Automated Market Makers (AMMs) were clearly revolutionary. AMMs made market making, which was previously only available to a select few, available to anyone who deposited a pair of tokens into a liquidity pool via a smart contract. The people who did this were called Liquidity Providers (LPs), and in return, LPs received a portion of the trading fees.

At first glance, LPs seem to be very profitable, but according to Bancor's report on Uniswap v3 LPs, 49.5% of all LPs reportedly lose money. The reason for this result is called Impermanent Loss (IL).

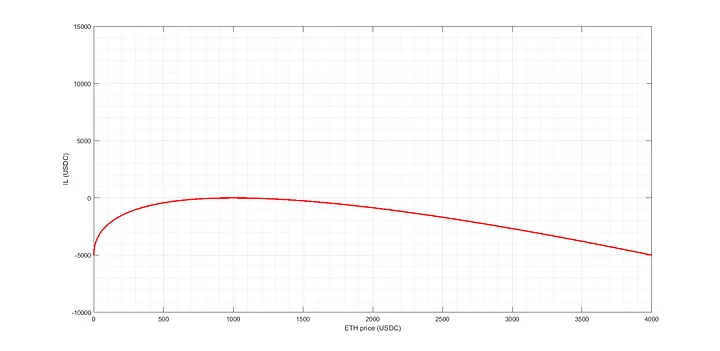

IL is caused by a change in the price of the token(s) when an LP deposits a token pair, and the value of IL is measured by how much they lost by depositing the token pair into the liquidity pool compared to just holding the same amount of tokens. For example, using the IL calculator, we can see that a 100% increase in the price of Token A, which was previously 100 times the price of Token B, would result in a 5.72% loss for an LP who deposited into the liquidity pool compared to if they had not. (This does not include any trading fees earned by the LP).

Why does IL happen? As the demand for token A rises, more people will deposit token B into the liquidity pool and take token A out of it. This causes two things to happen:

1. The number of tokens A in the liquidity pool decreases, and the number of B increases.

Since tokens A have become scarcer in the pool relative to B, the price of A, relative to B, has increased.

So, naturally, the number of tokens whose price has increased relative to what it would have been if you just held on to them will decrease, and the number of tokens whose price has not increased will increase, and you will lose money.

Referring back to the original report, "49.5% of Uniswap v3 LPs lose money" means that the losses from IL are greater than the trading fees earned from liquidity deposits. Considering that Uniswap v3 is an AMM that maximizes capital efficiency through concentrated liquidity, we would expect other Uniswap v2-style LPs to be more unprofitable.

As such, it is generally unprofitable to LP due to IL, and DEXs recognize this and try to fill the gap with their own token incentives. In addition, projects like Arrakis Finance automatically manage LP positions, helping regular users get better returns.

Here are some projects that do this:

Flashbot → MEV Industry

Hidden Hand → bribing of veTokens

Flashbot opened up MEV earnings to everyone, which was previously only accessible to a few with a high level of technical understanding, while projects like Hidden Hand and bribe.crv provided a marketplace for bribes in veTokens, allowing for more accurate pricing for each bribe.

While we all have different opinions on whether bribing for MEV or tokens is a good or bad thing, we can all agree that it can't be completely prevented, so if it can't be eliminated, it's in everyone's best interest to bring it to the surface and make it transparent and accessible.

In the case of MEV, some teams believe that it can be completely prevented, so it may not be the best example, but Flashbot's approach fits the "if you can't get rid of it, bring it up" mold.

Projects that fall into this category include:

Alkimiya → commoditizes the future cash flows generated by a specific hashrate and consequently makes blockspace tradable.

Timeless Finance → allows you to trade only the interest of a yield bearing asset (ex: yvUSDC, stETH).

I'm sure there are many more, but "trade the untradable" is probably the most successful strategy for DeFi protocols to find PMFs. By taking something that was previously untradable and somehow structuring it to make it tradable, you can 1) create a new way to hedge against certain events, and 2) deepen the underlying market. Of course, being a playground for speculators is a bonus.

Smilee Finance tries to apply the two strategies mentioned above to IL:

Like MEV and bribing, IL cannot be completely eliminated due to the structure of AMM, and it is probably a necessary evil that LPs have to bear.

Also, IL is not tradable until now. People could lose money on ILs, but they couldn't profit from them unless they were actively arbitraging on a DEX.

