Disclaimer: This article is written for informational purposes only and does not take responsibility for investment, legal, or advisory aspects. It is not a recommendation for investment in any specific assets, and investment decisions should not be made solely based on this content.

1. Introduction

I believe that Berachain is undervalued. I'm not talking about its valuation in terms of its seed round valuation or as a target for airdrops. As its stated at the beginning, this article is not an investment recommendation. Fundamentally, I lack the intelligence and knowledge to make such recommendations. Therefore, if you are expecting such content, this article is not for you. The undervaluation I'm talking about is its value as a case study in this industry.

In my personal opinion, if you are a player in this industry and you should study Berachain's playbook. You need to study how it started in the NFT community, and sublimed its most personal problems to building a independent Layer 1. You should study how it created its own language within the community without any marketing expense. You need to study how it efficiently gathers funds for the most costly aspects of running a Layer 1, such as security and liquidity.

It's been over a year since I first introduced Berachain, so I decided to write this article to update the content of the original article and to encourage more people in the industry to take Berachain MORE seriously.

2. Understanding Berachain

The background and basic information about Berachain have been well explained in various articles such as follows:

Berachain - Innovating the Approach to L1 Building by Blocmates

Berachain Explained Interview with Smokey | Beramates 001

Therefore, I will only mention a few points that I personally want to emphasize.

2.1 Community First, Tech Delivered

It seems that everyone somewhat acknowledges that Berachain has a strong community. However, having a strong community alone is not enough; it must be accompanied by strong technical capabilities to create products. My confidence in Berachain's technical capabilities started with Polaris.

To discuss Polaris, we first need to look at the technical components of Berachain. Berachain combines hot topics from each fields. For its consensus engine, it uses CometBFT; as a blockchain framework, Cosmos SDK; for VM, EVM; and for oracle, Skip's Slinky module. Polaris is the framework that connects EVM with Cosmos SDK.

Polaris is an in-house framework developed by the Berachain team, allowing arbitrary base layers like Comos SDK, Polkadot Substrate, etc., to use Ethereum-equivalent EVM. The advantage of using Polaris is that it separates the base layer and the EVM runtime layer, allowing developers to experiment with the base layer without harming the EVM. For example, custom precompiles can be added for customization. In Berachain's case, they implemented the Proof of Liquidity mechanism through their own precompiled contracts.

Polaris is open-source, and as far as I know, it is used by various projects including Berachain, Argus's World Engine, Cosmos gaming L1 Tabichain, and modular liquidity project Mitosis. The use of the Polaris framework by various projects is not a direct benefit to Berachain, but I think it is enough to verify & certify the top-tier technical ability of the Berachain team.

2.2 Chain of the Degen, by the Degen, for the Degen

Perhaps more important than the fact that Berachain started with the NFT project Bong Bears is that its inital community was full of degens. They were heavy on-chain users, DeFi users, and traders, so I think Berachain has started from their most internal, private, or maybe personal desire or motivations.

In fact, most alt-Layer 1 projects came out to solve the problems of existing on-chain users, so Berachain does not seem to differ much in this regard. What I think Berachain differs from other is that their needs were their most personal needs. Some say that you should do business to meet the needs of others, but that argument assumes that I can understand the minds of others 100%. I think that assumption is false, so I believe that the highest probability of success in business is when you try to meet your own needs. Also, when trying to solve one's own needs, outlier results can occur, as seen in cases where patients with rare diseases or their families create their own treatments. As far as I know, besides Canto, there is no alt-Layer 1 with founders and building teams as degens as Berachain.

2.3 Proof of Liquidity (PoL) vs World

Proof of Liquidity is undoubtedly Berachain's flagship concept. To better understand Proof of Liquidity, let's compare it with Liquid Staking, Superfluid Staking, and Restaking.

