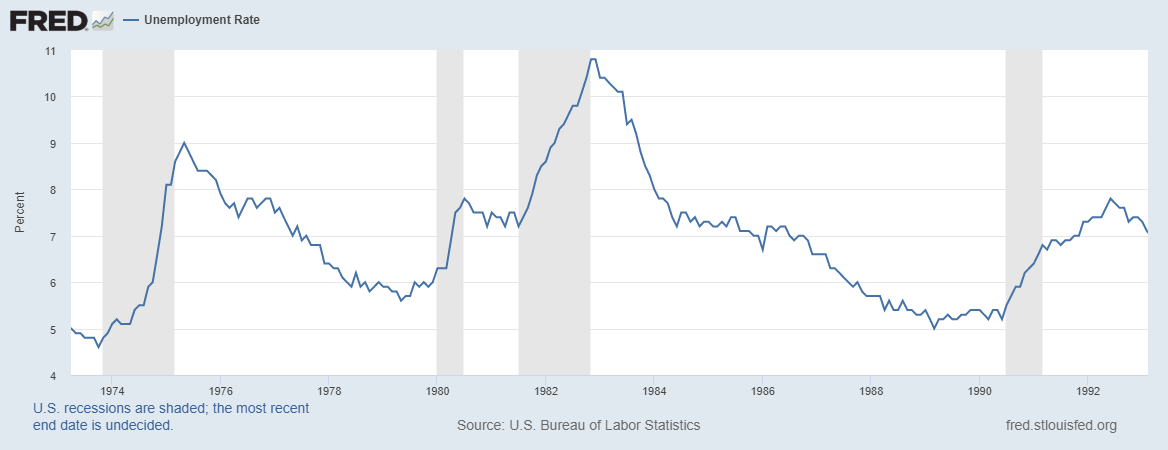

This policy, however, led to a recession in 1981-82, which put pressure on sectors of the economy reliant on borrowing, such as manufacturing and construction. Unemployment grew from 7.4% at the start of the recession to nearly 10% a year later. Despite repeated calls from Congress to loosen monetary policy, Volcker maintained that failing to bring down long-run inflation expectations would result in more serious economic circumstances over a much longer period of time.[1].

But Volcker persisted and his hard work paid off. His more accommodative monetary policy had some success in encouraging economic development. Unemployment dropped from 10.8% in late 1982 to 5.3% in early 1989. The success on the inflation front was accompanied by a gradual decline in the unemployment rate.[1].

Thanks to Volcker's actions, the brutal stagflation that tormented the nation in the latter stages of the Great Inflation of 1965 to 1982 came to an end. However, his policy did cause a revival of inflation. By the time Volcker stepped down as Fed Chairman in 1987, inflation had risen again[1].

When I think back on Paul Volcker's term as Federal Reserve Chairman in the early 1980s, I can't help but notice the mixed outcomes of his tight monetary policy. On the one hand, his initiatives helped to combat stagflation and stabilize the economy. Yet, by the time he left his job in 1987, inflation had risen again.

This serves as a reminder that while difficult decisions and short-term sacrifices may be required for long-term economic stability, they are not infallible solutions. To avoid repeating past mistakes, policies must be constantly reassessed and adjusted. The resurgence of inflation following Volcker's tenure emphasizes the importance of maintaining vigilance and flexibility in monetary policy.

