In our initial article, “Credit”, we established a solid foundation for comprehending the concept of credit and presented a compelling argument highlighting the growing demand for decentralized, permissionless credit.

In this second article of our series, "Onchain Credit," we aim to dive into the various products and services that make up this world. We explore the primary applications of credit within the current landscape, examining trends, demand, and utility in the DeFi market as well as nascent technologies enabling the future of the decentralized credit space.

A sufficient understanding of prior art will serve as a foundation for readers to identify transformative innovations in DeFi credit systems. Opening the path to introduce OnCred.

Existing decentralized credit protocols are estimated to be worth 40-50 billion dollars (200 billion at market peak). These applications have been instrumental in shaping the DeFi industry as we know it today. Let's delve into some of the most prominent credit protocols in DeFi, exploring their mechanisms, benefits, limitations and how they map to offerings within the traditional finance world.

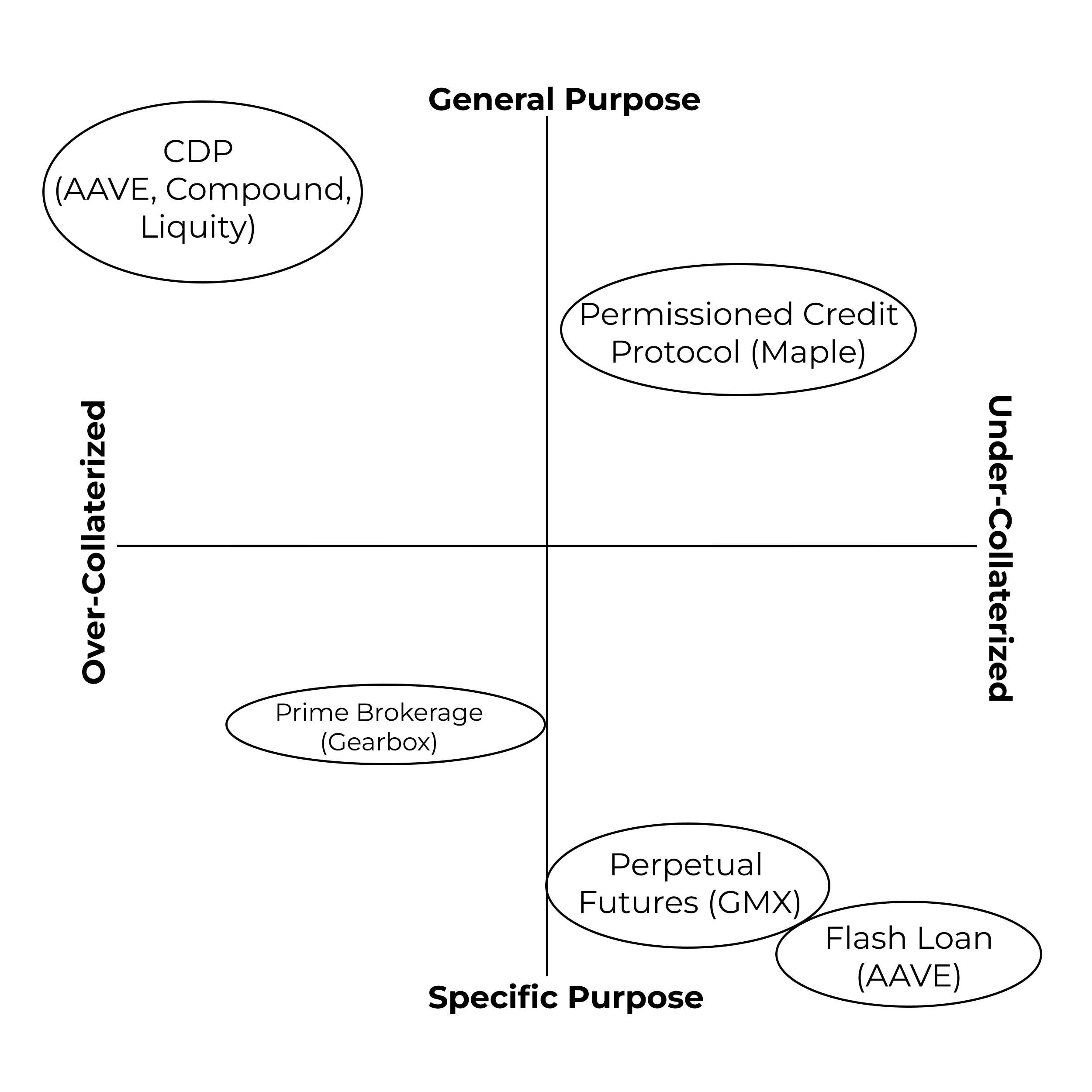

The most common form of DeFi credit is through overcollaterized loans known as Collateral Debt Positions (CDPs). These are akin to a reverse mortgage in TradFi.