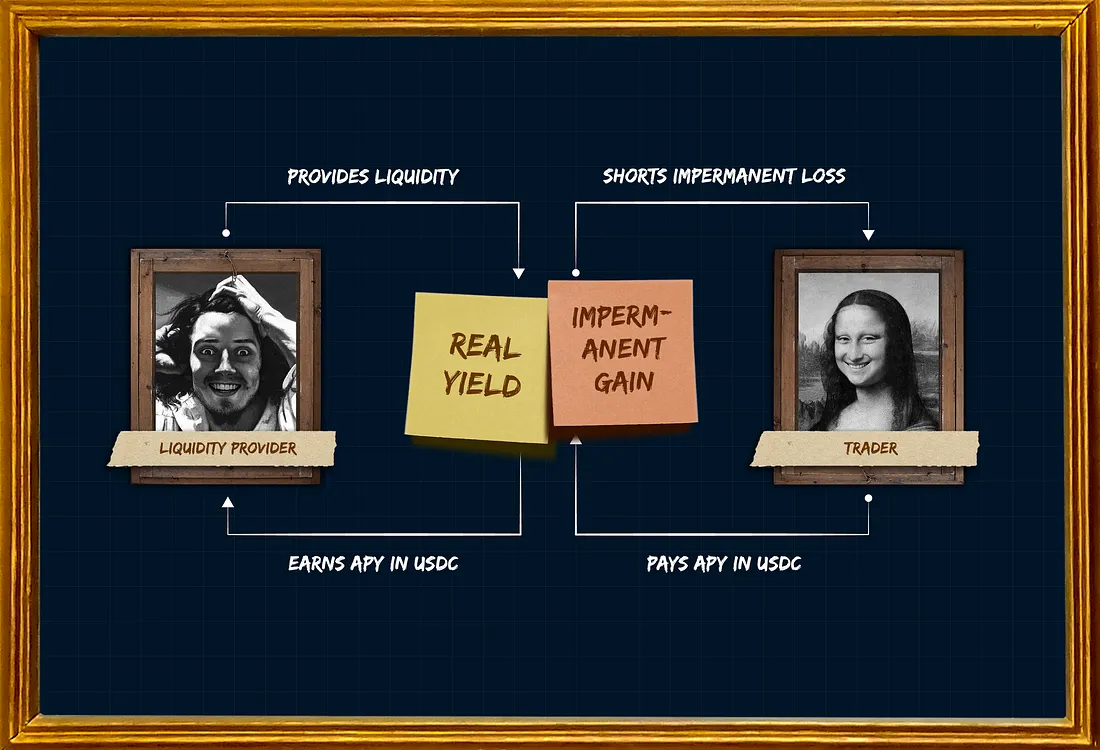

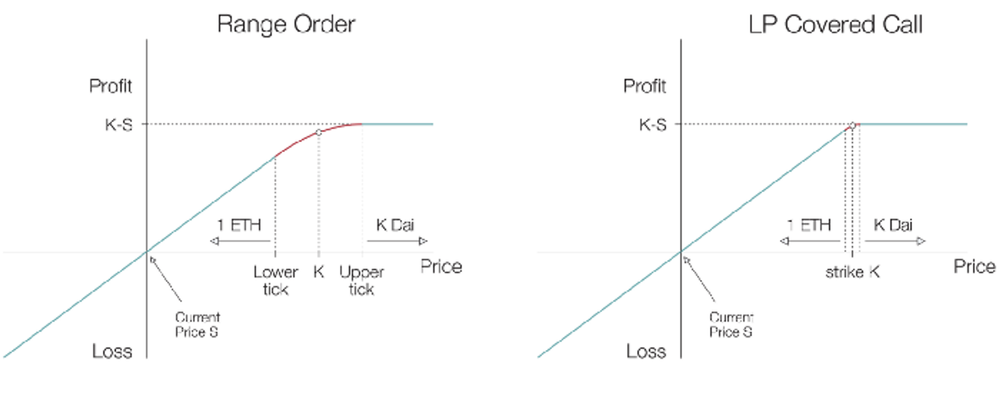

ILs are structured so that the more an asset deviates from its original price, the more volatile it is, the more you lose. In other words, LPs are short volatility (gamma).

Smilee Finance has created a Decentralized Volatility Product (DVP) that replicates the returns of IL and allows users to go long on this DVP and pay a premium to get an impermanent gain, or go short and get an option premium in exchange for exposure to IL.

