Is This Web3's Greatest Tokenomic Design?

And no, it's not digital gold...

Kyle Reidhead

11 min read·

GM PRO DOers,

Designing a successful token isn’t easy.

In fact, most tokens in web3 end up doing more harm than good for a business over the long run.

Axie Infinity, STEPN, and Luna are just a few examples of the consequences of poor tokenomics.

Now, it goes without saying that in order for a token to succeed it should retain or appreciate in value over time. If a token can achieve this, it can be one of the greatest acquisition and retention tools of all time. 🚀

But if the token depreciates in value, well, it can also be the worst…

It’s for this reason that tokenomic design is so important. So too is aligning incentives of your token holders with the business.

Whether you’re building in this space and utilizing a token, you’re partnering with an entity that utilizes a token or you’re simply investing across web3, understanding tokenomics is vital.

But it’s also important to note that the best tokenomics will not matter if the product or business behind the token doesn’t provide real sustainable value to its customers and users. 🤷

Tokens are a tool to amplify your business, they aren’t the business itself.

In today’s on-chain report, we are going to uncover the tokenomics of a technology that has both found incredible product-market fit as well as created what I believe to be the greatest tokenomic design for any fungible asset in web3 so far.

That technology is the Ethereum Blockchain and its native asset ETH.

Below we will explore:

The relationship between the Ethereum Blockchain and ETH 🧑🤝🧑

The fascinating design of ETH’s tokenomics 🪙

How Ethereum has used its token to align incentives across multiple participants within its ecosystem 📈

This isn’t meant to be a bull case for ETH (though it may be that too), but instead a means of inspiration and understanding for how a token should function within an ecosystem and community.

But first, a quick refresher on the foundations of tokenomics.

What Is Tokenomics?

Tokenomics is a combination of two words “token” and “economics,” and refers to the supply & demand characteristics of a digital asset. It takes into account things like issuance, attributes, distribution, supply, demand, and other characteristics.

Now, the economics of an asset is nothing new. We can evaluate the economics of any asset in the world, not just crypto.

The one many of us are familiar with and use the most is fiat currency. Rather than “tokenomics” however, we use the term “monetary policy”.

What policy is that?

In the fiat system that we use today, there are a few boomers in Washington that take a look at some spreadsheets and charts about how our economy is doing on a monthly basis.

Based on those numbers they either create a bunch of fiat out of thin air to stimulate economic activity (this is called quantitative easing or, in crypto terms, money printer go brrrrr).

But taking this action also reduces the value of our hard-earned money due to inflation and an increased money supply.

Or, they decide to stop creating new money to slow economic activity (quantitative tightening) with the goal of having most of us buy fewer things and ultimately lose our jobs…

This action lowers the value of everything we own while increasing the costs of everything we currently borrow (raising interest rates).

WTF kind of crazy circus world are we living in? 💀

But that’s the “tokenomic design” we are all used to. It does a terrible job at aligning incentives with participants across the ecosystem nor does it appreciate in value, a direct contrast to the tokenomic design of ETH which we will look at below.

Of course, there are many other assets we could look at in the physical world too, like gold for example.

Gold's “tokenomic design” is simple. It's naturally hard to find and mine, not to mention expensive, so it inflates at about 1-2 %/year, making it relatively scarce versus fiat.

You can think of these assets and their “tokenomic design” as an analog version of what web3 has enabled.

The main difference is that tokens are programmable and their policy can be set and verified by code, rather than set and trusted by a human.

Understanding Web3s Best Tokenenomic Design: ETH

First, it’s important to understand that there is Ethereum the blockchain, and ETH the asset. They are two very different things.

Ethereum uses ETH for 2 main functions:

To secure its blockchain.

As gas to transact on the blockchain.

Ethereum, the blockchain, needs one thing from ETH, the asset, and that is for its value to go up.

Why? The higher the value of ETH, the more secure its blockchain is. 🔒

The more secure Ethereum is, the better the product it provides to its customers. So let’s keep this in mind while we explore Ethereum's tokenomic design.

When evaluating tokenomics, at the root of everything is supply and demand.

It doesn’t matter what type of asset it is, supply and demand are what dictate its price (assuming it’s on an open market and not regulated or manipulated by the government…).

If there are more buyers than sellers, the price goes up.

If there are more sellers than buyers, the price goes down.

If there are the same amount of buyers as sellers, the price stays the same.

That’s the foundation of open markets. The goal then of any asset is to figure out how to create more buyers/holders than sellers and/or its rate of new supply (inflation).

Enter ETH, an asset that has probably the most interesting and complex supply and demand dynamics in the history of any asset.

It’s an asset that has had many iterations to its monetary policy over the last 8 years. While that policy is still nearing completion, I believe it already has the greatest tokenomic design in web3.