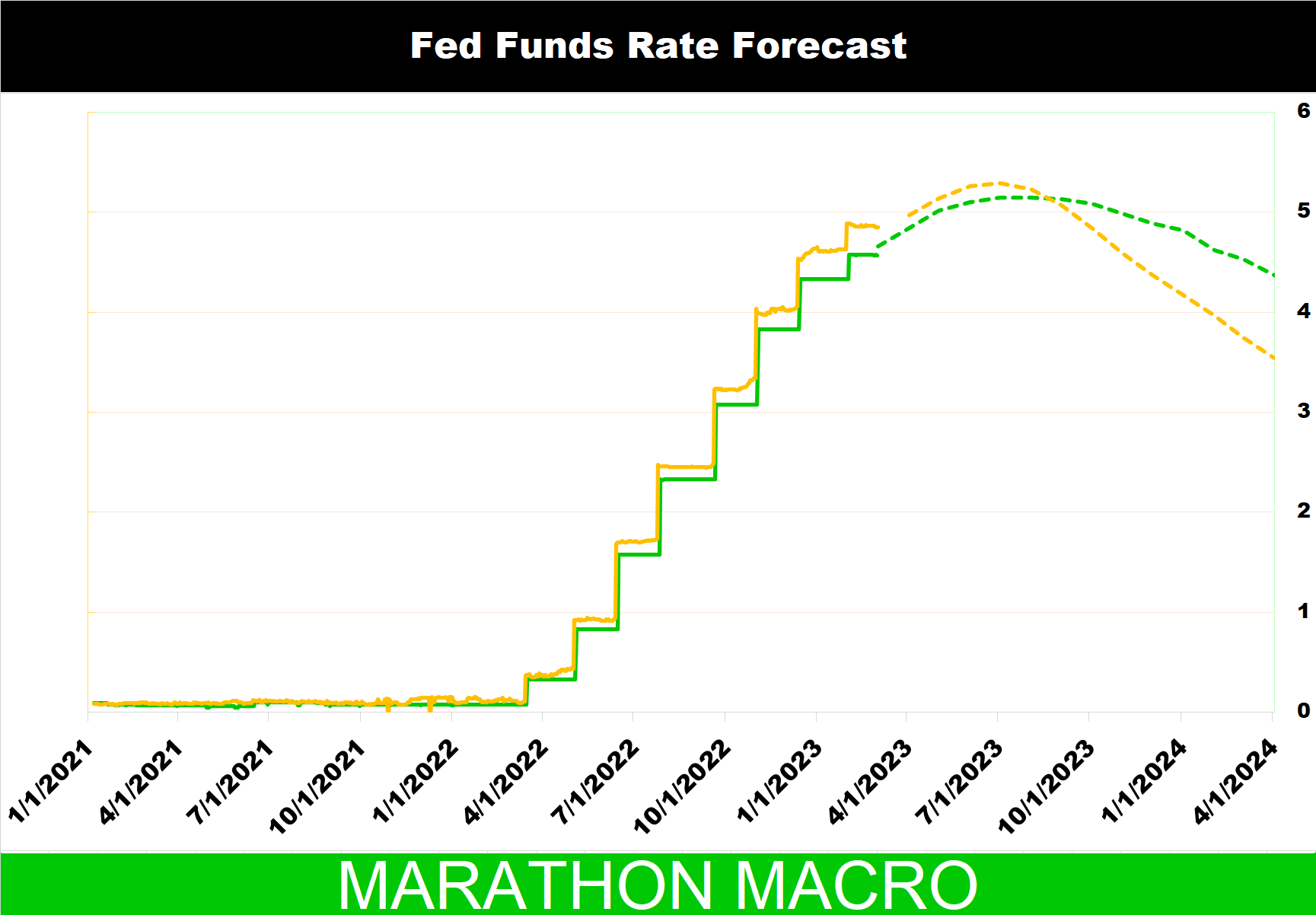

The Federal Reserve raised its benchmark interest rate by 25 basis points in February 2023. This was in line with expectations, as some analysts had predicted a 50 basis point hike[1]

In February 2023, the Federal Reserve chose to increase its key interest rate by 25 basis points in response to rising inflation. While this decision was a cautious one, I personally believed that a more aggressive approach was necessary and that a 50 basis point increase would have been more appropriate.

Choosing to only raise interest rates by 25 basis points can be compared to Paul Volcker's more lenient approach to monetary policy in the mid-1980s. Volcker gradually lowered interest rates and loosened monetary policy in an attempt to stimulate economic growth. This approach ultimately led to inflation coming roaring back in the late 1980s.

With the current level of excessive inflation, the Federal Reserve must take the necessary steps to bring it under control. This will most likely entail more rate hikes and an increase in unemployment, which may cause short-term economic damage.

History has shown that being too lenient on inflation can have disastrous effects, as was the case during the Paul Volcker era. Tightening monetary policy may cause a short-term recession and increase unemployment, but it is critical for long-term economic stability.

Inflation could escalate out of control if the Federal Reserve does not take necessary action. As a result, it is critical to confront inflation head on, even if it means making temporary compromises.

Although it is difficult to tolerate short-term suffering for long-term benefit, we must remember that the alternative is far worse. We must learn from history in order to avoid making the same mistakes again.

Further rate hikes and an increase in unemployment are needed to get inflation under control, even if it means short-term pain. Failing to take sufficient action now could have disastrous ramifications in the future, as we saw during the Paul Volcker era.

As the Federal Reserve prepares for further rate hikes to tackle inflation, it is important to be transparent and clear in their messaging about the potential for higher unemployment rates in the near future. I believe that by doing so, the public can be prepared and the shock and uncertainty that may arise can be minimized.

To manage expectations and prevent excessive panic or anxiety, the Federal Reserve should communicate clearly and directly with the public about the potential impact of rate hikes on employment. It is crucial to highlight that short-term pain may be necessary for long-term economic stability.

Furthermore, the Federal Reserve must work with other government agencies and organizations to design and implement initiatives that will support and assist those who may be affected by greater unemployment.

While the Federal Reserve takes steps to guarantee long-term economic stability, it is critical to communicate openly and provide assistance to people who may face an increase in unemployment. The detrimental impact of rising unemployment on individuals and the economy as a whole can be mitigated via clear communication and joint efforts.

I am filled with hope and excitement for this upcoming spring season. After enduring the haze of COVID-19 for the past two years, this spring is shaping up to be the best one in three years. I plan to do more traveling and exploring, both within Taiwan and possibly even abroad. It's important to remember that the Marathon doesn't stop, and neither should we in our pursuit of success and fulfillment.

The information contained in Amarii Holdings website and newsletters is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. This information is not intended to constitute individual investment advice or to be tailored to your personal financial situation. The views and opinions expressed in these publications are those of the publisher and editors and are subject to change without notice. The information may become outdated and there is no obligation to update it. Any use of this information is at your own risk and Amarii Holdings accepts no liability for any loss or damage resulting from your reliance on it. You should consult with your financial advisers before making any investment decisions to determine if a particular investment is suitable for your needs.

Subscribe to Marathon Macro

<100 subscribers

Unlock the secrets to becoming a better investor in just 10 minutes a week for Free!