As mentioned in the 2023 outlook, I believe that DeFi as a playground for djinns and speculators will remain in steady demand. In this case, Smilee Finance and Y2K Finance can be seen as safe playgrounds for degens to run around in, and I say "safe" because there are clear winners and losers. Some DeFi protocols present themselves as if it's a positive-sum game, and if you play hard enough, everyone wins, and I would define these protocols as "unsafe" playgrounds.

If you can't get rid of the playground, you might as well make it safe, and a DeFi protocol that says, "This game is zero-sum, so there are clearly people who win and people who lose, and the choice is up to you" is the ideal playground for degens.

However, this doesn't mean that Smilee Finance and Y2K Finance don't benefit the market itself. In the case of Y2K Finance, users can hedge against the risk of stablecoin de-pegging, minimizing their losses in the event of a UST-like event. In the case of Smilee Finance, it can help the market in the following ways:

When events like the Shanghai Update or the FOMC happen, token holders can hedge against volatility by shorting DVP. This can stabilize the token price.

LPs can short DVP to hedge against ILs in highly volatile liquidity pools. This can create deep liquidity in a volatile pool.

Both protocols can contribute to market stability by giving users the opportunity to hedge.

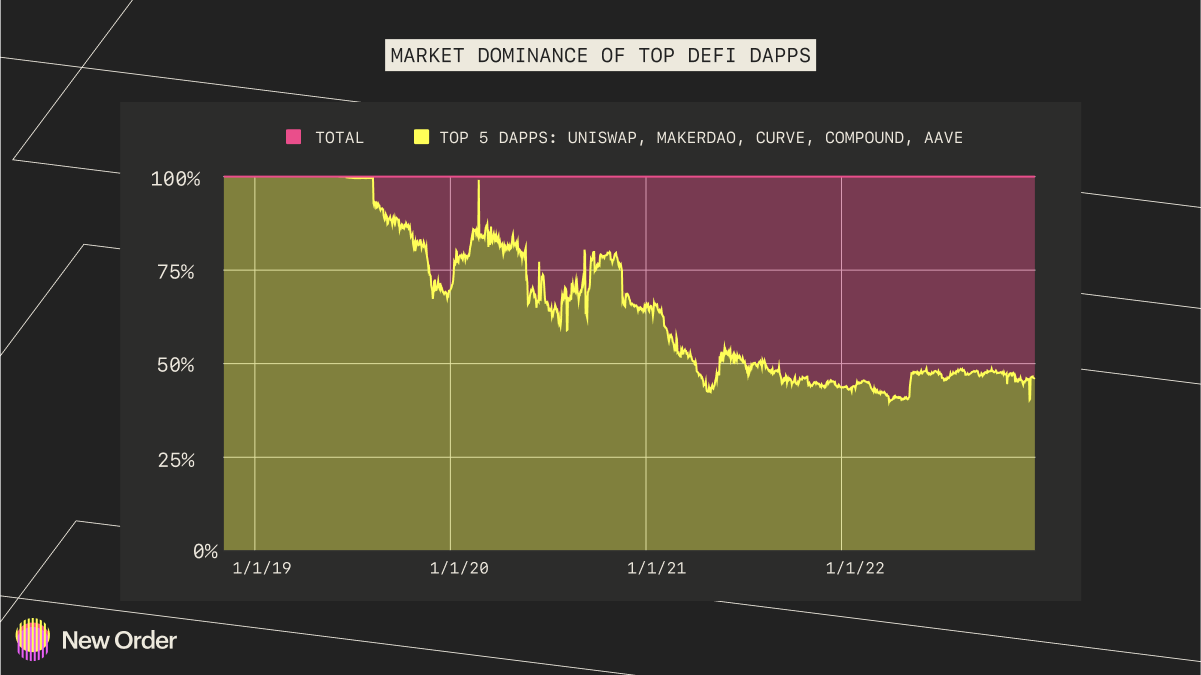

Looking at the current DeFi industry, we can see that the top five DeFi protocols account for 85% of the total TVL. In this situation, the best strategy for a new DeFi protocol is to jump on the tiger's back.

In the case of Y2K Finance, it was created by leveraging existing stablecoins and Liquid Staking Derivatives (LSDs), and in the case of Smilee Finance, it leverages existing legacy by converting existing liquidity pools on Uniswap or Curve into DVPs. Rather than going head-to-head, these strategies are smart moves that capitalize on one of DeFi's greatest strengths: composability.