So let's break it down…

The Supply Dynamics of ETH

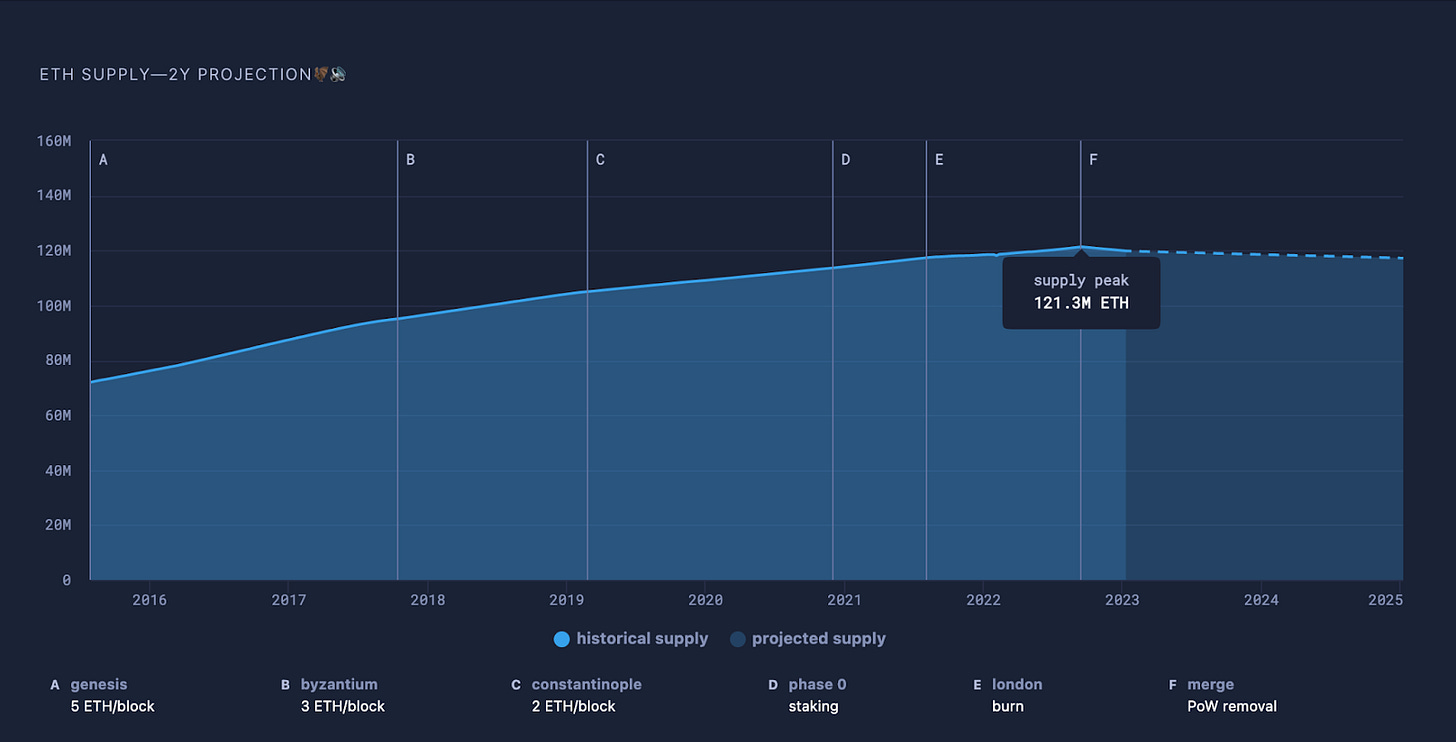

Let’s start with the supply side of ETH as it has changed the most over time.

Supply = how much ETH is in existence.

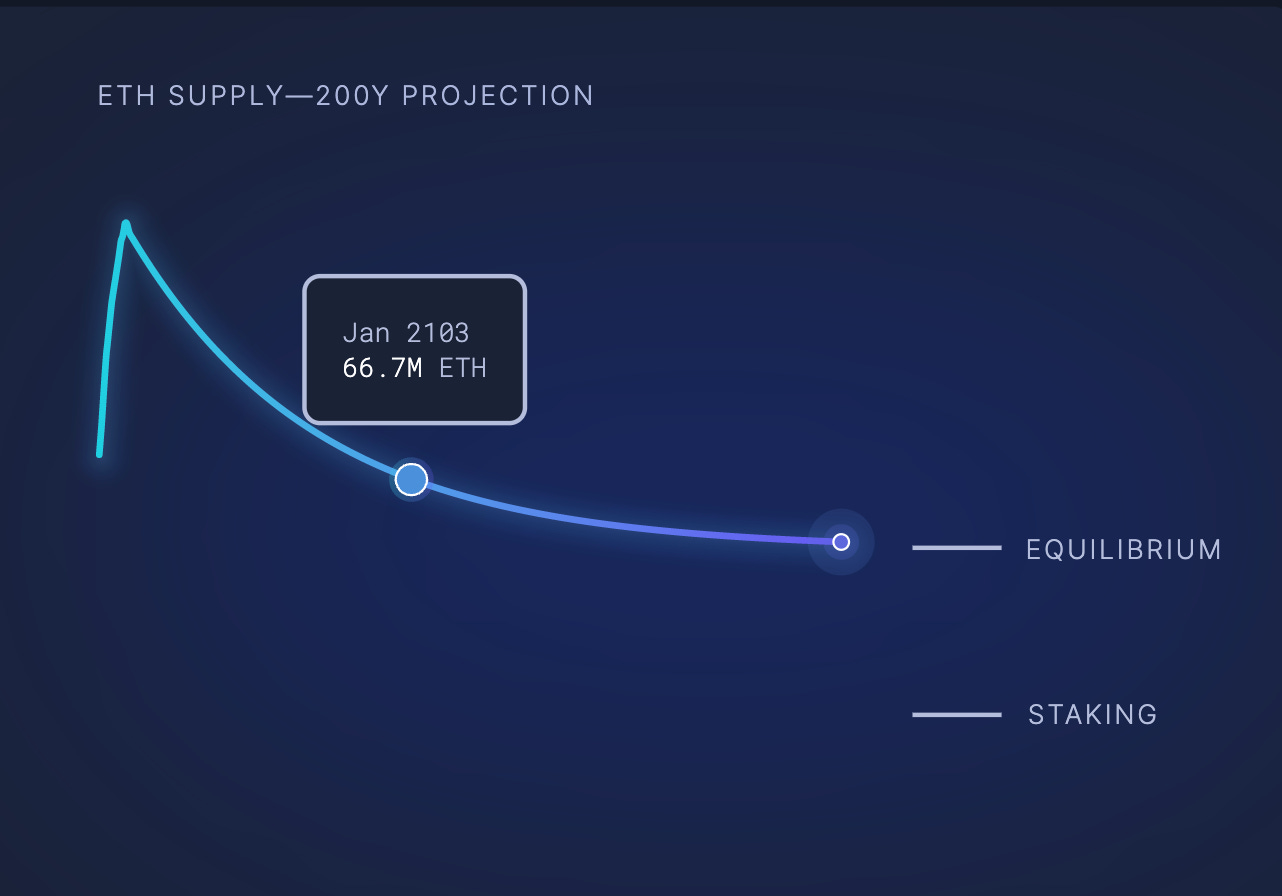

In the chart below, you can see the increase in ETH supply up until 2023, where it is then projected that supply will decrease moving forward.

