GM PRO DOers!

Launched in 2017 on Ethereum, Maker stands as one of the earliest applications developed on a blockchain.

Fast forward 7 years later (to today) and Maker is:

Generating over $30 million per month in revenue

💰 Holds more than $5 billion in its treasury

🔒 Has more than $8 billion of TVL on its platform

Despite all of this, $MKR has a fully diluted valuation (FDV) of less than $2 billion. 🤯

If you’re not aware, Maker is developing the $DAI stablecoin, which is the main source of Maker’s revenues.

In recent events, Maker’s centralized competitor, Cicle ($USDC), has recently filed for an IPO in the USA.

This could mark a significant turning point in validating stablecoins and driving their mainstream adoption, which could be a catalyst for Maker.

Even before Circle’s IPO, Maker was looking like an undervalued asset, mainly because approximately 15% of its token supply was being force sold by specific funds, so the price was being held down.

Looking ahead, there are some interesting catalysts coming from a soon-to-be updated $MKR tokenomic structure, an ecosystem rebrand and the potential of “The End Game”.

…more on all of this in just a second.

What’s the opportunity for you?

While $MKR is already up 3.5x from its lows in December 2022, it still has 3x to go before reaching its previous all time highs from last cycle.

This makes $MKR a potential candidate to outperform our base asset, $ETH.

I’ve been watching this for a few months and I wish I wrote a PRO report sooner, (I had no time over the holidays!). But the story of Maker and the chance to see some exciting events happen this year is something I really want to share with you now.

Here’s what Maker has going for it this year and what we’re going to explain in this report:

Earning $30 million monthly with significant growth potential and a reliable revenue stream in all market conditions

Their main centralized competitor is about to go public

Forced selling of $MKR by large funds has recently stopped

A rebrand in the assets to simplify the MakerDAO ecosystem

Upcoming "stock split" to reduce $MKR's token price (from $2,000 to less than $1)

Implementing the End Game strategy to position Maker as the most intricate and decentralized protocol and DAO in the crypto space

Ok, before we get too far ahead of ourselves. Let’s get everyone up to speed on just what Maker is and clarify the pieces of its ecosystem.

What is Maker? 🤔

The idea behind Maker was conceived back in March 2015 and brought to reality in 2017. Since then, Maker has been operating as a decentralized protocol running on the Ethereum blockchain.

It operates like a global reserve bank, introducing the concept of DeFi to the wider finance world.

The primary goal of Maker is to provide a USD stablecoin known as $DAI.

The protocol employs a system where users can collateralize assets like $ETH, liquid staked $ETH, $BTC, and other established tokens on Ethereum, to generate $DAI tokens.

$DAI is designed to maintain a stable peg to the U.S. dollar. This stability is maintained through overcollateralization; users need to lock in more value of assets than the $DAI they generate.

Originally, Maker was created by the Maker Foundation, which held control over the protocol's contract during its launch.

However, on March 25, 2020, the foundation transferred control to MakerDAO, a DAO consisting of $MKR token holders.

MakerDAO's decentralized governance model involves $MKR token holders who make decisions around adjusting interest rates, determining collateral types and managing the overall debt limit.

So to be clear, here are the following pieces of the ecosystem:

Maker - A DeFI protocol on Ethereum

MakerDAO - The governing body of Maker

$MKR - The governance token of MakerDAO

$DAI - The stablecoin

One other important note about Maker is that the Maker team never built a Maker front-end for users to interact with it.

Instead, Maker focused on building the protocol and allowed other teams to build front-end interfaces which users could interact with.

Maker should be thought of as a decentralized protocol on Ethereum that apps can be built on top of, rather than an app itself.