2.3.1 What is Proof of Liquidity?

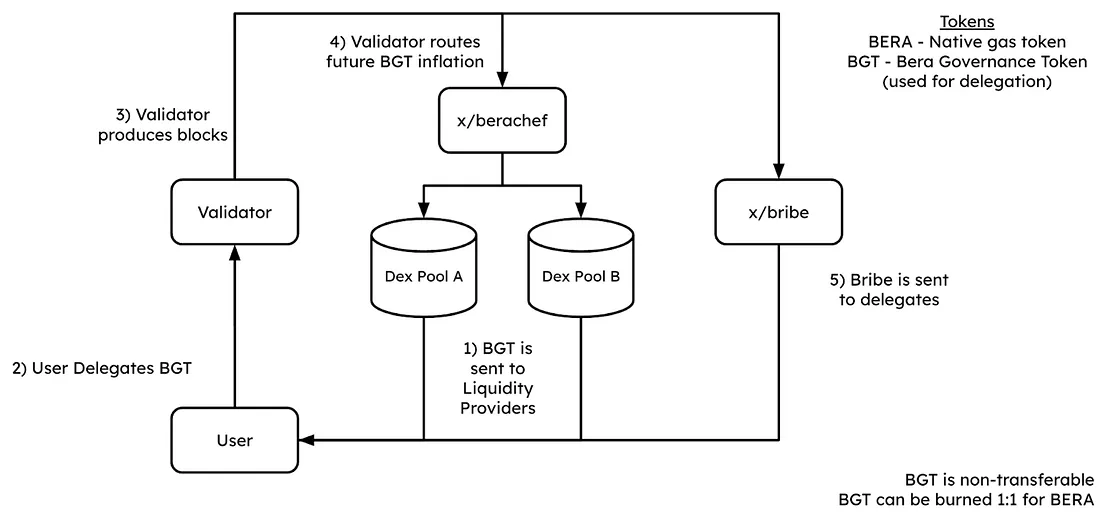

Proof of Liquidity is a consensus algorithm created by Berachain to compensate for the problems of existing Proof of Stake: 1) opportunity cost of staking, 2) staking centralization, and 3) misalignment of incentives between ecosystem protocols and validators.

Opportunity cost of staking: Users have to choose between enhancing the security of the chain and deploying liquidity.

Staking centralization: When the native token of the chain is newly minted due to inflation, it goes pro-rata to existing staking participants, leading to increasing centralization of staking.

Misalignment of incentives: Validators do not benefit from the activation of the ecosystem, and ecosystem protocols cannot contribute to enhancing the security of the chain.

To solve this, Berachain devised a mechanism where contributing to liquidity is the only way to contribute to the security of the chain. Berachain maintains security through staking of $BGT, a non-tradable governance token. This $BGT cannot be purchased in the market and can only be obtained by performing specific activities in services specified by Berachain. This includes depositing liquidity in specific pools of Berachain's native DEX BEX, borrowing $HONEY from Berachain's native lending service Bend, and providing liquidity in Berachain's native futures service Berps.

2.3.2 vs Liquid Staking

At first glance, the rewards from PoL may seem similar to depositing ETH in a Liquid Staking protocol and then LPing the LST, but there are several differences upon closer inspection.

Order of procedure: In the case of Liquid Staking followed by LPing, the process is $ETH deposit → receipt of shadow tokens like $stETH → LPing in stETH/ETH. However, in Berachain's case, it's liquidity deposit in $WBERA/$HONEY → receipt of $BGT → staking through delegation, which is the opposite.

Issue of staking centralization: Unlike Liquid Staking, Berachain's PoL is fundamentally free from the issue of staking centralization. Of course, protocols like Lido and Rocketpool are making efforts to prevent staking centralization and use mechanisms like DVT, but PoL fundamentally does not need to worry about this.

Governance overhead: Liquid Staking protocols inherently have governance overheads, such as node operator selection and conflicts of interest between $ETH holders and $LDO holders. However, PoL in Berachain is enshrined in the chain, so it is free from these problems.

Type of rewards: We will look at this in more detail later, but the type of rewards users can get from participating in each protocol is different.

2.3.3 vs Superfluid Staking

In the case of Osmosis's Superfluid Staking, users can stake or delegate OSMO/X LP tokens, which is similar to PoL in that it catches two birds with one stone: liquidity and chain security. However, there are differences as follows:

Presence of a discount factor: In Superfluid Staking of Osmosis, if it's an LP token, its value is discounted compared to regular $OSMO staking. On the other hand, in Berachain, because everyone must deposit liquidity to stake governance tokens, so there is no concept of a discount factor.