But why was the ETH supply previously increasing?

The Ethereum blockchain creates (issues) new ETH on a daily basis to pay those who secure the blockchain (aka validators and previously, miners).

Validators are hundreds of thousands of machines around the world that hold 32 ETH in a smart contract and run a machine that verifies and approves the transactions that make Ethereum function.

As a means of incentivizing people to use their own electricity and equipment to run an Ethereum Validator, Ethereum issues new ETH to pay these validators for their services.

As we learned above, however, creating new supply is a form of inflation and this is not necessarily a good thing for any financial asset as it means we always need more buyers for the price to stay the same or increase.

In fact, over-inflating currencies were one of the main problems which brought down the Axie Infinity and STEPN ecosystems (FYI they are not dead, they are just not thriving like they were when their tokens were at a much higher value). ❌

This is where the beauty of ETH’s tokenomic design comes into play.

In September 2022, Ethereum lowered its issuance rate (inflation rate) of ETH from 4.61 %/year down to ∼0.52 %/year, a whopping 88.7% decrease in its yearly issuance rate.

That is a very big drop in terms of new supply issuance. To put it into perspective, Ethereum went from issuing 4,931,000 ETH/year down to 622,000 ETH/year.

So based on the formula above, if demand simply stayed the same, the price would have no choice but to increase due to the restricted supply.

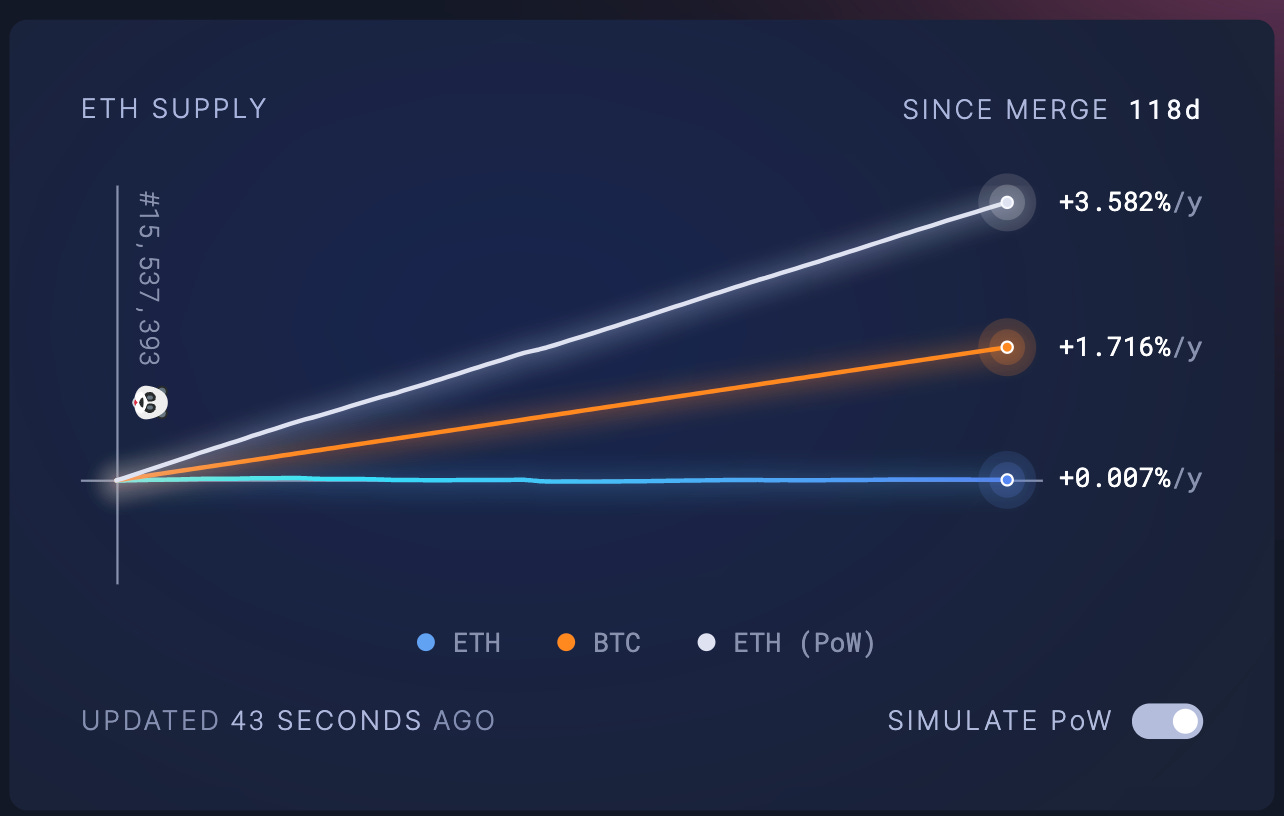

To clarify, Ethereum was able to lower its issuance rate so significantly due to its merge from Proof of Work (PoW) to Proof of Stake (PoS), effectively altering how the blockchain is secured to a more optimal and much cheaper security system.