The Solid Fundamentals Of Maker 💪

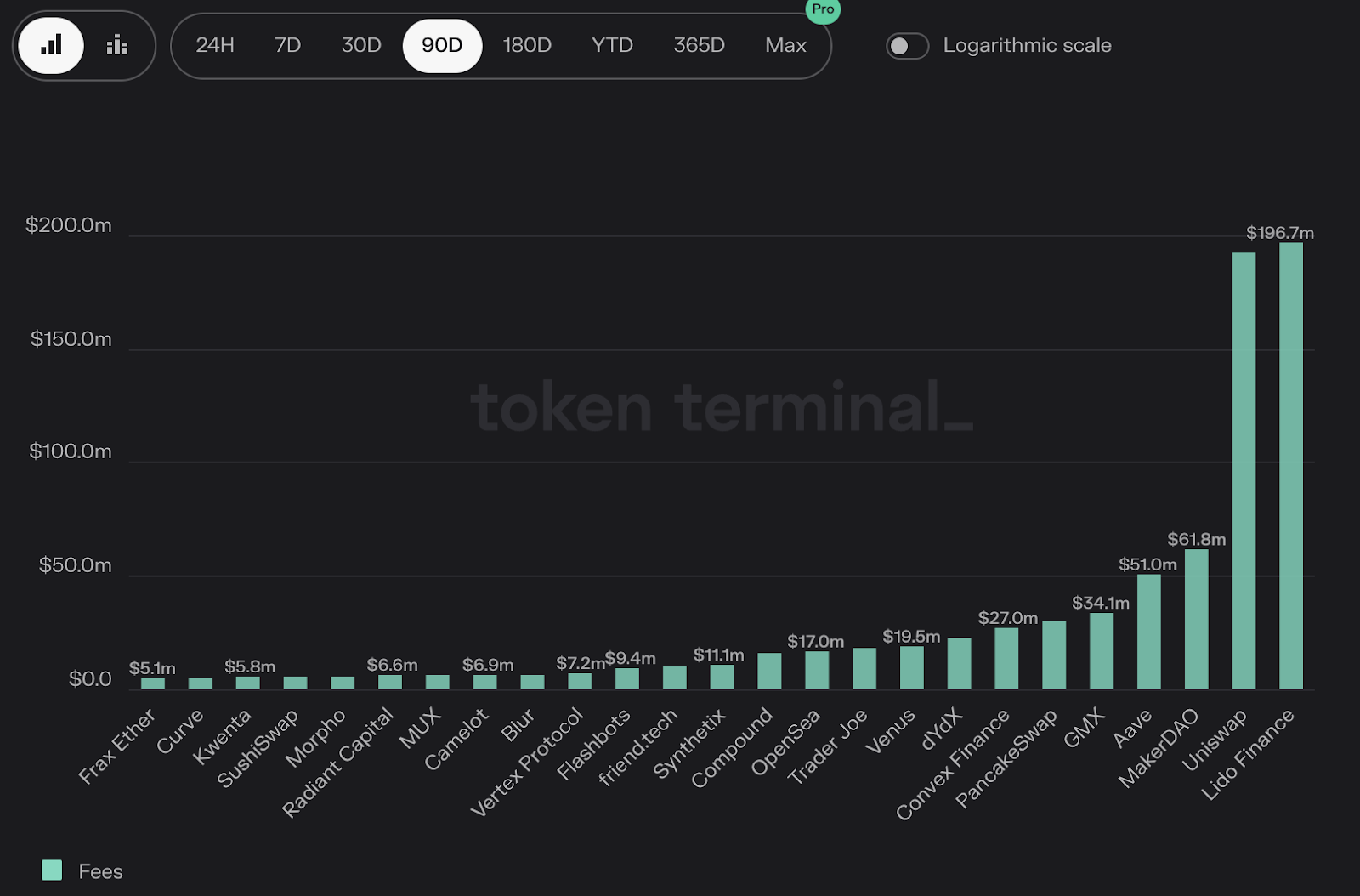

In the last 90 days, Maker is 3rd among all onchain applications and protocols in terms of generating revenue.