Choice of LP pools: In the case of Superfluid Staking of Osmosis, only pairs including $OSMO are possible, but in Berachain, any liquidity pool can receive $BGT emission as long as it is approved by governance. Initially, Berachain plans to have House Pools, where only default liquidity pools can receive $BGT, but new liquidity pools can receive $BGT emission as long as the it passes the governance.

Tradable status of governance tokens: In Berachain, to enforce liquidity provision for governance power, $BERA and $BGT are deliberately separated, and $BGT is made non-tradable. In the case of Superfluid Staking of Osmosis, there is no such purpose.

2.3.4 vs Restaking

Restaking aims to gather fragmented security in one place by using funds staked in the original chain to verify and stake in other infrastructures(AVS). In this regard, Berachain's PoL is closer to Liquid Staking than Restaking, as its purpose is more about increasing liquidity than security. Of course, if we think Berachain's BEX, Bend, Berps as infrastructure, there are commonalities in philosophical concept.

2.4 Possibility as a Settlement Layer

A settlement layer is a layer that verifies the validity of transactions and solving the dispute. Depending on the design, both the DA layer and the execution layer can act as a settlement layer. In the case of Ethereum Layer 2, Ethereum mainnet resolves final disputes over transactions, so Ethereum can be considered a settlement layer, and in the case of Sovereign rollup, which verifies the validity of transactions in the execution layer, the execution layer can be considered a settlement layer.

As shown in the 'Scaling Bera' session in recent Berapalooza event, Shogun, Movement Labs, and Argus Labs seems to have plan to launch their projects based on Berachain. Shogun seems to be a team implementing an off-chain solver network for processing intents on-chain, Movement is a MoveVM-based rollup project, and Argus is an on-chain game studio/infrastructure project.

In my personal opinion, the biggest advantage of projects newly launching using Berachain as a Settlement Layer is not the technical advantage, but the ability to leverage the already existing strong community. For example, if Movement launches a MoveVM-Bera rollup using Berachain as a Settlement Layer, many Berachain community users will try it. This is similar to the logic of teams considering pivoting to Layer 2 to leverage the Ethereum community or projects using Celestia as a DA layer to leverage Celestia. Of course, the liquidity gathered through PoL in Berachain is a bonus.

3. PoL Advanced Course | Looking at Each Stakeholder

To better understand PoL, we need to look at each stakeholders in PoL; users, validators, and protocols participating in this ecosystem. For reference, here, users are equivalent to stakers who do not directly operate validators but delegate governance tokens $BGT to validators. In Berachain, governance is basically maintained in the form of Cosmos SDK, so participation is possible in a similar way to DPoS with a fixed number of validators.

3.1 Users

3.1.1 Goal

The goal of users is to maximize rewards by contributing to the security and liquidity of Berachain.

3.1.2 Actions to Take

To achieve this, the following actions should be taken:

Choose a liquidity pool in Berachain's native DEX, BEX and deposit liquidity: Not all liquidity pools give $BGT as a reward, so this should be considered when choosing.

Delegate the $BGT obtained through liquidity deposit to validators

Exercise voting rights in governance proposals: This does not affect rewards. However, as a user of Berachain, passing proper proposals and blocking malicious ones will indirectly affect your economic rewards.

3.1.3 Rewards

The rewards users get through these actions are as follows:

LP fees: The usual trading fees obtained by depositing liquidity in LP

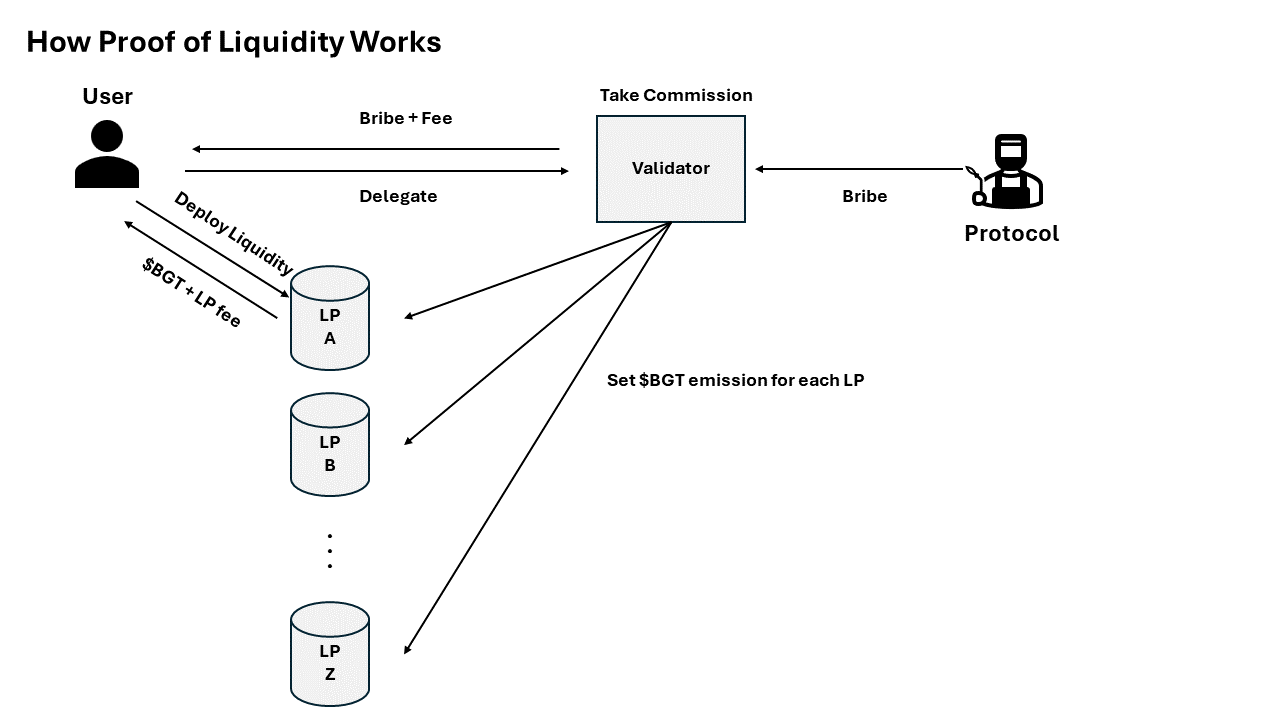

Bribe from validators: Validators can provide additional economic incentives to attract users. In the case of Berachain, this mechanism is implemented enshrined to chain itself as 'bribe'.

(1-Commission) * Block Capture Value (BCV): One of Berachain's unique features, BCV refers to specific fees generated in Berachain's native dApps BEX, Bend, and Berps. For example, when swapping tokens in BEX, a certain transaction fee is allocated to BCV, and when minting or burning $HONEY with $USDC in Bend, a certain fee is also allocated to BCV. Validators who get the chance to create blocks can include transactions containing BCV in their blocks, thus earning the corresponding BCV as a reward. Here, validators take a certain commission, and the rest is provided to users who delegated to them.

(1-Commission) * Gas Fees: According to the original EIP-1559 model, the base fee is burned, and priority fees are provided to validators and users who delegated to them.

3.1.4 Decision Making

Users have to make two major decisions. The first is "which LP to deposit liquidity in," and the second is "which validator to delegate my $BGT to."

In the case of liquidity pools, you should choose the pool where the sum of $BGT + LP fees obtained by depositing is the highest. The problem is that $BGT cannot be directly converted into economic value, so the decision may vary depending on the user's preference. For now, $BGT is non-tradable, but it can be exchanged 1:1 for $BERA (the opposite is not possible), so $BGT = $BERA + a, but the value of 'a' will be different for each person. Also, the more $BGT a liquidity pool gives, the more people will flock to it, and accordingly, the LP fees each user takes will decrease, so optimizing this is an interesting part.

In the case of choosing validators, 1) choose validators that do not miss blocks and verify and create them well, 2) give the most bribes, and 3) take the least commission.

3.2 Validators

3.2.1 Goal

Validators are essentially users + node operators, so the goal is to get the most rewards through validator operation and staking.