The chart below compares how the ETH supply would increase if it was still using PoW (white line), versus its current state in PoS (blue line), and finally, versus Bitcoin’s current inflation rate (orange line).

Now, if you’re paying attention to the details you may be wondering why the inflation rate above says 0.007%/year rather than the 0.52%/year I mentioned above.

You may also be wondering why the supply of ETH is projected to decrease in 2023 if Ethereum is still creating new ETH to pay for its security each day.

The answer to both questions above is EIP 1559 or “the burn”. 🔥

This is a mechanism that was launched on the Ethereum Blockchain in August 2021, which effectively burns ETH and creates a deflationary mechanism to the supply of ETH.

Here’s how EIP 1559 works:

To execute any transaction on Ethereum, users must pay a minimum fee (aka a base fee) in the form of ETH for it to be valid.

That base fee varies depending on the network activity, otherwise known as the demand for Ethereum's blockspace (more on this in the demand section below). Through EIP 1559, that base fee is now burned and removed from the ETH supply.

What this means is that if the activity on Ethereum increases, more ETH is burned.

So if more than 0.52% of ETH is burned every year, then ETH becomes a deflationary asset, an extremely uncommon phenomenon for any financial asset, in crypto or otherwise.

Currently, if we look at the burn rate in the last 30 days and average it out over a one-year timeframe, we would burn 625,000 ETH in the next year while we only expect issuance of 622,000 ETH during the same time frame.

This would result in ETH’s supply decreasing by 3,000 even during a bear market where activity is significantly lower.

But if we look at the average burn rate since EIP 1559 launched, which includes activity from the middle of the bull run, we see that the burn averages roughly 1,966,000 ETH per year. Remember, issuance does not change so ETH would actually decrease its total supply by 1.10% (or 1,344,000ETH) in a single year.

This is where ETH gets the name: Ultra Sound Money 🦇🔊(playing off the meme that Bitcoin's capped supply of 21 million is termed “Sound Money”).

We can also use the data to project the total supply of ETH over time, which may help in evaluating the price of the asset. Currently, ETH has a total supply of 120,523,822.

But it’s projected that in the next 100 years, ETH’s supply will drop by almost 50%! So if you believe demand for the Ethereum blockchain will increase over time, then you can start to understand what has to happen to the price of ETH 👀

Before you get all bullish, remember, I’m explaining this because the goal of Ethereum (the blockchain) is for ETH to increase in price, in order to make its product more valuable, not to make its holders more wealthy.

Though, as a marketing tool, if it can achieve both then you’re really onto something. 🚀

It’s also worth noting that there is another form of burn that can occur on Ethereum. If validators go offline for an extended period of time, or even worse, are found breaking the rules of the system, the ETH they stake can be “slashed” (aka burned).

This creates a nice feedback loop and aligns the incentives of those securing the blockchain with the asset of the blockchain even further.

I’ll cover more on how the token aligns incentives of various users soon but we first need to dive into the demand dynamics of ETH.

The Demand Dynamics of ETH

What’s so interesting about ETH is that there are two avenues of demand in play.

There is demand for ETH, in terms of more buyers wanting to purchase or hold the asset.

There is demand for the Ethereum blockchain, in terms of users, businesses, robots, and other blockchains wanting to use Ethereum blockspace, resulting in the burning of ETH.

Both avenues of demand can impact the price of ETH and both tend to be synergistic with one another. Meaning, whenever there is more demand to buy ETH, there tends to be more demand to use the Ethereum blockchain and vice versa.

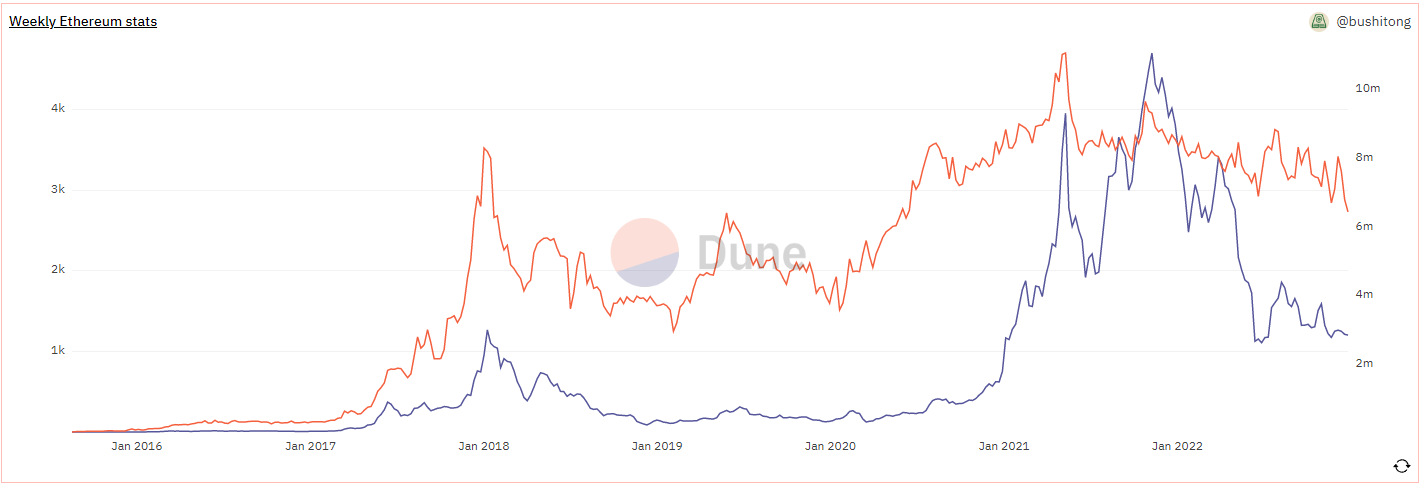

Seen below is the clear correlation between transactions on Ethereum (orange) and the price of ETH (blue).

