From Wall Street to Web Street?

CupOfCrypto

4 min read·

History Of Equity Raising

Traditionally fundraising for companies and startups involved putting together a pitch deck for the executives of a fund or Angel Investors. If it met the qualifications of the prospective stakeholders, they would offer Equity-Based investing, which is the process of investing money in exchange for a percentage of ownership in a company which allows the founder of the startup to access funds for company expansion and growth meanwhile the investor gets security and control over the business to some degree to provide oversight and direction.

Drawbacks of Equity Raising Investor POV

The consequences of equity raising lie in a few different areas for investors, such as high minimum investment thresholds often being in the few to a couple hundred million range on average, creating substantial risk for loss of investment. There is also the risk of being illiquid as these investors and funds have their money tied up for a set period which can quickly lead to a prisoner dynamic if the company fails to deliver. Management duties also tie up investors as they are not only investors but owners of the company; therefore, they are expected to oversee the company's expansion via identifying their target audience and general operations if they acquire enough stake, as well as managing internal management, which is time intensive.

Drawbacks of Equity Raising Founder POV

There are also consequences of equity raising for founders as well such as pitching your idea to multiple firms for months and or years if the vision is not entirely grasped by prospective investors or due to the founder's inability to compose a sound business plan; therefore, large amounts of time are wasted. Another hindrance of equity raising for founders is the equity portion itself, as a founder may end up giving a bigger stake in their company than they want to as a means to secure funding; if prospective investors perceive your business as risky, they might want higher stake with a disproportionate amount of money invested, but even then this does not guarantee that you will not need to seek out more funding eventually which also leads to more equity giveaway furthermore if the market climate changes such as a downturn risk appetite will be reduced. Many investors will avoid your startup together as they will be taking a higher asymmetric risk due to stepping in on later rounds.

Alternative Types Of Fundraising

Business Loans: Business loans are fairly straightforward, just as any other type of loan; you are approved for a set amount based on creditworthiness in exchange for repayment of the loan in a fixed timeframe occupied by an interest rate.

Accelerators: Accelerators should be thought of as a launchpad for startups that are past the idea stage as they usually have prototypes or are in pre-production but need help with other aspects of the business, such as production funding and management; here, they receive mentorship and build connections in their industry with investors in exchange for equity although it should be noted that these programs are usually short-lived lasting about three months in duration.

Equity raising was disrupted in the Web 2.0 era with the rise of crowdfunding platforms, namely Kickstarter and Republic, which allowed the general public to back potential startups that they otherwise would not be able to due to not being accredited investors; these platforms, however, have their problems respectively Kickstarter, for example, has known transparency, due diligence, and investor protection issues.

have been many projects on the platform that have misled investors, such as the infamous Holus project, which claimed to be an interactive holographic tabletop that could render any 2D image into a 3D holographic these claims turned out to be false; however, as the team behind the project were exposed for just using pieces of glass to reflect the 2D images for the investors of this project this betrayal of trust was horrifying as per Kickstarter's policy they do not have the authority to issue refunds nor do they verify the claims made by startups on their platforms they do however still make a commission as serving as the intermediary between the backers and creators so although investors were left high and dry and never seen a fully realized product or their funds returned Kickstarter themselves made a profit off the ruse.

Republic is another popular crowdfunding platform that holds 19% of the global market share of crowdfunding; unlike Kickstarter, it has more of an emphasis on actual startups and, to some degree, does proper due diligence on the projects that inhabit its platform; it still falls short of the ideal as even though they market themselves as a democratized investment platform, the reality is investors are still restrained as you can only invest up to 5% of your annual income or net worth in Regulation A securities if it is less than $124,000 which for most of the user base is the majority of the bracket they fall into thus there's a maximum cap for your investments and hypothetical returns in the process.

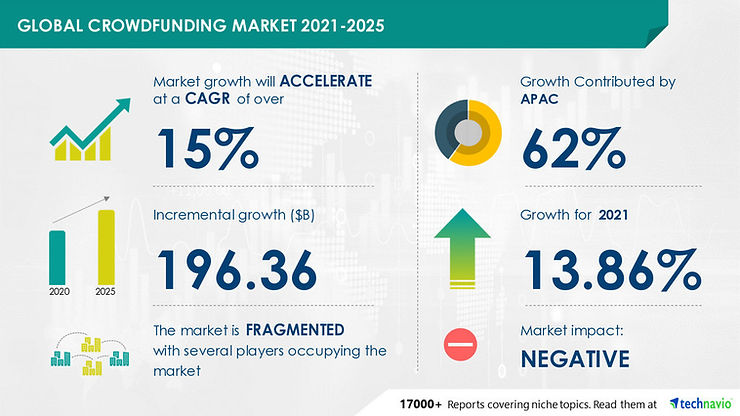

So how will Web 3.0 disrupt equity raising? By utilizing Investment Daos, as they are set to reach 1 trillion AUM (assets under management) by 2032, according to Imran Khan (CoFounder of Volt Capital). The crowdfunding industry is set to reach 200 billion by 2025, respectively, and the intersection of these industries will see massive growth. As they solve the problems non-accredited equity investors face in Web 2.0, such as the lack of transparency relating to funds with the platform they are interacting with, as truth is tokenized on-chain with the use of smart contracts leading to a restoration in investor confidence.

Another problem that is solved is the core issue of non-accreditation itself, as since investors are free from federal identification standards, it further lowers the capital limit. It expands potential investment opportunities for wealth creation. Investment Daos can also solve the locked liquidity problem equity investors face in early rounds with the introduction of ERC standards such as ERC-3525 which allows a token to have fungible quantitative properties as well as descriptive attributes; this allows the emergence of an on-chain OTC market which also bolsters transparency.

Last but not least, the organization's governance structure allows for dynamic governance and explosive capital deployment due to the lack of intermediaries slowing down crucial processes such as payment settlement and market participant misalignment. Information asymmetry is large among participants as well, allowing potential investments to be examined by a multitude of members, therefore, leveraging the knowledge base of multiple industries, which gives insight into how prospective investments are disruptive. The asymmetrical design of how information is spread and retained at various levels of the organization allows for better internal communication, thus allowing for better capital and labor alignment. Eventually evolving to the conception of internal incubated token raises.

Subscribe to Eosphoros Research

<100 subscribers

Exploring the intersections of Web 3.0, Philosophy. Technology, and more