Y2K Finance and Smilee Finance also have the potential to be used for P2P (Protocol-to-Protocol) business.

Protocols that are launching new stablecoins can use Y2K Finance to provide insurance for users to use their stablecoins with more confidence in the event of a pegged event. If a DAO or protocol is acting as an LP for its own native token, it can use Smilee Finance as a means of hedging against IL. These two protocols are also attractive to general retailers, but they get extra points for being able to have other protocols as customers.

One possible DVP short position, the Real Yield Vault, can provide LPs with a higher, more predictable return. Each Real Yield Vault specifies a token pair, a target APY, an expiration date, and an auction period, during which LPs deposit a token pair or a single token as liquidity for the desired vault. Then, when the maturity date is reached, the LPs are rewarded with a profit equal to the premium paid by the opposite Impermanent Gain Vault depositors minus the IL.

For a token pair x/y, letting the price appreciation of x relative to y be r, the initial deposit be V0, and the premium paid by the Impermanent Gain Vault depositors be P, the Real Yield depositor's PnL is as follows: (See Appendix for derivation)

While LPs traditionally receive a swap fee as a reward for depositing into a liquidity pool, in the Real Yield Vault they receive a fixed premium P in USDC, which is much more predictable and stable.

In fact, we can see that Real Yield Vault is more stable than Uniswap V3's ETH/USDC pool, assuming liquidity is deposited in the range (-50%, 50%). This is especially true when the value of r changes significantly.

( Real Yield Vault vs Uniswap v3(-50%, 50%) range | Smilee — The first primitive for Decentralized Volatility Products (DVPs))

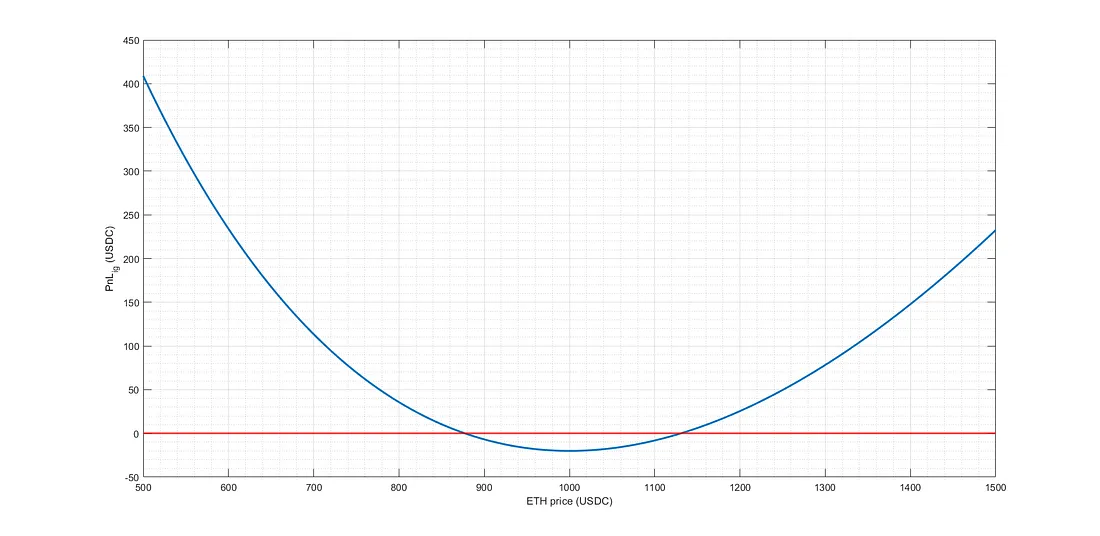

One of the possible DVP long positions is the Impermanent Gain Vault, which is suitable for those who want to bet on volatility and can profit from entering an Impermanent Gain Vault before an event such as the FOMC or a merge. Each Impermanent Gain Vault specifies the token pair, premium, leverage, expiration date, and auction period, during which users can pay the stated premium to enter the desired Impermanent Gain Vault. The premium is used as the APY for the opposite position, the Real Yield Vault. Then, when the expiration date is reached, the user will receive a profit minus the premium paid for Impermanent Gain.

