Move over Spotify, Google Pay has a wrap!!

Google Pay India has given millions of its users a walk down the memory for last 5 years. All banks have this information (in fact more with NEFT, RTGS, Demand Drafts, etc), so does RBI, so does the Income Tax department, but Big tech and Fintech are keeping us consistently engaged and entertained.

2 Bn daily transactions. 10 Mn+ merchants use QR code. - Google Pay

Two thirds of the transactions happen beyond top cities across 3 lakh villages. Those free Sticker Kits for Google Pay QR code have done way more for payments in India than old PoS (point of sale) machines that didn’t work work at the cashier counters. A tip of hat to the sleek phone shaped PoS machines that announced receipt of payment with the amount so that no one has to look at tiny screens or wait for paper receipts - they are better off on your own mobile with a transaction ID, your own UPI address and recipients UPI address. Being in the Goblin mode using Google Pay, I’ve come across only Paytm’s PoS devices, there are likely more setting the standards. While female users choose to use Google Pay, male users prefer using Amazon Pay, Paytm, GooglePay – lines up with the author of this article. Source: ET

Giants standing on the shoulders of UPI

The immense success of Google Pay lies is how ridiculously good UPI is and how well Google Pay has utilised it to onboard merchants and individuals. Google tops the charts with 38% market share in e-wallet users, closely followed by Amazon Pay at 37% with its instantaneous offers every time you order from Amazon. Homegrown, post-IPO battered Paytm at 36% is a stiff competition at number 3.

Out of 376 banks and payment service providers, Bigtech and Fintech shine and RBI has aptly rapped banks for being nowhere in the top market share. Retail business is lot of hard work though and most banks focus on mass affluents or minimum balance of average Rs. 2000. UPI has been able to capture that segment as well. RBI reported average person to merchant transaction value at Rs. 800 and it’s only growing.