Borrowers offer collateral and draw out cash that is less than the value of that collateral. This approach is driven by DeFi's permissionless nature, promoting efficiency and avoiding bias against borrowers. Furthermore to mitigate risks, CDPs use heavy, in most cases 150%, overcollateralization and automatic liquidation to safeguard lenders and the protocol from insolvency.

Overcollateralized loans in DeFi are currently used to implement diverse trading and hedging strategies. They provide much-needed access to capital without the need to sell your precious crypto and allow for extremely flexible loan terms, in many cases perpetual terms with only the need to maintain an LTV ratio.

DeFi CDPs serve as a compelling example of the advantages highlighted in our first article, embodying a product that exhibits comparable capital efficiency to traditional finance, specifically reverse mortgages, with origination and operational efficiencies gained due to it being built onchain in a permissionless manner.

However, these loans have similar limitations to reverse mortgages. They are exclusive to asset owners, requiring locked collateral exceeding the borrowed amount. Borrowers cannot access this collateral until the debt is fully repaid, reducing capital efficiency. Borrowers risk losing a portion or all of their collateral in case of liquidation.

All that said, permissionless CDP lending has shown to have serious demand and is the foundation of the current DeFi market, with a single major protocol like Aave having an all time high total value locked (TVL) exceeding $30 billion whilst still maintaining over $5 billion in TVL during even the most bearish periods.

Flash loans, pioneered by lending platform Aave, were designed for developers with technical knowledge. They allow borrowing assets without collateral, as long as the loan is repaid in one transaction. Flash loans are the truest permissionless unsecured credit in DeFi.

Flash loans are a product unique to DeFi, they cannot be offered offchain in any capacity. They open up a plethora of further unique DeFi use cases. However, use cases are niche and demand a high level of competence for utilization. Moreover, these cases are limited to extremely short-term loans, lasting just one block. An example is trading arbitrage, where traders can profit from small price differences between exchanges.

To get a flash loan, you need to create a smart contract and execute the required steps, including repaying the loan with the flash loan fee (typically a small % of the loan) in the same transaction, in 1 block.

We believe flash loans today are heavily underutilized and will become a major building block of decentralized credit opening up extremely innovative possibilities.

Perpetual futures are a trading product offered by centralized exchanges, allowing users to enter leveraged long and short positions for trading. This involves borrowing funds from the exchange, essentially functioning as credit.

In DeFi, platforms like GMX and DyDx incorporate perpetual futures contracts using liquidity pools. Users opt for leverage and pay open position fees and ongoing borrowing fees based on the duration of the trade. Profits and losses accumulate until traders close their positions or face liquidation.

It's important to note that this credit is specific to short-term leverage trading contracts for underlying assets and cannot be used for other purposes. Leveraged trading carries significant risks, with liquidations being very common.

Due to the high-risk nature, this product is in extremely high demand in the crypto market, attracting a large number of daily active users and generating substantial fee revenue for these protocols. This comes as no surprise, considering it incorporates the most sought-after feature from traditional exchanges and delivers it permissionlessly, allowing for democratized access and financial inclusion.

Prime brokerage credit protocols are one of the newer additions to DeFi credit. These protocols provide a framework by which the same lending capital can be generalized across different use cases, in contrast to perpetual futures, where protocols like GMX can only support a single purpose.

A notable example is Gearbox, a recent prime brokerage protocol on Ethereum. Gearbox enables users to leverage their positions through a "credit account." This account restricts capital deployment to approved trading strategies. By limiting where capital is deployed, often to 'blue chip' assets with deep liquidity, the protocol can better manage liquidations if the borrower's trades move unfavorably.

The innovation of requiring less equity to generate leverage by constraining its use is an important evolution in DeFi. It allows lenders to maintain overcollateralization across both equity and assets, protecting them against default in a permissionless environment while expanding where and how borrowers can put leverage to use.

While the potential of prime brokerage protocols is promising, the current market demand for this offering remains uncertain due to its infancy. As the DeFi space matures, we expect there to be more experimentation in how protocols balance capital, collateral and conditions to provide permissionless and frictionless credit.

The innovation covered thus far has centered on permissionless credit. These protocols primarily rely on three factors: the lender's ability to provide capital, the collateral procured through the credit provided, and the loan conditions dictated by the protocol.