First, let’s dive into the demand for Ethereum’s blockspace.

If you’re reading this report, I assume you already understand the many reasons why there is demand for blockspace. What I think is interesting and unique about Ethereum blockspace, however, is that it’s not just businesses and users who want to transact on Ethereum, it’s also other blockchains.

Ethereum is becoming the settlement layer of the internet and already has 30+ layer 2 blockchains rolling up their transactions and settling them on Ethereum. You can find a more complete list at L2beat.com.

What this means is that you have humans, businesses from various industries, and other blockchains all fighting for Ethereum's blockspace.

Each of these entities plays by the same rules to transact on Ethereum; They must buy ETH to use as gas and then the base fee of that gas must be burnt. This impacts both ends of the supply and demand spectrum.

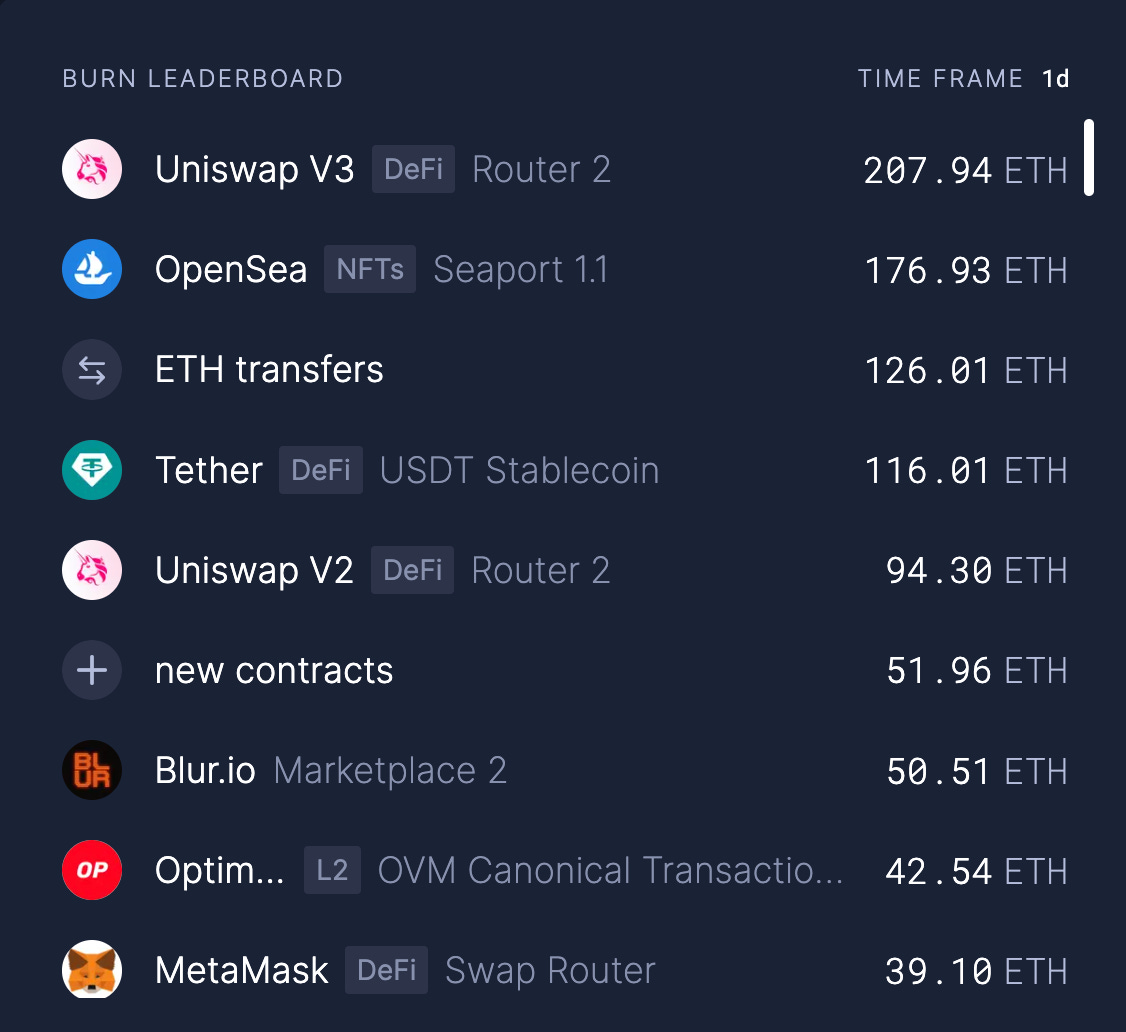

Let’s look further at what participants in the Ethereum ecosystem are burning ETH. Below is a “Burn Leaderboard” showing the top entities that have burned ETH from transactions in the last 24 hours.

You can see that Ethereum’s top decentralized exchange (Uniswap), NFT marketplace (Opensea), and wallet (Metamask) are among the top 10.

So is one of the leading stablecoins (Tether) and layer 2 blockchains (Optimism).

Sitting at number 3 are users simply transferring ETH from one wallet to another.

In the last 24 hours since writing this report, the cumulation of individual users, developers, businesses, and other blockchains has burned a total of 2,249.64 ETH or about $3,148,600 USD.

So again, if we think of supply and demand dynamics, this means that if ETH demand stayed the exact same as the previous day, just by burning this ETH the price would have to go up—a net positive for everyone in the Ethereum ecosystem.

