To truly grasp decentralized credit, we first need to get to the heart of understanding credit at large. Building a fundamental understanding of credit will allow us to appreciate better where DeFi credit fits into the overall picture, along with its strengths and weaknesses.

This article, “Credit”, marks the beginning of a series that aims to delve into the expansive concept of credit and extending credit on DeFi rails. This first paper serves as a foundation for understanding what credit is, and why it should be brought to DeFi.

The series will further cover the current decentralized landscape and nascent innovations, enabling readers to appreciate the transformative power of DeFi credit and empowering them with the discernment and recognition to identify transformative innovations within DeFi credit systems.

Finally, we will introduce OnCred, our contribution to the evolution of decentralized credit.

Borrowing and lending have been integral to human societies since ancient times, with early forms of credit involving lending materials to workers and expecting repayment in goods.

Today, credit is vital for the modern economy. It stimulates investment, spending, and consumption, ultimately the essential driver of economic growth by allowing borrowers access to capital now they otherwise wouldn’t have.

The most common form of this arrangement is a loan, where the borrower obtains credit from a lender with the expectation of repaying the principal plus interest or other fees.

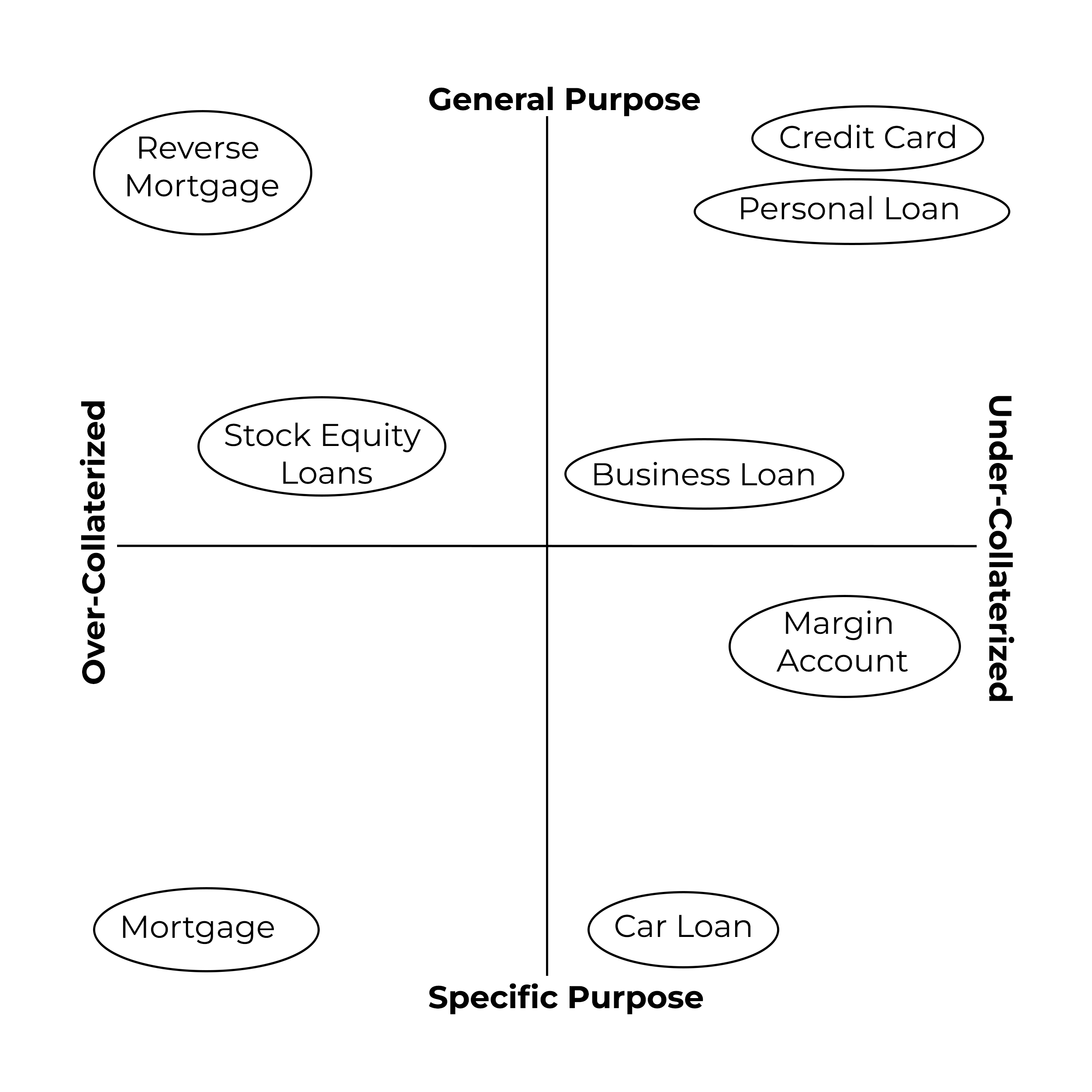

Three main factors determine the nature of a loan: the interest rate, the purpose of the borrowed funds, and how the loan is secured.

Let's take the example of a mortgage. Mortgages exist because an Individual that lacks the upfront affordability still wishes to purchase a property at its current market value. A homebuyer typically pays 20% upfront and borrows 80% from a bank when buying a house.

This loan facilitates the house purchase and is secured by the house itself. In mortgages, the bank holds the house deed, allowing them to repossess and sell the house if the buyer defaults on loan repayments, thereby recovering the loan amount. Additionally, the bank charges interest at their own determined rate on the borrowed amount as payment for the opportunity to borrow the funds.

Assets do not always back loans. In some instances, loans are backed by a claim on future income rather than direct collateral like a property. This gives rise to a spectrum of loans ranging from undercollaterized to overcollaterized. Credit card purchases and corporate bonds fall into the undercollaterized category. Typically the way an undercollateralized loan is secured is by the creditworthiness of the borrower.

Creditworthiness refers to an individual’s reliability in repaying debts in the past, proof of consistent income, and having enough funds to stay afloat in case of financial difficulties. This gives the lender confidence in the borrower's ability to repay the loan.