3.2.2 Actions to Take

Block creation and verification: Not only should you participate diligently in block creation and verification, but you should also include as many transactions related to BCV as possible to get the maximum reward.

Propose and vote on governance proposals: Everything from which tokens to newly import into BEX to whitelisting new liquidity pools to the $BGT emission is determined by governance, so governance is VERY important.

Determine the proportion of future $BGT inflation corresponding to your $BGT stake: According to the PoL mechanism, when validator A creates a new block, $BGT is newly minted according to the inflation plan. This $BGT is then paid to the liquidity pools specified by validator A. For example, let's say validator A has about 4% of the total $BGT stake. Then, the validator has decision-making power over 4% of future $BGT emission. If the validator allocates 3% to the $WBREA/$USDC pool and 1% to the $WBREA/$HONEY pool, then 3% of the newly minted $BGT from future $BGT inflation will be allocated to liquidity providers in the $WBERA/$USDC pool, and 1% to those in the $WBERA/$HONEY pool. This is done by a precompile called 'Berachef', and I think this job is the most important thing that Berachain's validators do.

Contract off-chain with protocols within the Berachain ecosystem that need liquidity: As seen earlier, validators have the powerful ability to induce users to deposit liquidity in certain token pools through $BGT emission amount adjustment. For this reason, protocols within the Berachain ecosystem can bribe validators and ask them to adjust $BGT emission to their liquidity pools.

3.2.3 Rewards

Commission on BCV & Gas Fee: Validators earn commissions on BCV and Gas Fee as compensation for node operation.

Bribe from Berachain ecosystem protocols: Economic rewards can be obtained in exchange for providing $BGT emission to certain liquidity pools. Of course, to do this, the proposal to whitelist the pool must first pass governance. Validators can keep part of the bribe they receive and use the rest to bribe more stakers.

User(Staker) revenue: As mentioned earlier, validators are likely to deposit their funds as liquidity like other users, so they also earn as users.

3.2.4 Decision Making

The decisions validators have to make can be divided into relationships with protocols and users.

First, in the relationship with protocols, the goal of validators is to make contracts with protocols that provide the most bribes, and accordingly, determine the proportion of $BGT emission for their stake. If a validator has sufficient liquidity, they can negotiate to deploy their liquidity to the protocol's native token pool in addition to $BGT emission and receive more bribes.

To get more bribes from protocols or increase bargaining power, validators need to have more $BGT, which leads to the importance of relationship with users(stakers). Ultimately, the variables validators can adjust are commission and bribing users. They must carefully decide between the short-term revenue of raising commission and not bribing and the long-term economic value of bribing to secure more $BGT.

3.3 Protocols

3.3.1 Goal

The goal of protocols within the Berachain ecosystem is to maximize the liquidity of their native tokens so that users do not have major problems trading those tokens.

3.3.2 Actions to Take

Community activities: By promoting how their protocol and native token positively impact the Berachain ecosystem, they should induce validators and users to propose and pass proposals to whitelist their token pools.

Bribing validators: To induce more users to provide liquidity to their token pools, they should bribe validators to maximize $BGT emission to their pools.

3.3.3 Rewards

More liquidity for my native token pairs!

3.3.4 Decision Making

In the case of protocols, they have to decide who and how much they should bribe to induce $BGT Emission. To do this, they need to consider various variables, such as 1) the value of unit liquidity secured per $BGT emission, 2) the target amount of liquidity for their native token, 3) the upper limit of costs that can be spent on bribing due to $BGT emission, etc. They need to choose the best validators (or validators) for each situation and secure liquidity as close to the target as possible with the least amount of bribing.

4. Strategic Considerations

4.1 Users

In my opinion, there are two important things for users in Berachain. The first is to quickly find good liquidity pools and organically move liquidity according to changing situations, and the second is to participate in governance. The first is self-explanatory, so let's look a little more at the second.

To allocate $BGT emission to new token A, a proposal must be proposed unconditionally, and the proposal must pass governance. Due to the nature of the Cosmos governance module, users who have delegated tokens have the opportunity to vote first, and if they do not vote, validators can vote on their behalf.