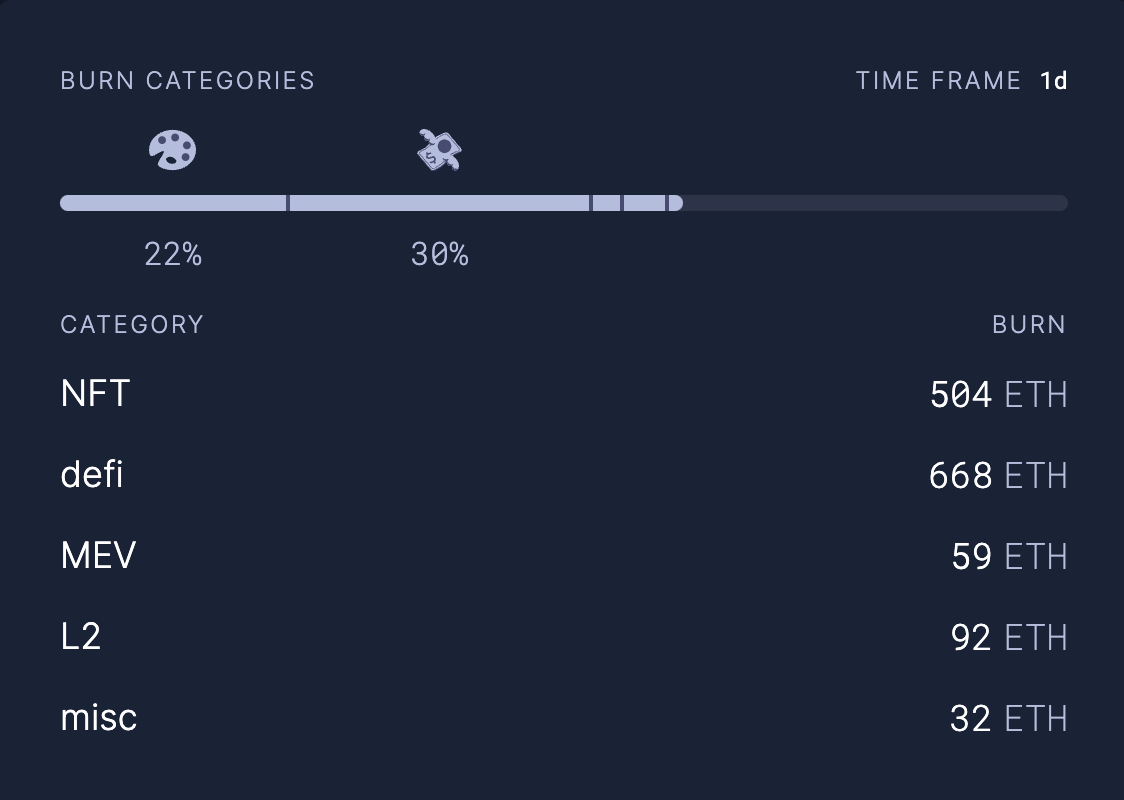

We can even break down the burning of ETH by categorizing use cases to have a better understanding of which parts of the Ethereum ecosystem are burning the most ETH.

Whether it’s NFTs, decentralized finance, or layer 2s, they’re all driving demand for Ethereum blockspace and ultimately burning ETH through EIP 1559.

As I mentioned above, in order to transact and burn ETH, you must also buy the ETH first, which highlights the synergies between both demand avenues. 🤝

Outside of buying ETH to transact, let’s talk about ETH demand from other perspectives.

Of course, like any financial asset people can buy ETH to speculate, which is definitely a large function of ETH demand currently.

However, as more things are created within the Ethereum ecosystem people also buy ETH to spend on the blockchain—meaning, it’s used to purchase other goods, like NFTs, social tokens, and more.

The two most interesting and maybe most significant aspects of ETH demand however are its use as collateral in DeFi and to run a validator to secure the Ethereum blockchain itself.

It’s important to note that the differentiator that ETH has versus any other asset created on Ethereum is that it has no smart contract risk. ETH is the only native token to Ethereum, whereas all other tokens are created by someone or something else and are done so in a smart contract.

In the Ethereum ecosystem, ETH is known as pristine collateral. 💎

This is important because not only does ETH being a pristine collateral create more buying pressure for ETH, but it also temporarily removes ETH from circulation, thus taking ETH off the market.

To be clear, it's not removed for good like the EIP 1559 burn, however, it’s being put to work so it’s less likely to be sold in the immediate future.