However, in the past two years, a new breed of protocols, known as permissioned credit protocols, have emerged. These protocols shift the focus towards assessing the character and capacity of the lender and borrower, leveraging the public blockchain for settlement to enhance loan efficiency.

This makes permissioned protocols remarkably similar to credit as offered in traditional finance. This similarity serves as an easy onboarding for market actors and is an extremely bullish case for the overall adoption of blockchain and our crypto industry. Further, they are the main usable form of undercollaterized lending in DeFi as it stands.

The key innovation of this class of protocol is to open up a marketplace for third-party risk assessment. This model introduces a separate entity responsible for conducting credit assessments, distinct from lenders and borrowers. As a requirement, this entity often stakes a portion of capital as a ‘performance bond’, and risks this capital to incentivize their accountability in the event of a loan default that they approved.

Prominent credit protocols, like Maple Finance, Goldfinch, and TrueFi, rely on third-party risk assessments and attract substantial interest from institutional lenders and borrowers. These platforms manage multiple billions of dollars in TVL and, operating under a permissioned model, are currently the strongest sector for credit in DeFi.

Its main benefit, opening up undercollaterized loans, is also a drawback. Borrowers are predominantly, or at this stage entirely, risk-assessed institutional borrowers benefiting from the lucrative liquidity of DeFi markets. Third-party risk assessors can have more confidence in these borrowers due to their corporatization and penalty accountability. Regardless, the market clearly favors this approach, with the aforementioned protocols holding some of the highest TVL numbers in all of DeFi.

As touched upon extensively throughout this article series, the pursuit of unsecured lending, is driving innovation in our DeFi space. We are starting to see some emerging technologies, explored below, that are enabling the realization of these offerings.

Introduced in 2022 by Chainlink, a leading blockchain middleware layer, DECO is a privacy-preserving oracle protocol that enables undercollateralized lending. It provides a way to prove data without revealing sensitive information, ensuring confidential attestation of offchain data. DECO utilizes zero-knowledge proofs (ZKPs) to verify the authenticity of offchain data while maintaining privacy. This allows borrowers to demonstrate creditworthiness, such as credit scores, without disclosing specific details. Notably, DECO is already integrated into emerging protocols like Teller to verify bank account balances and more.

By addressing the need for privacy and data access while enabling trustless creditworthiness verification, DECO plays an invaluable role in shaping the future of credit on DeFi platforms.

KYC (Know Your Customer) is a standard procedure in traditional finance, but crypto KYC adds a unique twist. In many cases, crypto KYC requires onchain verification in a trustless manner. While not all onchain KYC utilizes zero-knowledge proofs (ZKPs), ZK-KYC offers a more permissionless approach on blockchains. Alternatively, non ZK-KYC is typically performed by a traditional company that confirms onchain activity when necessary. For instance, Blockpass, a SaaS company, facilitated wallet KYC for the NFT land sale of Yuga Labs Otherside metaverse.

While there are multiple proposed solutions for implementing ZK-KYC, the core components and benefits of this concept involve KYC parties authenticating individuals' identities without knowledge of their digital asset wallets or DeFi activities. All while DeFi protocols interact with digital asset wallets but lack information about the individuals themselves.

The final element of this puzzle involves a method for verifying and disclosing an individual's actions in cases of suspected malicious activities. This solution architecture remains highly technical and experimental. Nevertheless, ZK-KYC in DeFi aims to successfully balance regulatory transparency with user privacy concerns unlocking vast opportunities for new credit applications and unprecedented capital efficiency in the DeFi industry.

Enforcement of any form of KYC even a fully private ZK-KYC does mean the protocol falls on a more permissioned side of the spectrum as it places potential limits on users based on location, age and even the legal ability to hold or complete identification.

Onchain credit scores are also a key pillar in bringing undercollaterized lending onchain. Onchain credit scoring is extremely nascent, and there is no clear utilized framework but rather a plethora of far and wide concepts and designs. These solutions range from permissionless to permissioned and from potentially very effective to just a better solution than psuedo-anonymous addresses with no history attached.

New and more inherently onchain credit scoring generally involves previous wallet activity such as trading, historical loan repayments, and governance participation being scored and tied to a wallets history in one way or another. There are many concepts and designs of this type of psuedo-anonymous onchain credit history and many protocols are experimenting with these at this time. Should a protocol choose to integrate or enforce this, it starts to differ the level of access to users rather than having an unbias level playing field for all. This trade-off of access is made for more features than you could potentially get in a fully permissionless credit system.

A fully permissioned example of onchain credit is a system like Credora, where similar to TradFi it has a full KYC with financials and assets review, which is then placed onchain against your wallet.