In case of non-payment, the lender has the option to pursue the borrower's other assets. If nonpayment does occur, outstanding claims are typically resolved through collections or bankruptcy processes.

Another important dimension is the purpose of the borrowed funds. Mortgages are specific-purpose loans. They can only be used to purchase nominated real estate. On the other hand, credit cards are general-purpose loans, as the borrower is free to use the borrowed funds however they want.

In traditional finance (TradFi), undercollaterized general-purpose credit is readily accessible. This is owing to the elaborate loan application procedures, Know Your Customer (KYC) verifications, and the formidable legal ramifications that stand poised to be enforced. Thus we see that the concept of creditworthiness effectively underpins undercollaterized credit in TradFi.

Lending across the dimensions discussed above is essential for the functioning of the modern economy as they provide the capital necessary for consumption, investment and growth. It is important to understand that loans can fall on a spectrum ranging from under to over collateralized and from specific to general purpose. Traditional finance encompasses all quadrants.

DeFi, short for decentralized finance, encompasses financial services on public decentralized blockchains, predominantly Ethereum. Within the realm of DeFi, one can engage in activities akin to those offered by traditional finance, including lending, borrowing, earning interest, and trading derivatives, among others.

The distinct advantages of DeFi include its swift settlement process, paperwork elimination, and eradication of intermediaries. All DeFi protocols fundamentally operate and secure their data through decentralized blockchain infrastructures. However, how a protocol secures and manages its operations and access to services varies on a spectrum from permissioned to permissionless.

On one end of the spectrum, permissioned protocols limit who can access them or their features. On the other end, interacting meaningfully with a permissionless protocol requires nothing more than a wallet.

Permissionless protocols generally possess the following attributes:

Security of an immutable and decentralized blockchain, such as Ethereum

Global availability 24/7

Access without identity, or vague eligibility criteria/standards

Functions independently from centralized authorities, including protocol owners

Non-custodial asset management whereby users retain control of their keys to access funds

Why is permissionless desirable? Permissionless protocols are unimpeachable, credibly neutral, and unbiased. They champion meritocracy by allowing the best players to succeed based on clear, predictable rules. In essence, they push the concept of individual freedom and autonomy to its logical extreme.