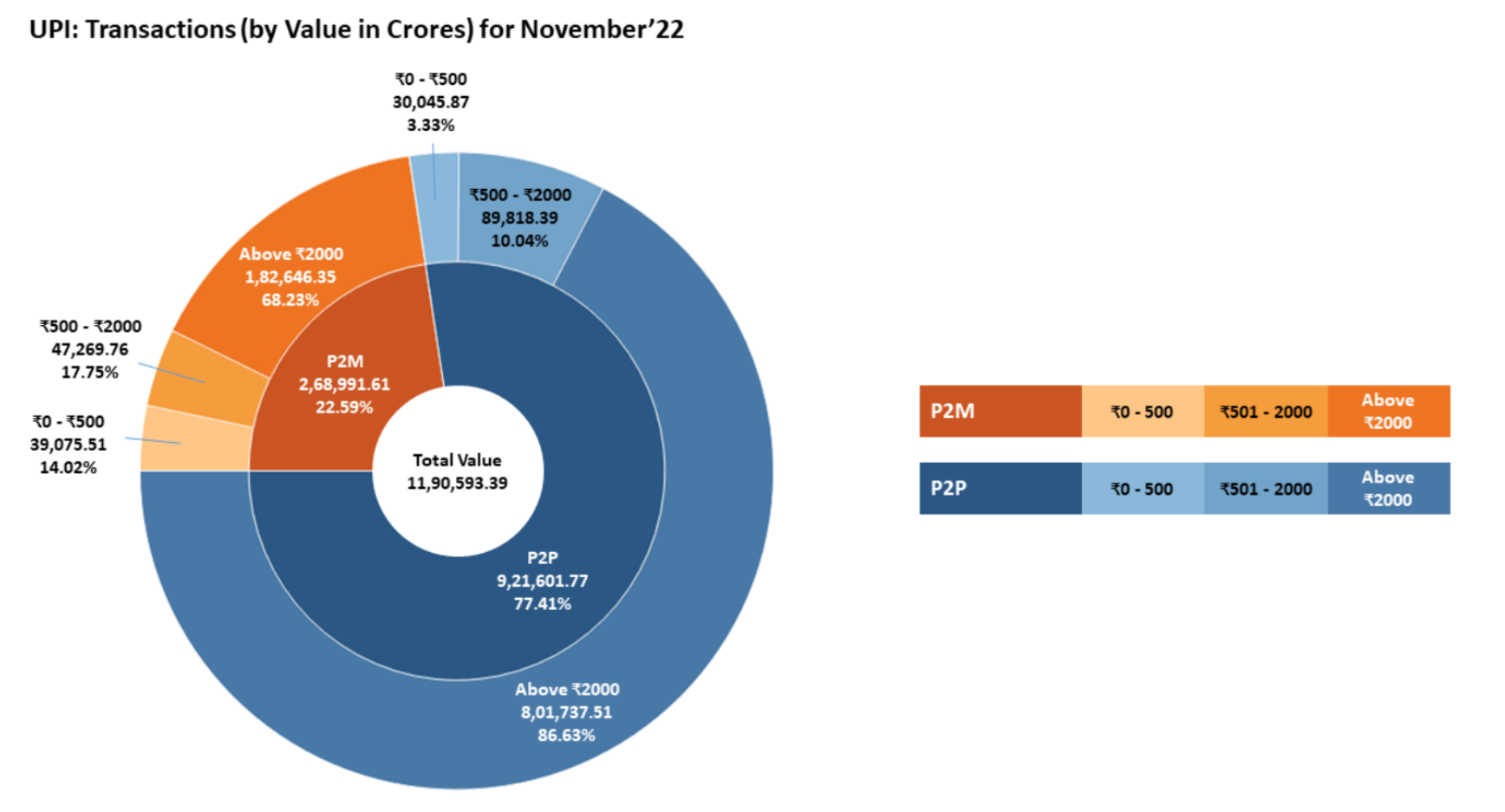

86.6% of UPI person to person payments are above Rs. 2000

68.2% of UPI person to merchant payments are above Rs. 2000

UPI was launched in 2016, following IMPS and USSD. IMPS itself felt like magic when we could simply send within the existing banking mobile apps, unlike USSD (*99#) which is a session-based basic banking that doesn’t require the Internet. While Google recommended US Fed to have a look at UPI in 2019.

Currently, in Nov’2022 UPI crossed Rs. 11,90,593 Cr worth with 730 Cr transactions, towering IMPS 46.3 Cr transactions. (Source: NPCI) As I pen this, Machankura in Africa is using USSD for bitcoin wallet payments without a smartphone (that’s for another post, getting back to UPI)