According to Token Terminal, Maker has generated more than $60 million since mid October.

These numbers are picking up as we move into a bull market and the appetite to take out leverage onchain increases. We are already sustaining higher revenue numbers than last cycle!

Maker generates revenues in a few different ways – some onchain and some off-chain.

In terms of the onchain revenue (which is trackable in real time), the bulk of Maker’s revenue comes from lending interest.

This simply means that users collateralize their $ETH and receive $DAI, but they pay an interest rate for it.

Another significant onchain revenue source is liquidations, which primarily occur during bullish market peaks and as markets transition into bearish phases, as shown in the red section below.

However, Maker has a significant source of revenue off-chain too, which Token Terminal is not accounting for.

As mentioned above, Maker has a treasury of more than $5 billion. Almost half of that is sitting in the U.S. Treasury Bills (T Bills).

For the last year, U.S. T Bills have been earning over 5% due to higher interest rates.

With $2.1 billion sitting in T Bills, Maker has been earning close to $10 million per month off the U.S. government!

Below is a chart of Maker’s annualized revenue (taking past revenue and projecting on a 12 month basis).

Almost 50% of their revenue comes from T Bills currently.

The numbers above are accounting for all the slow months of Maker earlier this year, but with the combination of crypto prices rising and interest rates still high, Maker is generating more than $30 million per month currently.

If that remains or continues to pick up, Maker’s annualized revenue would be more than $360 million. 😲

Now, of course, the revenue from T Bills won’t last forever.

If (when) rates go back to near 0, this revenue source will diminish quickly.

However, if rates return to near zero, it's likely indicative of a full-on bull market, which would significantly boost Maker's lending revenue.

Maker has found the perfect 2-sided business model, similar to that of Coinbase.

A business model that generates significant revenues when rates are low and a treasury that generates significant revenues when rates are high.

You can see the share of revenue between sources below…

Additionally, if we look at the TVL (total value locked) in Maker, we can see that it has a long way to go to get back to the levels it saw in the last bull market.

Maker has less than half the value in its smart contracts from last cycle, yet is already earning about the same in lending fees from last cycle.

As prices of assets rise and appetite for borrowing increases over the next 1-2 years, Maker’s revenues are set to dominate those from last cycle.

If they were able to accumulate $5 billion in their treasury from last cycle, think about how much more they can accumulate this time around!

Ok, so we’ve established that Maker prints money and has potential to print a lot more during both bull and bear markets.

We’ve also established that Maker is already making more $$$ than last cycle, yet we’re still very early in the current cycle.

So what does this mean for us? What’s the opportunity?

Well, $MKR is still 3x below its ATH from last cycle, even though it already has better fundamentals.

So what’s holding $MKR back?

Why Maker Fundamentals Don’t Match $MKR Price 😕

During the bear market, $MKR was hit hard, falling 90% from top to bottom.

Like most tokens in this space, $MKR more than doubled throughout 2023, going from $600-$700 to $1300-$1400 in Q3.

However, in Q4 2023, the token didn’t break out of its range while many other tokens were skyrocketing.

This was when I started paying attention and was trying to figure out what was going on with $MKR.

I realized that there was one main reason that the token was lagging the rest of the industry…

Big VC firms were selling their $MKR tokens in mass. Paradigm and a16z sold most of their holdings while CMS sold some too.

It’s estimated that 15% of the total $MKR supply was sold off by these big firms, which would put a lot of selling pressure on the token and also deter new investors from diving in.

The capitulation in MKR this year has been significant. No fewer than 15% of the supply has been hastily sold by large funds, the last of which is finishing now. This supply has been absorbed by the ~$120M yearly buybacks from MKR earnings and new MKR buyers.

We are betting…

We are betting…

182

182

I don’t know exactly why they were selling, but part of it is due to the confusion and debates around “The End Game” plan that was proposed in 2023 (more on this later), which saw some long-term contributors leave the ecosystem.