True permissionlessness extends beyond individual actors to other contracts, programs or even future neural networks, the ability to access and build products and services on top of existing ones. Innovation thrives when no barriers exist to building on existing products and services. Permissioned systems, on the other hand, can limit access as a strategy to build a moat and protect value capture.

While there is a case to be made for permissioned protocols, within the crypto community, a general view has been reached that permissionless applications reign supreme. Permissionless applications comprehensively embody the myriad of revolutionary value propositions decentralized blockchains offer.

In traditional finance, the extent of credit available to individuals is determined based on a widely recognized framework, the "5Cs of credit".

Character, Capacity, Capital, Collateral, and Conditions.

These 5Cs are used to evaluate a borrower's financial status comprehensively. For instance, a borrower's creditworthiness is assessed based on these 5Cs when applying for a home loan. Consequently, obtaining a loan in traditional finance is more complex than a simple wallet transaction, involving multiple parties and individuals contributing to the different steps of the process.

In the world of permissionless DeFi, the traditional 5Cs of credit are not fully applicable. Currently, our primary levers at scale are Capital, Collateral, and Conditions. As more of one's financial life transpires onchain, we may begin to incorporate Character and Capacity information into a decentralized credit decisioning engine. However, the feasibility of this approach at scale remains uncertain, given the cost and complexity of enforcement across disparate legal systems and jurisdictions.

Credit in DeFi is asset-backed. If those assets fall in value, borrowers in a rational market will default. TradFi mitigates this risk through legal enforcement and central banks acting as insurers of last resort.

DeFi, lacking the power of the state to enforce loan covenants and act as an insurer of last resort, relies on algorithms and game theory. While this approach limits the amount of credit that can be issued, it is a feature, not a bug. The total credit supply in DeFi is market-set.

By applying algorithms and game theory principles, DeFi democratizes access to credit, enhances transparency, and streamlines processes, all while providing robust security measures. DeFi has materially reduced the marginal cost of credit for all market participants.

For borrowers, it eliminates many of the traditional hurdles associated with obtaining credit. For lenders, it opens up new opportunities for participation and yields with transparent and automatic risk management in case of delinquencies. The principal benefits for borrowers and lenders are explored below.

TradFi loans are expensive and time-consuming. On average, only about 7% of loans are processed within a week, and the involvement of multiple parties increases lending costs. Even applying for a new credit line from your current financial institution may require going through the entire 5C vetting process again. The borrower usually bears the operational expenses passed on, resulting in higher overall costs.

Some well-known shortcomings of TradFi loans are:

Tedious processes of submitting and verifying personal information like income, expenses, assets, and liabilities for approval.

Dealing with the hassle of sending numerous physical documents.

Waiting for weekends when services are closed, leading to delays.

Managing interactions with customer service representatives or brokers.

Being subjected to settlement times and limits on funds.

Paying premium fees to financial institutions for the privilege of accessing the above services.

In contrast, contemporary DeFi models have revolutionized these cumbersome processes. At the fully permissionless end of the spectrum, borrowers can connect their wallet and engage directly with the protocol, eliminating all aforementioned middlemen and intermediaries.

For permissioned DeFi credit applications that may require credit checks and some offchain dependencies, the associated overhead remains significantly reduced as borrowers only go through minimal intermediaries, such as the protocol itself and a credit check, thereby still expediting the overall process.

In addition to eliminating outdated and inefficient intermediaries, DeFi offers borrowers a wide range of services and features that would be otherwise inaccessible without the utilization of blockchain technology. Some of these include:

24/7 availability, ensuring uninterrupted access and loan management.

Instant origination, borrowing, repayment, closure, and settlements for quick and efficient transactions.

Access to additional DeFi tools like flash loans for collateral swaps, wrapped interest-bearing collateral and other functionalities.

Non-custodial access to funds, granting users full control and ownership over their assets.

Reduced fees and costs, resulting in more cost-effectiveness.