In other words, users have the authority to override the votes of the validators they have delegated to. For this reason, even if validators and protocols agree off-chain to whitelist a certain token pool, users who have delegated to those validators can ultimately override it. Therefore, the more active the users' voting, the more validators will have to include users' rights in the contract, which I cautiously predict will lead to more sharing of bribes received from protocols with the delegators.

For example, when validator A agrees to whitelist protocol B's native token $B in exchange for a certain bribe, the stakers who have delegated to validator A can claim that they will override validator A's voting rights and withdraw delegation unless they receive 90% of the bribe from the contract. To do this, it is important for users to speak out and claim their rights as a group or union, not as individuals.

4.2 Validators

For validators, it is important to turn the validator flywheel. If more users delegate $BGT, validators will have stronger bargaining power with protocols, and if they can receive more bribes with that bargaining power, they can provide more rewards to users as bribes, which will attract more delegations from users.

There are several ways to start this flywheel, such as using 0% commission or negative commission (0% commission + own bribe) initially, or quickly contacting undervalued Berachain ecosystem projects to make off-chain contracts for cheap bribing. In addition, there may be creative initiatives in non-economic areas to deliver values to 1) users or 2) protocols that other validators cannot provide, which I expect will help find the starting point of the flywheel.

4.3 Protocols

If I were a Berachain ecosystem project, I would receive investment from VCs operating Berachain validators or liquidity funds large enough to deposit a lot of liquidity in my token pool during the investment round. Conversely, this means that VCs interested in Berachain ecosystem projects can get differentiate themselves by operating validator in Berachain or have large liquidity to deploy in Berachain.

Also, as protocols like Infrared, Beraland, Kodiak Finance, and HoneyJar DAO are currently participating as validators in the testnet, if possible, running validators themselves can be a way to minimize value extraction and stably provide liquidity to their native tokens. Of course, if the block verification runtime is not consistent, it may lead to worse results than not running it.

5. Q&A (Last updated in 03.07.2024)

I will continuously organize common questions related to Berachain that I have received here. Also, I have unresolved questions, so I will record them here and update them if they are resolved.

5.1 Resolved Q&A

Is $HONEY an algorithmic stablecoin?

No. It's an over-collateralized stablecoin that can only be minted with $USDC, essentially a Berachain-style wrapper of the existing USDC. In the case of borrowing, it seems possible with $WBTC or $WETH instead of $USDC, but naturally, it's possible to borrow according to the LTV of each asset.

Aren't Berachain stakers exposed to IL (Impermanent Loss)?

Yes. That's why IL hedging protocols like Smilee Finance, which are about to launch in Berachain, are expected to be popular.

Is it possible to participate in PoL with arbitrary tokens?

Yes and no. Initially, only Berachain BEX's house pools receive $BGT emission, but as mentioned earlier, any pools in BEX can receive $BGT emission if they pass governance by validators. Therefore, the key is whether it passes governance by Berachain validators.

Is the contract that can receive $BGT emission limited to BEX, or can third-party DeFi protocols also receive it if they pass governance?

Yes, any third-party apps's contract can recieve $BGT emission if it passes the governance.

How will the initial validators be allocated $BGT, i.e., voting power?

It will be done by foundation delegation program.

5.2 Unresolved Q&A

6. Conclusion

The reason I keep feeling the urge to write tweet or article about Berachain more is probably because it's the project with the biggest gap between its impact evluated by me and other people's perception. Of course, as of March 2024, compared to October 2022, more builders, researchers, VCs, and others in the crypto industry are interested in Berachain. However, the gap between the impact of Berachain I think and the actual perception is still large. In Korea, this gap seems even larger, which is... meh.

I tend to be interested in products that I think are undervalued by others, and in this regard, Berachain has been at the top of my interest list since October 2022 until now. I sincerely hope that more people will take an interest in Berachain and properly evaluate its impact, so that Berachain will gradually fall in my interest ranking.

If you are a current ecosystem participant (VC, validator, builder, ...) and would like to talk more about Berachain with me, or if you are interested in doing something related to Berachain, please feel free to contact me via email, Telegram, or DM!