Nonetheless, the future risks and benefits are yet to be seen for all onchain scoring methods. However, we see onchain credit scoring becoming increasingly adopted on many DeFi applications, as a reliable form of reputation building to allow for more access to products and services akin to TradFi.

The holy grail and vision of Ethereum, to tokenize the world and bring it onchain. RWAs, short for real world assets, are exactly that, and integrating offchain assets onchain opens up new use cases especially for collateral or loan support options in credit systems. The most common form of RWA is arguably stablecoins with backed USD reserves. However in the context of credit, we will explore how tokenizing something like real estate could be effective.

Firstly, there are two broad token formats for generating RWAs. The first involves non-native tokens, where onchain tokens represent RWAs managed offchain by a custodian. This format is commonly used due to the early stage of RWAs and the ability to leverage existing financial infrastructure for asset custody. It will also be the one used for assets such as real estate. Most existing USD-collateralized stablecoins follow this token format.

The second format is native tokens, where an onchain token serves as the RWA itself, without representing any off-chain asset. For example, bonds directly issued onchain as tokens are native RWAs, while a bond issued and held offchain can be tokenized as a non-native RWA.

RWAs have attracted considerable institutional interest, with a notable example being the Singapore Central Bank's Project Guardian. This project conducted in late 2022, explored the application of DeFi in wholesale funding markets. The pilot involved DBS Bank, JP Morgan, and SBI Digital Asset Holdings and resulted in JP Morgan executing its first DeFi transaction on a public blockchain. Trading $100,000 tokenized Singapore dollar deposits (the first issuance of tokenized deposits by a bank) for tokenized yen issued by SBI Digital Asset Holdings.

More close to home, MakerDAO, one of the earliest and largest CDP platforms, currently has the highest adoption rate of RWAs in DeFi, using them as part backing for its stablecoin DAI and other experimental use cases within its protocol.

It is clear that RWAs will play a major role in the future of decentralized credit. Tokenizing real world assets presents significant opportunities for both established financial institutions and the emerging DeFi ecosystem. While there are challenges to overcome, the potential market for RWAs is vast, amounting to trillions of dollars. With the disruption of nearly every traditional financial stronghold, the vision of tokenizing the world is on the horizon, waiting to be realized.

This article series aims to explore potential product-market fits that drive advancement in the decentralized credit sector. In this context, capital efficiency plays a crucial role.

Capital efficiency involves utilizing capital in a productive and optimized manner to achieve maximum returns or outcomes. In decentralized credit, it means optimizing available capital in lending markets to contribute to industry growth by increasing liquidity. As we discussed in our previous article, it's important to note that economic growth relies on liquidity, not just leverage.

Achieving high capital efficiency is vital for our nascent DeFi industry. It accelerates growth, attracts further investment, increases market stability, and builds confidence and credibility in DeFi. Most importantly, it enhances overall liquidity within the markets.

How would a DeFi protocol contribute towards higher capital efficiency in our markets? It all comes back to ways in which a protocol can reduce required capital and collateral requirements by innovating tools and financial products. This is the key unlock for investors to effectively deploy their capital and, importantly, unlock liquidity.

Most DeFi applications rely on a liquidity pool model, where lending is necessary for borrowing. While this model has advantages, it restricts the scalability of leverage and liquidity offered by these products. While the fully backed nature of DeFi prevents the creation of credit out of thin air, there is potential for exploring more efficient lending models.

To enhance capital efficiency and boost liquidity, we look for a protocol allowing users to leverage without being constrained by their lender liquidity pools. This approach paves the way for a more scalable and robust lending model, unlocking on-demand liquidity and ultimately leading to increased capital efficiency.

The next potential innovation on the current DeFi Lending model would be to improve collateral ratios. Take CDPs as an example. Although they unlock some liquidity, their collateral requirements (150%) often outweigh the liquidity they offer, resulting in inefficient liquidity ratios. Introducing a product within a protocol that enables collateral ratios below 100% while ensuring full loan security would deliver a more capital-efficient solution for the market.

How to attract new market participants? It's simple, by introducing a financial product that is currently unavailable in the market. To take it a step further, by offering a financial product that fundamentally differs from the existing options in our market. This approach is almost certain to attract a fresh set of users.

Most credit products available today cater specifically to current market participants. For example:

CDPs enable crypto asset owners to utilize their assets for various purposes.

Flash loans serve niche needs of highly technical individuals in the crypto space.

Perpetual trading and prime brokerage platforms provide short-term leverage trading, which represents one of the largest use cases in the crypto domain.