Competitive interest rates and favourable lending terms, including perpetual terms and considerations for health factors.

By eliminating the aforementioned burdensome experiences, borrowers can truly unlock a seamless and cost-effective financial journey with access to competitive interest rates and bypass traditional complexities.

DeFi allows any individual to participate as a lender, completely democratizing access to yield. This can prove highly rewarding and, in many instances, is safer than lending offchain.

DeFi systems offer lenders transparency and equal information access, thus creating a level playing field. Unlike in TradFi, where private lenders may have an information advantage, DeFi's on-chain nature eliminates information gaps and ensures equitable treatment for all lenders. DeFi credit protocols can provide real-time on-chain credit scores and historical borrowing data, enhancing loan transparency compared to centralized counterparts. This transparency fosters a fair and just lending environment.

Lenders also enjoy enhanced safety benefits in DeFi. Borrower negligence is governed by code, which ensures better protection of lender capital through automated liquidations of borrower collateral in case of default. This surpasses traditional finance methods, where the priorities and considerations are often opaque and involve lengthy legal processes to unpack and unwind.

Onchain reputation for an address, demonstrating their creditworthiness through consistent responsible behaviour similar to traditional systems is possible. However, this approach faces fundamental challenges for a fully permissionless system, mainly the ability to change addresses and insufficient penalty enforcement to deter defaulting.

In TradFi, consequences like damaged credit scores, higher borrowing costs, and limited credit access motivate debt repayment. However, in permissionless DeFi, credit scores aren't applicable as borrowers are anonymous, lacking identifiable individuals or recourse in case of default.

Anonymity enables permissionlessness and self-sovereign identity but also incentivizes Sybil borrowing. Sybil Borrowing is a practice where an individual or entity creates multiple anonymous or disposable identities to obtain loans. If these loans default, it doesn't affect the creditworthiness of the real borrower, as seemingly unrelated entities took out the loans. This practice is particularly problematic in DeFi due to the ease of creating new, anonymous addresses.

Preventing defaults based on individual addresses alone would be ineffective. This goes back to our inability to effectively decision credit in permissionless DeFi based on ‘character’. Current DeFi lending models lean heavily on collateral and capital via overcollateralized loans. Similar to reverse mortgages in TradFi the borrower would be disincentivized to default as they have assets with a higher notional value at risk than what they borrowed.

Sybil Borrowing is the primary challenge to why unsecured general-purpose credit is, at this stage, still not possible for a fully permissionless protocol.

The underlying blockchain provides a trustworthy and verified data environment. However, this is only true for data inherent to the chain, such as transaction settlements. Often applications need to involve data that cannot be found on the blockchain. This introduces offchain dependencies like Oracle price feeds or offchain credit check providers. This trade-off, while often valid, can compromise the integrity and robustness of DeFi applications.

Stablecoins, like USDC, are prime examples, as their reliance on external entities to onramp, offramp, and custody USD exposes them to traditional banking risks, government intervention, and asset sanctions. Similarly, oracles, which provide offchain data to onchain applications, can become points of vulnerability if compromised. These dependencies can undermine the inherent value and integrity of onchain applications.

The decision to incorporate or exclude off-chain dependencies presents a substantial constraint and compromise in developing credit systems within DeFi. It represents a trade-off between maintaining the decentralized ethos of DeFi and ensuring the robustness and reliability of the credit system. Furthermore, offchain dependencies add complexity and increase the surface area of the entire system. It is crucial to balance the level of offchain dependencies with the level of security, utility and permissionless access needed in a DeFi credit system.

Transparency, a fundamental benefit of public blockchains, can also impose risks and limitations on credit in DeFi. The open nature of blockchain transactions allows anyone to view and analyze the activity of any address, which can lead to potential risks and challenges.

For instance, the dominant credit system in DeFi is overcollateralized loans, where the loan covenant requires the borrower to maintain a specific loan-to-collateral ratio. When breached, the borrower’s collateral is liquidated to protect lenders. Traders can monitor the liquidation thresholds of others, leading to predatory practices like "liquidation hunting." This involves intentionally manipulating market prices or interest rates to trigger the liquidation of a borrower's collateral, thereby profiting from their loss. An example could be a trader shorting a particular asset when they notice a large position is close to being liquidated.