The other part is due to Maker’s recent reliance on RWAs (T Bills, Real Estate, etc.) on their balance sheet rather than crypto assets, adding third party risk to its balance sheet.

Regardless, there’s a few positives that arise from this:

First, the selling from big firms is over, removing a massive sell pressure from the $MKR token.

Second, when VC firms hold a large % of a tokens supply, it can be a reason that others would not invest in the token due to centralization risks. This has now been alleviated.

$MKR price has since jumped from $1400 to $2000+ (in a matter of weeks).

Future Catalysts for $MKR 🚀

Now that the selling is behind us and $MKR is proving to remain one of the top revenue generating protocols in crypto, what’s next?

What could drive the catalyst for $MKR’s next big leg up?

Big things are coming to Maker in 2024, here’s what you need to understand:

1. A Maker Rebrand

Maker is doing a complete rebrand at some point this year. Maker is one of the oldest protocols and currently it’s an extremely confusing ecosystem for new people to understand…

There’s the $MKR token, the $DAI token, the Maker protocol, and a MakerDAO governance token. 🥴

The plan is to simplify this entire ecosystem and update its branding to speak to the new entrants of crypto this cycle.

I’m not sure how big of an impact this will make, but with a bull market coming our way and with millions of new people flooding into crypto in the coming months-years, solid marketing along with product market fit could mean big things for attracting new users and investors.

2. A $MKR “Stock Split” (aka Redenomination)

As of today's writing, $MKR’s token price is $1997.

While educated investors understand that the price of a token is irrelevant and that what matters is its market cap, retail investors don't quite get this.

When they see a token sitting at $2000, they think it’s too expensive and they are too late to invest. Instead, they go for the meme coins that are priced at fractions of a penny.

As part of the rebrand, MakerDAO will be redenominating its token 12,000/1, putting the $MKR token price under $1.

Again, I’m not sure how much of an impact this will make, but we haven’t seen many rebrands or redenominations of tokens in crypto yet as the industry is still so new.

It will be interesting to see what sort of impact this makes during the coming bull market.

3. Circle files for an IPO

Maker’s main competitor is a centralized company in the USA, Circle, the creator of $USDC.

Last week they announced they have filed for an IPO. This IPO will send a signal to the TradFi world that stablecoins are a legitimate innovation and something they should be looking into.

It’s likely that as they do their due diligence, they will learn about Circle’s decentralized competitor, Maker, at some point down the rabbit hole.

Even if TradFi doesn’t (which they will), Crypto Twitter and retail investors will likely be all over this as a speculative bet as the Circle IPO comes to fruition.

As an example, when Coinbase first announced they filed for an IPO back in December 2020, Uniswap, Coinbase’s decentralized competitor, skyrocketed from $3.76 to $20 within weeks.

Now to be fair, this was also at a point where the bull market was starting to take off and Uniswap was the main DEX being used, so its token was likely going to do well regardless.

But, it’s likely that Coinbase’s IPO had some impact on the $UNI demand, especially as researchers started to compare their revenues, expenses, etc.

4. The End Game

Rune, the founder of Maker, shared a plan in 2023 called “The End Game” of Maker in their governance forum.

It includes 5 phases of complex and significant changes to Maker (including the rebrand and redenomination above).

While I won’t go into full details on this as it’s extremely lengthy (you can review a summary of it here), the end goal is to create an extremely complex governance system using subDAOs that utilize both the $MKR token and SubDAO tokens for governance.

In the end game, there are a couple really important outcomes relevant to the price of $MKR.

First up, Maker would be by far the most decentralized protocol and DAO in crypto, creating a low-risk environment for applications to build on top of.

Remember, Maker is focused on being a decentralized protocol that apps build on top of, not becoming the user-facing app itself.

In the long run, the idea is that global companies are more likely to build on Maker rather than a U.S.-controlled company like Circle.