For a token pair x/y, let's call the price appreciation of x relative to y r, the initial deposit V0, and the premium paid by depositors of the Impermanent Gain Vault P, the PnL for depositors of the Impermanent Gain Vault is as follows: (See Appendix for derivation)

Since the Impermanent Gain Vault works similarly to insurance, the profit increases with r, i.e., the more the price of one token changes relative to the price of another token.

In order for the Impermanent Gain Vault to pay off, the value of r must be greater than r1 or less than r2 below.

For example, if you deposit $10,000 of initial funds into the Impermanent Gain Vault at ETH/USDC with a premium of $20, the price of ETH must increase by at least 13% or decrease by at least 12% in order to see a profit according to the formula above. As you can see from the above example, Impermanent Gain is inherently highly leveraged, but at the same time, you can only lose up to the premium, making it a very capital-efficient and relatively safe product.

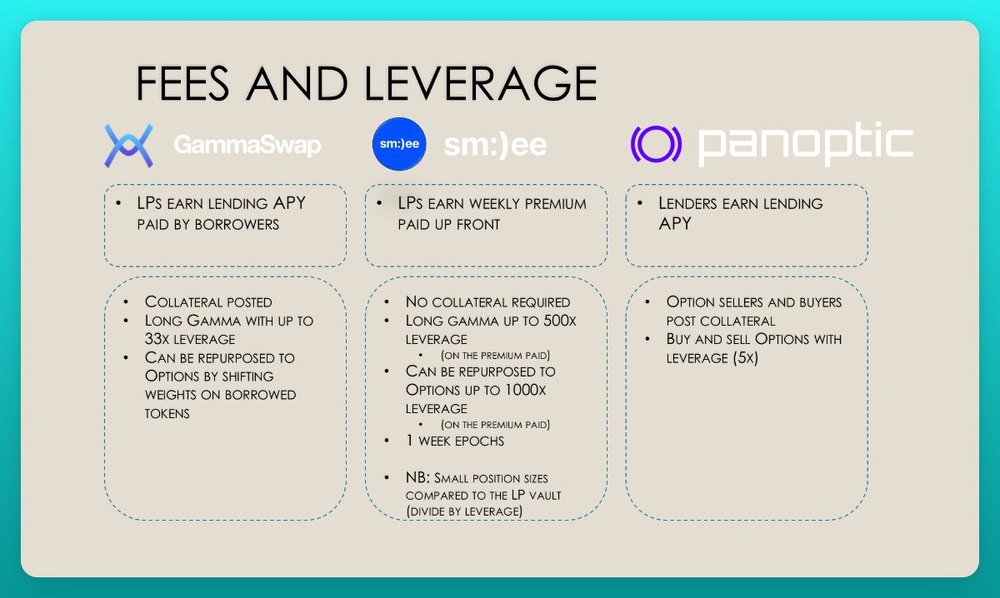

While we've only covered Smilee Finance in this article, protocols like GammaSwap and Panoptics also focus on making ILs tradable by turning them into volatility-based products. For a detailed comparison, please refer to this thread.

GammaSwap allows LPs to borrow the LP tokens themselves and short them for impermanent gains. LPs deposit their LP tokens and receive transaction fees and interest from borrowers. Since LP tokens are taken and spent as they are, there is no oracle, and positions have no expiration.

Panoptic is a protocol based on Uniswap V3 that offers Perpetual Options, which are options with no expiration date. The act of providing liquidity to Uniswap V3 is very similar to selling a put option.

Panoptic takes this idea and implements it through put-call parity, where buying a put option is borrowing liquidity, selling a put option is depositing liquidity, and for call options, put-call parity. It also imports Uniswap v3 LP tokens as is, so there is no oracle and no position expiration.

The first advantage of Smilee Finance is that it uses the form of a vault, which makes it easy for end users who don't understand LP tokens to use it because it abstracts away the actual workings. Also, in the case of Real Yield Vault, depositors can get a predictable return, which is also an advantage. However, the presence of expiration dates and the reliance on Uniswap and Chainlink's oracles can be seen as disadvantages.

Smilee Finance is a interesing protocol that allows you to bet long and short on volatility via IL. Just as Y2K Finance is expected to naturally increase its TVL and user base with the development of the stablecoin and LSD industries, Smilee Finance is expected to grow naturally as DEXs maintain or increase their current TVL. There are projects like GammaSwap and Panoptic that are similar to Smilee Finance, but I personally think that the Vault format will be the most accessible to users, so I'm looking forward to Smilee Finance to dominate this scene.