Moreover, exposing a credit protocol's inner workings removes any ‘security via obscurity’. Savvy traders can exploit this transparency to manipulate the ‘rules of the game’ for personal gain, often going against the protocol design principles and vision - destabilizing the protocol and potentially leading to significant losses for other participants.

It's worth noting that these transparency-related challenges do have known solutions, unlike sybil borrowing. Open research in an area known as Zero-Knowledge (ZK) proofs, which allow for verifying information without revealing the information itself, will allow future protocol engineers to decide where to draw the trade-off between transparency and confidentiality.

While transparency is a significant advantage of DeFi, it also brings its own set of challenges. Balancing the benefits of transparency with the need for privacy and security is a key consideration in the development of DeFi credit systems. As the DeFi landscape evolves, emerging technologies and approaches will address these challenges.

To fully realize the potential of DeFi as an independent financial infrastructure, it must encompass essential functions of traditional finance, including undercollateralized and general-purpose credit. These functions align with the core purpose of finance, which is to match capital requirements with the term of return to foster investment and growth.

Today's dominant form of credit in DeFi is overcollateralized lending, akin to reverse mortgages in traditional finance. While this form of lending provides some liquidity, it also limits borrowers by tying up their assets that could be used more productively elsewhere. Here, liquidity refers to the availability of assets that can be easily converted into cash without affecting the market price. For economic growth, liquidity is crucial as it enables businesses to meet short-term obligations and invest in growth opportunities.

However, overcollateralized lending in DeFi differs from traditional reverse mortgages in that liquidation is automatic and tied to observable market prices. This essentially makes the loan term market dependent as opposed to purpose dependent - as such, even though in theory it’s a general purpose loan, in practice, it is mostly used to facilitate leverage trading as opposed to economic growth via productivity increase.

Economic growth relies on liquidity, not just leverage. Consider a company that can significantly contribute to global GDP but requires a substantial upfront investment. Depending solely on internal profits, it could take years to accumulate the necessary funds. Traditional finance offers immediate access through a corporate debt market, whereas existing overcollateralized lending protocols in DeFi cannot support such ventures without realized income streams.

While DeFi has made significant strides, the journey to fully decentralized credit is still very early. Aligning loan terms to purpose and reducing collateralization without opening the system to Sybil attacks are but a few promising areas of exploration in this emerging field. The potential rewards are immense, promising a more inclusive, efficient, and resilient financial system.

This article serves as a primer, a foundation for understanding credit and its potential in the decentralized world. The deep understanding of credit fundamentals provided in this article is crucial to envisioning the path forward for decentralized credit.

Our next article explores DeFi credit prior art, unravelling the current landscape and offering insights on the innovations enabling the future of decentralized credit.

The future of credit is decentralized. We are just getting started. We are early.

Baker, L. (2023) “Paradigms for On-Chain Credit,” Jump Crypto. 22 August. Available at: https: /jumpcrypto.com/writing/paradigms-for-on-chain-credit/

Treehouse Finance (2022) “The Holy Grail of DeFi Lending: Undercollateralized Loans” Treehouse Research. 28 December. Available at: https: /www.treehouse.finance/insights/the-holy-grail-of-defi-lending-undercollateralized-loans

FranklinDAO Research and Isaac Tham (2022) “Undercollateralized Lending: Better Yields with Better Risk Management: Musings on undercollateralized lending by Isaac Tham,” FranklinDAO Research Substack, 23 December. Available at: https: /franklindao.substack.com/p/undercollateralized-lending-better

Kenton, W. (2023) “Over-Collateralization (OC): Definition, Benefits, and Examples,” Investopedia. Available at: https: /www.investopedia.com/terms/o/overcollateralization.asp

My debut blog article is here! first article in a series of three introducing oncredxyz.twitter first 2 articles are thought-provoking educational releases aiming to ignite conversations. The last unveiling our vision for the future of DeFi Read it here: https://paragraph.xyz/@oncred/credit s/o @colin and @paragraph