Secondly, The End Game would create a scenario where value generated from Maker could accrue to $MKR holders and DAO participants (albeit still not very clear how).

Some of this can occur through buybacks of $MKR (already happening) as well as rev share.

This is something that Uniswap for example (another big revenue generating protocol) has not been able to figure out yet. This is a big reason why $UNI hasn’t managed to retain value in its token since last cycle.

Fundamentals Don’t Matter…

If there is one theme in crypto that we are often reminded of, it's that fundamentals don’t matter.

If they did, how could memecoins gain as much adoption as they do and how could new L1s with no adoption and inflating currencies perform so well?

In bull markets, where there is infinite new demand, fundamentals are definitely not necessary for price to appreciate. Oftentimes narratives can be more than enough.

In bear markets, fundamentals matter a lot more, which is the reason that $BTC and $ETH (as of late), outperform every other asset significantly during those times.

But what happens when a token with a narrative, product market fit AND fundamentals hit at the same time…during a bull market? We don’t really know, as that hasn’t really ever happened…

This is the first bull market that will have apps and chains generating real, sustainable profit. It’s the reason why I’m so bullish on $ETH for this cycle.

Now, all of that said, Maker may be generating significant revenues and have some interesting rebranding and narrative catalysts coming its way, but until $MKR token is accruing value from the protocol, then technically $MKR the token doesn’t have real fundamentals like $ETH does.

This is the thing that applications and protocols need to figure out for long term price sustainability.

$ETH for example, has figured this out. It’s a network that generates millions of dollars in revenue/month and has found a way to sustainably share that value with its network participants.

This is why $ETH is worth more than $300 billion.

If Maker can find a way to accrue some of its value to its network participants, I think it can quickly become one of the top assets in crypto too.

Final Thoughts 💭

To be clear, I don’t think $MKR is going to be the best performing asset this cycle. I’m not even sure it will perform well at all.

What I’m sharing are a bunch of potential catalysts that could make $MKR a hot token this cycle.

There are a lot of “what ifs” and things that need to actually be executed for this to happen.

What I’m mostly interested in is how these upgrades to Maker impact its token price. It’s not often that we get to see a legit project in crypto make a bunch of big upgrades like this.

Even if you don’t invest in $MKR, watching how this investment plays out from the sidelines will be very helpful for future investments across crypto.

Sometimes the best learning is from the investments that you don’t actually make!

Good luck out there friends :)

Thanks for reading. And remember, you're strong, you’re powerful, you’re alpha! ❤️

How'd you feel about our read today?

ABOUT THE AUTHOR

Kyle Reidhead

Founder of Web3 Academy and Impact3

Find him on Twitter

PRO ACTION STEPS

CLAIM PRO NFT

As a PRO, you’re entitled to a PRO or FOUNDERS Pass (NFT), depending on your subscription.

This Pass will grant you access to our token-gated Discord and to other perks such as early access to various protocols and discounts to IRL and online events.

To grab your Pass, simply click the button below, connect your wallet to your Paragraph account and grab your Pass.

TAKE WEB3 INVESTING MASTERCLASS

Learn the best practices to allocate capital and successfully invest in crypto and web3 with our Web3 Investing Masterclass.

This invaluable resource costs $249. But as a PRO, you get it at a 50% discount.

And as a Founding member, you get it for FREE! 🤯

All you need to do is grab your PRO/Founders Pass (see above ☝) and connect your Pass using the link below. 👇

JOIN OUR DISCORD

As a PRO or FOUNDERS Pass holder, you have exclusive access to our token-gated Discord channels dedicated to PRO members!

Upon claiming your Pass, head to Discord and connect your Pass in the #start-here channel (WEB3 ACADEMY PRO category) to unlock access to PRO-only channels!

Disclaimer: This article is for informational purposes only and not financial advice. Conduct your own research and consult a financial advisor before making investment decisions or taking any action based on the content.

Good morning