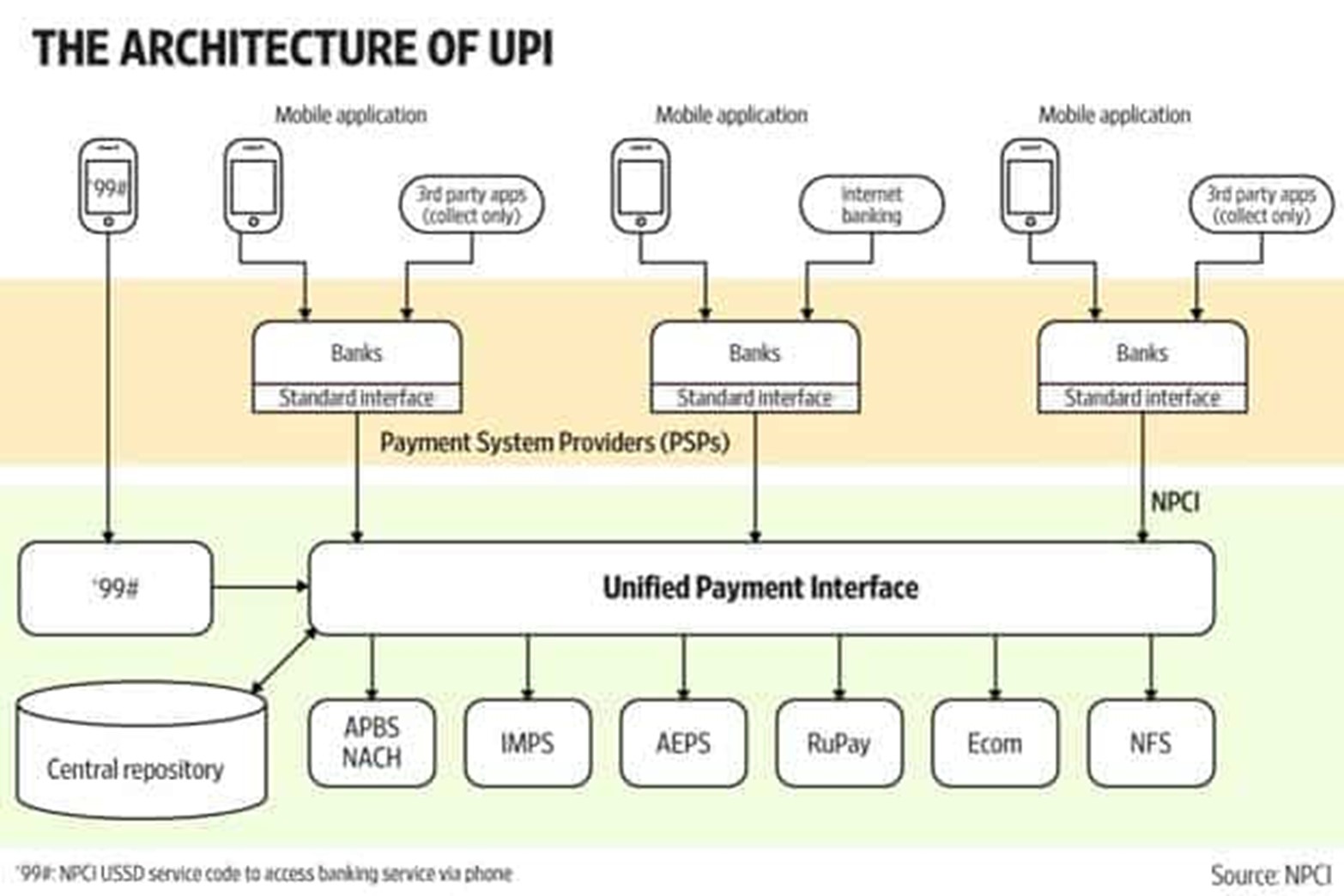

NPCI started off with ecosystem with a role for all - Payer PSP(Payment Service Provider), Payee PSP, Remitter Bank, Beneficiary Bank, NPCI, Bank account holders, Merchants.

UPI Product: 24x7x365 money transfer on virtual address instead of account numbers details for increased security, single 2FA authentication, QR code payments, payments to contacts using a single click. Winning UX is usually as simple as single click. Of late, UPI can be paid via pre-defined IVR number, missed call pay, OEM-enabled Payments and sound technology using mobile.voice@psp format. (Source: NPCI)

Users simply have to create a virtual id, select existing bank account and create a 4 digit PIN. No KYC is required again because APIs connect to banks directly. No documentation, no account number or bank login details. From shopping to donations, it serves all sending money and requesting money scenarios. More details

UPI Architecture: UPI is a cheap, secure, reliable, mobile-first, interoperable, open-source, instantaneous settlement and both pull and push platform -as it was first described in 2016. It has been free for end users, who are infact getting cashback and constant gamification glues.

UPI’s uptime has been 100% in June’2022 as well as in Nov’22, with every spurt in volumes, uptime is back to 100% which is feat when we hear about unexpected system failures around the world. Although UPI was hit with downtime during start of pandemic lockdowns.

UPI as a fund transfer system enables real-time movement of funds. UPI as a merchant payment system also facilitates real-time settlement, as against the T+n settlement cycle for card settlements. The settlement amongst participant banks is on a deferred net basis.

One of the most fascinating experiences was how smoothly a transaction went through despite the bank with which I hold account was having payment glitches. The transaction was initiated in Google Pay, from my Bank A to beneficiary’s Bank B. And it was getting attempted to pass through by two additional banks, Bank C and Bank D with SMS messages from both C and D, without me having UPI linkages to any of the banks C or D. This was preemptively done before a transaction failure. UPI seems to have solved its transaction drops with banks supporting real time in case anyone of the larger volume handlers are not functioning. Would be happy to hear more if anyone knows how exactly does this work!

The cost of UPI far exceeds the government subsidiary of Rs. 1300 Cr, given the sheer volumes with zero MDR and zero customer fees. Payments Council of India seeks Rs. 8000 Cr as banks have not been sharing the costs with payment aggregators (Source: ET)

UPI is clearly is preferred by any small to mid sized shop that has to pay MDR to Visa or Mastercard and ask customers to pay it else to use UPI/cash. A cash equivalent in digital form! Is the digital rupee an answer to reduce cost of settlement, intermediaries and inefficiencies of business declines and technical declines? Or will UPI itself get on a blockchain and be the Web2.5 product in near future? We are waiting to hear from NPCI.

PS: Meanwhile, Google Pay India's Twitter account's last tweet was in April 2022. Probably silently working hard to shine, away from the cesspool. Binance users can now purchase crypto using Apple Pay and Google Pay, wonder when's that coming to India.