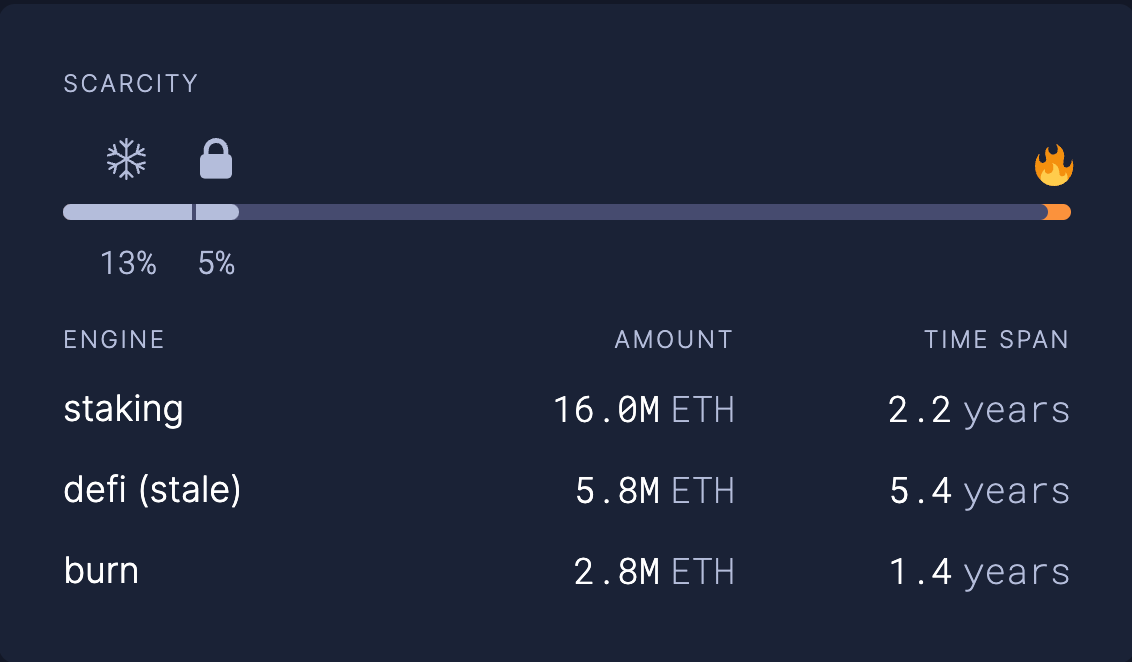

We can see in the table below that currently about 21,800,000 ETH are locked in a staking or DeFi smart contract. That’s 18% of the total ETH supply that is being put to work, rather than being readily available to be sold.

The burn has permanently removed 2,800,000 ETH from its supply, whereas ETH locked in smart contracts has temporarily removed 21,800,000 ETH from circulation.

Finally, if you want to participate in securing the Ethereum ecosystem, you must purchase and stake 32 ETH to run a validator, thus removing ETH from circulation (included in the numbers above).

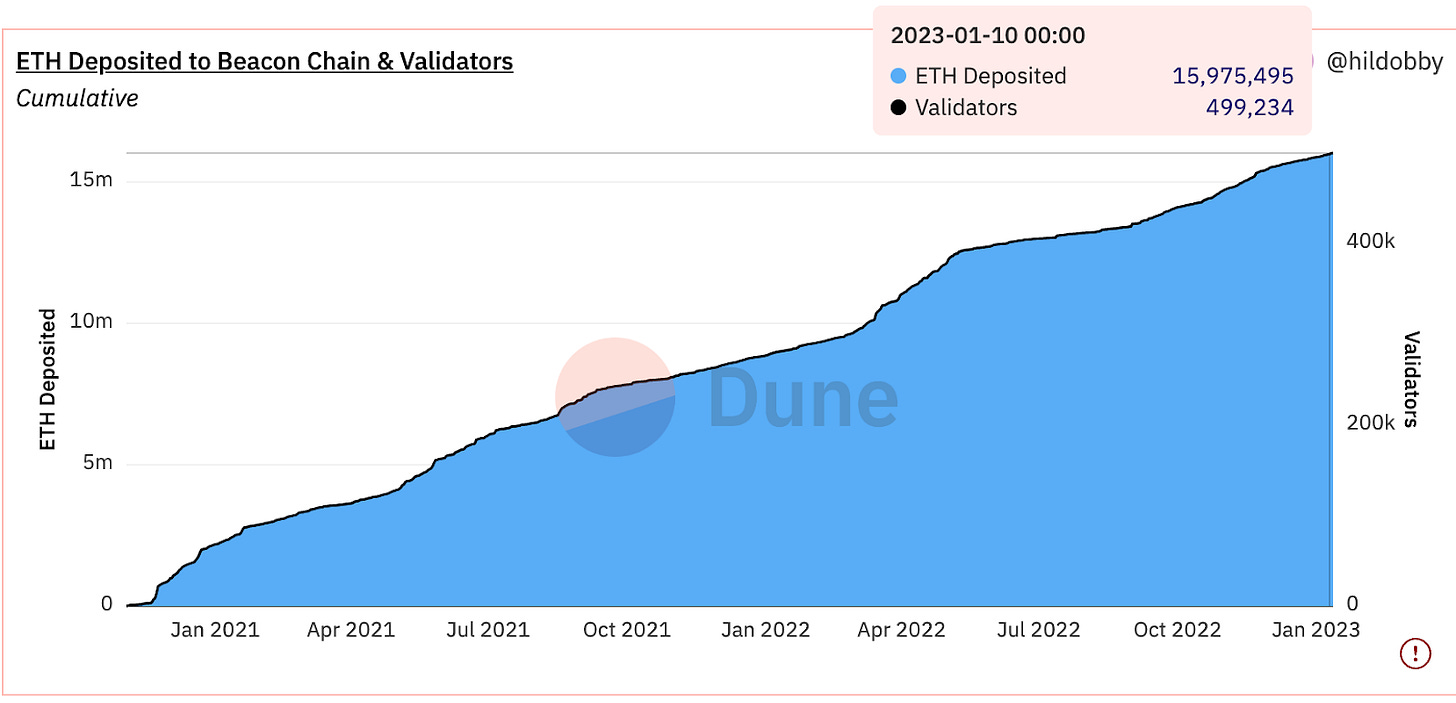

What’s interesting here is that we can see on-chain that there are 499,234 validators staking a total of 15,975,495 ETH. At the time of this writing, it’s not possible to withdraw that ETH, which effectively removes it from circulation.