It is evident that the current market is largely driven by high-risk strategies, reflected in the tools that receive the most attention, often involving substantial short term leverage. Additionally, the tools available cater primarily to current crypto holders rather than new entrants with minimal crypto assets.

Considering the industry’s maturation trajectory, newer entrants may increasingly desire less risky products, particularly those that offer utility to individuals with minimal crypto asset exposure. Protocols that offer longer term, more responsible lending financial products could attract users seeking a more sustainable approach to increase their crypto assets.

Further to the more responsible leverage offerings, incorporating insurance elements for added security could incentivize more TradFi capital to enter the space as it starts providing similar services.

These approaches will entice new capital into our industry, igniting growth and enhancing capital efficiency.

The decentralized credit landscape is diverse and rapidly evolving, driven by the dual pursuits of expanding utility and usability for users and increasing capital efficiency. As we have explored in this paper, there are many permissionless products and services catering to different needs and risk profiles. There are also permissioned protocols bringing the building blocks of TradFi while grasping the benefits of being onchain and in many cases, enhancing the offerings.

However, the journey is far from over. We see that all the new emerging technologies like DECO, ZK-KYC and RWAs are pushing the boundaries of what's possible in permissioned DeFi. While these innovations are expanding both DeFi credit utility and capital efficiency, opening up exciting new opportunities, we believe the potential of DeFi extends beyond replicating and enhancing traditional finance on top of blockchain rails.

The real opportunity lies in creating novel fully permissionless financial products and services that are uniquely enabled by blockchain technology. Most permissionless DeFi credit protocols serve as intermediaries that connect borrowers and lenders. These protocols typically do not originate loans directly, and most non-overcollateralized credit protocols do not enable long term, responsible credit generation.

By innovating lending models, reducing collateral ratios, introducing responsible long term lending products, and incorporating insurance elements, permissionless DeFi protocols can, and will, attract a wider range of participants. Fostering a more robust and capital-efficient ecosystem, and ultimately allowing for a fully independent, unstoppable financial system to flourish.

As we look to the future, it's clear the DeFi industry has the potential to transform the world of credit, offering unprecedented financial inclusion and democratization. This article sets the scene to identify and discern the protocols that will revolutionize the future of permissionless credit.

Our next article introduces OnCred.

A revolution for onchain credit. We are just getting started. We are early.

Baker, L. (2023) “Paradigms for On-Chain Credit,” Jump Crypto. 22 August. Available at: https: /jumpcrypto.com/writing/paradigms-for-on-chain-credit/

Treehouse Finance (2022) “The Holy Grail of DeFi Lending: Undercollateralized Loans” Treehouse Research. 28 December. Available at: https: www.treehouse.finance/insights/the-holy-grail-of-defi-lending-undercollateralized-loans

AAVE Flash Loans - FAQ. Available at: https://docs.aave.com/faq/flash-loans.

Zeller, M. (2021) “Sneak peek at Flash Loans - Aave Blog - Medium,” Medium, 13 December. Available at: https://medium.com/aave/sneak-peek-at-flash-loans-f2b28a394d62.

Capital, C.C. (2022) “The Current State of Undercollateralized DeFi Lending — 2021,” Medium, 6 January. Available at: https://medium.com/coinmonks/the-current-state-of-undercollateralized-defi-lending-2021-1f84e14527b5.

Chainlink (2022) “How DECO Enables Undercollateralized DeFi Lending: A Proof of Concept With Teller,” Chainlink Blog. Available at: https://blog.chain.link/undercollateralized-lending-teller-deco-poc/.

Pauwels, P. (2022) zkKYC in DeFi: An approach for implementing the zkKYC solution concept in Decentralized Finance. Available at: https://eprint.iacr.org/2022/321.

Protocol, T. (2023) “What is DeFi Lending? An Intro to Decentralized Finance,” Teller Blog. Available at: https://blog.teller.org/what-is-defi-lending/.

ChainLinkGod (2023) “Tokenized Real-World Assets (RWAs): Scaling DeFi to a Global Level,” Chainlink Blog. Available at: https://blog.chain.link/tokenized-real-world-assets/.

Yang, Y. (2022) “JPMorgan Executes Its First DeFi Trade Using Public Blockchain,” Bloomberg.com, 2 November. Available at: https://www.bloomberg.com/news/articles/2022-11-02/jpmorgan-executes-its-first-defi-trade-using-public-blockchain.

Second article is out now! Dive into our insightful series, this compelling piece sets the scene to introduce oncredxyz.twitter in the next article Read it here: https://paragraph.xyz/@oncred/onchaincredit