However, in a few months, a new upgrade to Ethereum will enable withdrawals and will allow this ETH back into circulation. ♻️

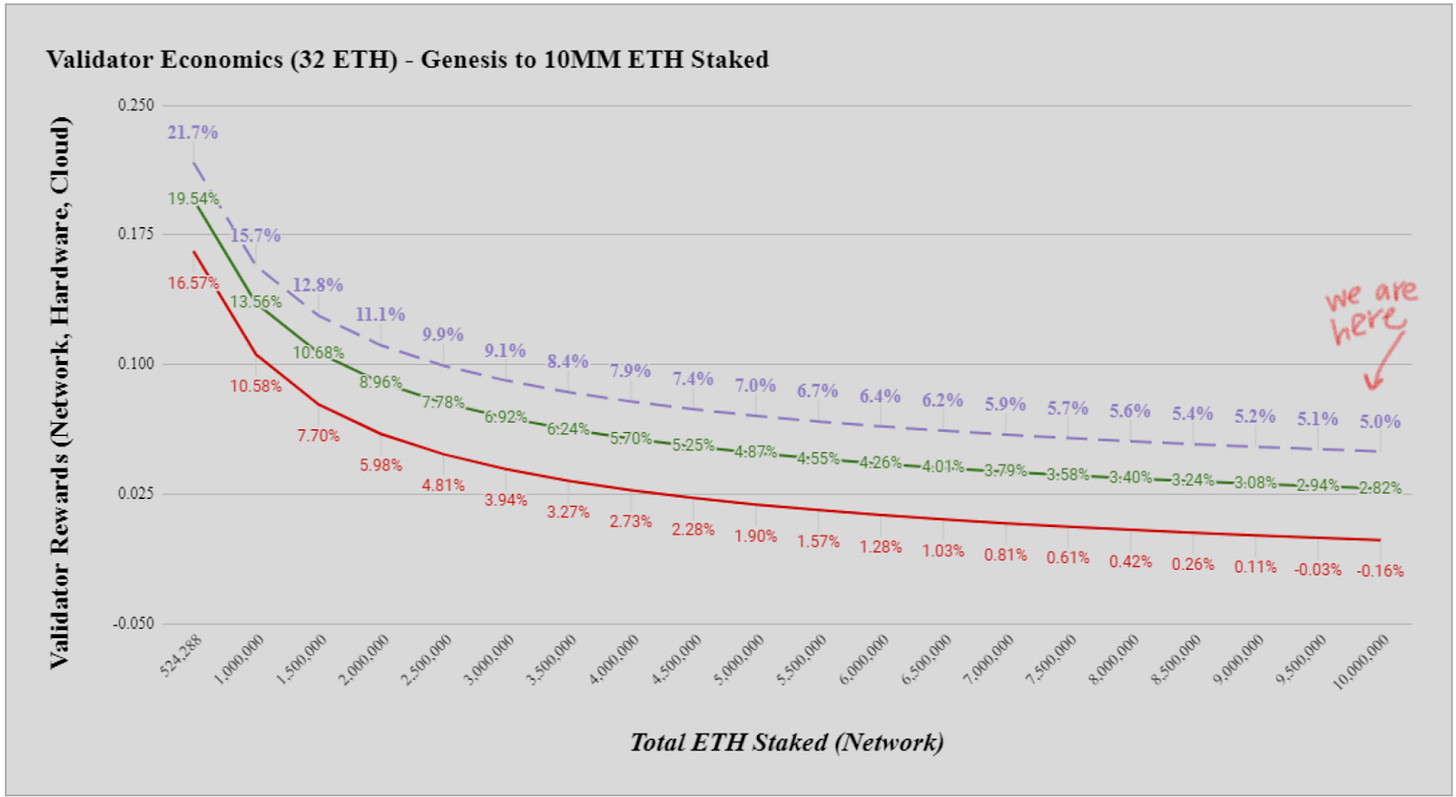

That said, Ethereum uses another intelligent incentive mechanism to ensure that people continue to validate the Ethereum network. It does this by using a sliding scale for how many rewards it provides to Ethereum validators based on the number of participants validating at any given time.

When fewer people are running a validator the % that a validator would earn increases and when more people are running a validator that % decreases.

Thus, if at any point people begin to withdraw their ETH and no longer validate Ethereum, there is an increased incentive for new people to join in and start validating. 💸

These incentives ensure that Ethereum maintains its security and decentralization of the Ethereum blockchain (it always comes back to ensuring the product remains the best it possibly can be).

You can see the validator economics in the chart below.

Key Takeaways From ETH Tokenomics

As you can gather from the information above, there is an important relationship between Ethereum blockspace (the product) and its token, ETH.

Neither could exist or function without the other. ⚖️

There is also an important relationship between ETH and the Ethereum community. Regardless of who you are and what you are doing in the Ethereum ecosystem, you must buy and use ETH. It means that developers, validators, users, and builders of the Ethereum ecosystem are all tied to ETH in some form.

It puts ETH at the center of the Ethereum ecosystem and the community. In my opinion, this is the purest form of web3 tokenomics.

This isn’t to say that all tokens must act as a currency as ETH does. I am simply highlighting the various roles that ETH plays in the Ethereum ecosystem.

Now, when designing tokenomics, we need to think about the following things:

How the token will maintain or appreciate in value over time (ie. why will people continue to buy or hold the token rather than sell it for another asset).

How the token amplifies my product or service (ie. incentives, experiences, access, etc.).

How the token will function for various participants across the community.

Remember that tokens can serve many purposes for many people within the same ecosystem. They can be used as governance, equity, access, rewards, points, revenues, currency, and more.

So the more that you can create value and utility towards your token for as many people in your community (users, developers, decision-makers, audience, etc.) as possible, the more sustainable the token will remain over time. 📈

Again, designing a successful token isn’t an easy task. This is an area that is still very much in the innovation stage. However, the dynamics that Ethereum has created with ETH can be used as inspiration.

I will be sure to highlight additional tokenomic designs in future PRO reports so that we can continue to learn the best tools to create a successful token.

If you have tokens that you believe have effective tokenomic designs, please share them in the comments below so all of our PRO members are aware of them.

I will also review and may use them in future reports (I would even love to co-create a report with you if you are already knowledgeable about another token’s design).

Thanks, PRO members and let me know below if you enjoyed this report! 😁

ABOUT THE AUTHOR

Kyle Reidhead

Founder of Web3 Academy and Impact3

Find him: Twitter

Collect this post as an NFT.